|

市場調查報告書

商品編碼

1637878

亞太地區酒精飲料包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)APAC Alcoholic Drinks Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

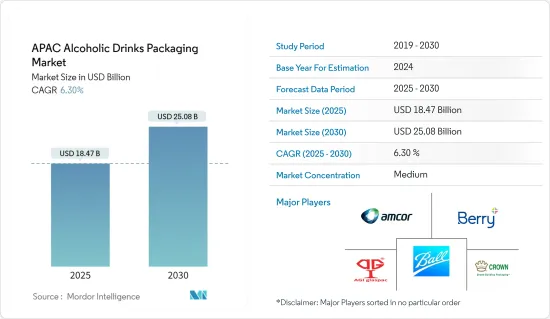

亞太地區酒精飲料包裝市場規模預計在 2025 年達到 184.7 億美元,預計到 2030 年將達到 250.8 億美元,預測期內(2025-2030 年)的複合年成長率為 6.3%。

隨著該地區酒精飲料消費量的增加,對飲料包裝瓶和罐的需求預計將增加。瓶子和罐子很受顧客歡迎,因為它們易於運輸和儲存。預計這些因素將推動亞太地區酒精飲料包裝市場對瓶子的需求增加。

酒精飲料製造商提供各種各樣的產品,包裝對於擴大其市場範圍至關重要。消費者在休閒上的支出增加,加上社會接受度的提高,導致對酒精飲料產品的需求穩定成長,從而對包裝行業產生了影響。

玻璃由於其可回收性、再生性和中性反應性,已成為成長最快的酒精飲料包裝材料之一。此外,金屬罐的日益普及也推動了酒精飲料包裝市場的發展。金屬罐是用於儲存和分配酒精飲料的包裝容器。它的強度和剛度使其能夠快速輕鬆地填充罐子而不會損失酒精。

此外,該地區的酒精市場受到節慶、都市化、婦女賦權和社會傾向青年人口增加等各種因素的影響,這些因素正在推動市場成長。此外,預測期內,淡啤酒、葡萄酒、低酒精飲料、利口酒和單一麥芽威士忌等新酒精飲料類別的大量成長也將推動該地區包裝市場的發展。

亞太地區酒精飲料包裝市場趨勢

金屬包裝強勁成長推動市場

- 酒精飲料包裝市場根據塑膠、紙張、玻璃和金屬等多種材料進行細分。它還涵蓋瓶子、罐子、袋子、紙箱和類似容器等產品。此外,市場分析還考慮了永續性、飲料產品的生產力、供需以及疫情對市場的影響等多種因素。

- Ball Corporation、Amcor Group Gmbh 和 Berry Global Inc. 等公司預測其在印度的金屬包裝業務將大幅成長。由於其永續性,威士忌、葡萄酒和烈酒等新類別正在轉向使用鋁罐。

- 啤酒愛好者和釀酒師都認知到罐裝啤酒在維持飲料品質和新鮮度方面的好處。罐子能更好地抵禦光線和氧氣,因為光線和氧氣會使啤酒隨著時間的劣化。此外,金屬罐的可回收性很高,回收所需的能源也比玻璃瓶少。隨著該地區努力建立更加綠色的未來,啤酒產業轉向罐裝符合國家永續性目標。

- 此外,該公司正在投資金屬包裝的未來,因為他們了解選擇完全可回收的飲料包裝對社區和環境的巨大影響。印度的企業正在積極探索擴大產品類別,以涵蓋相當廣泛的酒精飲料。各公司也密切關注監管動態,希望創造對罐頭更有利的環境。

- 印度工程出口促進會表示,2023年印度鋁及相關產品的淨出口額將達88億美元。隨著出口價值的增加,鋁生產可能實現規模經濟和成本效率。這可以使酒精飲料的包裝選擇更加實惠,並成為製造商更理想的選擇。

- 在該地區經營的酒精製造商正專注於推出新的包裝酒精飲料。例如,2024 年 3 月,聯合啤酒有限公司 (UBL) 宣布推出罐裝Queen Fisher 啤酒。女王費雪啤酒 (Queen Fisher Beer) 是一款全女性努力的啤酒,從限量版女王費雪罐裝啤酒的配製到由女性釀酒師釀造。

預計啤酒將佔據很大的市場。

- 過去幾年,啤酒消費量有所增加。印度每年有超過 2000 萬達到飲酒年齡的人口,仍然是世界上最大的啤酒市場之一。印度最大的啤酒製造商和著名翠鳥品牌的生產商聯合啤酒公司 (United Breweries) 最近推出了最新系列翠鳥即溶啤酒。一盒該產品有兩袋。

- 帶有皇冠蓋的玻璃瓶是該地區傳統的啤酒包裝。玻璃廣泛用於酒精包裝,因此預計預測期內其需求將會增加。此外,玻璃價格對酒精產業的利潤率有顯著影響,並隨原油價格的波動而波動。

- 此外,無麩質啤酒在該地區越來越受歡迎。中國、印度和越南的啤酒消費量每年也以超過 6% 的速度成長。這將帶來偏好和烹飪方法的創新,刺激對啤酒的需求,並有望帶動罐裝啤酒的成長。

- 根據中國國家統計局的數據,2023年7月中國啤酒產量接近400萬千公升,2022年12月為254千萬公升。啤酒產量的增加可能會鼓勵包裝公司投入資金進行研發,發展出創造性的、環保的包裝選擇。環保包裝、新設計和新材料將提高亞洲酒精飲料包裝的品質和吸引力。

- 此外,2024 年 3 月在新加坡成立的 Lion Brewery Co. 正在開闢新局面,並在全球舞台上提升該國精釀啤酒的知名度。該公司是第一家利用線上硝化技術開發罐裝硝化烈性黑啤酒的精釀啤酒製造商,也是第一款在杜拜銷售的新加坡精釀啤酒。這是新加坡精釀啤酒品牌首次生產烈性黑啤酒黑啤酒。

亞太地區酒精飲料包裝產業概況

亞太地區酒精飲料包裝市場受主要企業的主導。市場的主要企業包括 Amcor Group GmbH、Crown Holdings, Inc.、Ball Corporation、AGI Glaspac 和 Berry Global Inc.該領域的最新策略舉措包括:

2023 年 8 月 - Crown Holdings Inc. 宣布收購飲料罐和蓋製造廠 Helvetia Packaging AG。收購薩爾路易工廠將擴大皇冠飲料罐網路,年產能約 10 億罐。作為協議的一部分,收購完成後,Crown 將接管 Helvetia 現有的基本客群和相關合約。

2023 年 7 月—Amcor Rigid Packaging (ARP) 為 Ron Rubin Winery 的新 BLUE BIN 葡萄酒系列推出了 100% 再生聚對苯二甲酸乙二醇酯 (rPET) 包裝。此系列產品有 750 毫升瓶裝。與傳統的葡萄酒包裝相比,rPET 包裝除了減少溫室氣體排放外,還具有許多環境效益。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場動態

- 市場促進因素

- 永續包裝需求不斷成長

- 亞洲酒精消費量上升

- 市場限制

- 政府限制塑膠的使用

第6章 市場細分

- 按材質

- 塑膠

- 紙

- 金屬

- 玻璃

- 依產品類型

- 瓶子

- 能

- 小袋

- 紙盒

- 按國家

- 中國

- 印度

- 日本

- 新加坡

- 澳洲和紐西蘭

第7章 競爭格局

- 公司簡介

- Amcor Group GmbH

- Mondi Group

- Crown Holdings, Inc.

- Gerresheimer AG

- Hualian Glass Bottle

- Ball Corporation

- AGI Glaspac

第8章投資分析

第9章:市場的未來

The APAC Alcoholic Drinks Packaging Market size is estimated at USD 18.47 billion in 2025, and is expected to reach USD 25.08 billion by 2030, at a CAGR of 6.3% during the forecast period (2025-2030).

The demand for bottles and cans in beverage packaging is expected to grow as alcoholic beverage consumption rises in the region. Bottles and cans are more convenient to transport and store, making them popular among customers. Due to these factors, the demand for bottles in the Asia-Pacific alcoholic drinks packaging market is expected to increase.

Packaging has been essential in market expansion, with alcoholic beverage makers offering diverse products. Consumer expenditure on recreational activities has increased, as has societal acceptability, resulting in a steady increase in demand for alcoholic drink goods, impacting the packaging industry.

Glass has emerged as one of the fastest-growing alcohol packaging materials due to its recyclability, reusability, and neutral reactivity. Also, the rising popularity of metal cans drives the alcohol packaging market. Metal cans are packaging containers for storing and distributing alcoholic beverages. Its strength and stiffness make filling cans faster and easier without losing alcohol.

Furthermore, various factors influence the alcohol market in the region, including festivities, urbanization, women's empowerment, rising numbers of young people who tend to socialize, etc, push the market growth. Moreover, a lot of growth from new alcoholic drinks categories like light beer, wines, light alcoholic beverages, liqueurs, and single malts also pushed the packaging market in the region over the forecast period.

APAC Alcoholic Drinks Packaging Market Trends

Significant Growth in Metal Packaging to Boost the Market

- The market for alcoholic beverages packaging research market segmentation based on several materials such as plastic, paper, glass, and metal. It also covers products such as bottles, cans, pouches, cartons, and similar containers. Furthermore, the market analysis considers several factors, including sustainability, beverage product production rates, supply and demand, and the influence of pandemics on the market.

- Ball Corporation, Amcor Group Gmbh, Berry Global Inc., and other companies foresee a significant increase in their metal packaging business in India. Because of their sustainability, new categories like whiskey, wine, and hard spirits have moved to aluminum cans.

- Beer enthusiasts and brewers have also recognized the benefits of cans in maintaining the quality and freshness of the beverage. Cans offer superior protection against light and oxygen, which can degrade beer over time. Additionally, metal cans are highly recyclable, requiring less energy than glass bottle recycling. As the region strives to build a greener future, the beer industry's shift toward cans aligns with the nation's sustainability goals.

- Furthermore, businesses are investing in the future of metal packaging because they understand the significant impact of choosing endlessly recyclable beverage packaging on communities and the environment. Companies actively seek expanded categories in India, encompassing a considerably broader range of alcoholic beverages. The companies also closely examine the regulatory developments and expect a favorable environment for cans.

- Engineering Exports Promotion Council India stated India's net export value for aluminum and related products in 2023 was USD 8.8 billion. Aluminum production will experience economies of scale and cost-effectiveness as its export value rises. This might lead to more affordable packaging options for alcoholic beverages, making it a more desirable choice for manufacturers.

- Alcohol producers operating across the region are focused on launching alcoholic beverages in new packages. For instance, in March 2024, United Breweries Limited (UBL) announced the launch of Queenfisher beer in cans. Queenfisher Beer is an all-women initiative, from formulating the limited-edition Queenfisher can brewing it by women brewers.

Beer is expected to take a significant share of the market.

- Beer consumption has risen in the last few years. With over 20 million people reaching the legal drinking age yearly, India remains one of the world's foremost beer markets. United Breweries, India's largest beer manufacturer and maker of the well-known Kingfisher brand, has recently released their latest Kingfisher Instant Beer. The product is packaged in a box with two sachets.

- The glass bottle with a crown closure is the traditional beer packaging in the region. Because glass is widely utilized in alcohol packaging, demand is likely to rise throughout the forecast period. Furthermore, glass prices substantially influence the margin profile of alcohol industries, which swings in response to crude oil price fluctuations.

- Furthermore, gluten-free beers are becoming increasingly popular in this region. Beer consumption is also increasing at over 6% per year in China, India, and Vietnam. As a result, rising innovation in tastes and preparations is anticipated to stimulate beer demand, resulting in beer cans' growth.

- According to the National Bureau of Statistics of China, close to 4 million kiloliters of beer was produced in China in July 2023 which was 2.54 million kiloliters in December 2022. Due to the increase in beer production, packaging businesses may spend money on R&D to develop creative and environmentally friendly packaging options. The quality and appeal of alcoholic beverage packaging in Asia will be improved through eco-friendly packaging, new designs, and materials.

- Moreover, in March 2024, Singapore-founded Lion Brewery Co. is elevating the country's craft beer presence on the global stage by breaking new ground. They are the first craft brewery to pioneer a canned nitro stout with in-line nitro technology and the first Singaporean craft beer to be distributed in Dubai. This marks the first time a Singaporean craft beer brand has produced a canned Nitro Stout beer.

APAC Alcoholic Drinks Packaging Industry Overview

The Asia-Pacific alcoholic drinks packaging market is moderate with the presence of major players. Some of the major players in the market are Amcor Group GmbH, Crown Holdings, Inc., Ball Corporation, AGI Glaspac, Berry Global Inc., and others. Some recent strategic initiatives made in this sector are:

August 2023 - Crown Holdings Inc. announced the acquisition of Helvetia Packaging AG, a beverage can and end manufacturing facility. The acquisition of the Saarlouis plant will expand Crown's beverage can network, with an annual capacity of around 1 billion units. As part of the agreement, Crown will take over the existing Helvetia customer base and associated contracts at closing.

July 2023 - Amcor Rigid Packaging (ARP) launched 100% recycled polyethylene terephthalate (rPET) packaging for Ron Rubin Winery's new BLUE BIN wine range. The range is 750 ml in a bottle. In addition to reducing greenhouse gas emissions compared to conventional wine packaging, rPET packaging offers many environmental advantages.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Force Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Sustainable Packaging

- 5.1.2 Increasing Consumption of Alcoholic Drinks in Asia

- 5.2 Market Restraints

- 5.2.1 Government Regulation for Plastic Usage

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Plastic

- 6.1.2 Paper

- 6.1.3 Metal

- 6.1.4 Glass

- 6.2 By Product Type

- 6.2.1 Bottles

- 6.2.2 Cans

- 6.2.3 Pouches

- 6.2.4 Carton

- 6.3 By Country

- 6.3.1 China

- 6.3.2 India

- 6.3.3 Japan

- 6.3.4 Singapore

- 6.3.5 Australia and New Zealand

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Group GmbH

- 7.1.2 Mondi Group

- 7.1.3 Crown Holdings, Inc.

- 7.1.4 Gerresheimer AG

- 7.1.5 Hualian Glass Bottle

- 7.1.6 Ball Corporation

- 7.1.7 AGI Glaspac

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

酒精包裝市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測

酒精包裝市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測 中東和非洲酒精飲料包裝市場佔有率分析、行業趨勢和成長預測(2025-2030 年)北美酒精飲料包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030)拉丁美洲酒精飲料包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)歐洲酒精飲料包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)美國酒精飲料包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

中東和非洲酒精飲料包裝市場佔有率分析、行業趨勢和成長預測(2025-2030 年)北美酒精飲料包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030)拉丁美洲酒精飲料包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)歐洲酒精飲料包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)美國酒精飲料包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 全球酒精飲料包裝市場 - 2025 年至 2030 年預測酒精飲料包裝市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測

全球酒精飲料包裝市場 - 2025 年至 2030 年預測酒精飲料包裝市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測 烈酒包裝市場:按產品類型分類的全球預測 - 2025-2030酒精包裝市場:按材料類型、應用分類 - 2025-2030 年全球預測

烈酒包裝市場:按產品類型分類的全球預測 - 2025-2030酒精包裝市場:按材料類型、應用分類 - 2025-2030 年全球預測