|

市場調查報告書

商品編碼

1640478

歐洲勞動力管理軟體市場:佔有率分析、產業趨勢和成長預測(2025-2030 年)Europe Workforce Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

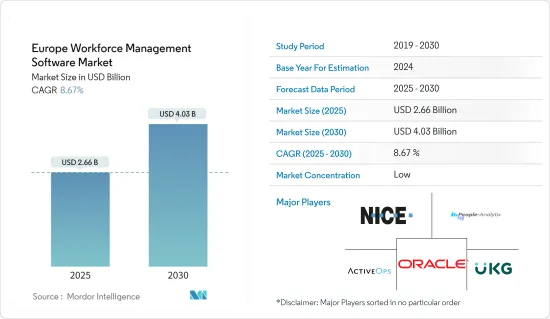

歐洲勞動力管理軟體市場規模預計在 2025 年為 26.6 億美元,預計到 2030 年將達到 40.3 億美元,預測期(2025-2030 年)的複合年成長率為 8.67%。

這一成長是由提高生產力以保持競爭優勢的需求以及與勞動力相關的標準日益複雜所推動的,這使得企業必須依靠 IT 解決方案來確保合規性。

主要亮點

- 鑑於職場的不斷發展,透過維護電子表格和記錄每項活動的記錄來管理員工隊伍已經變得非常耗時、繁瑣且容易出錯。勞動力管理軟體可以有效管理工作計畫、業務流程、人事費用和人才管理,進而最佳化組織績效。它還結合了分析和資料深入挖掘功能,為更好地管理人力資本提供更深入的見解。

- 過去十年,遠距工作趨勢一直穩定成長。然而,COVID-19 的影響在短時間內急劇加速了這一趨勢,迫使全部區域。由於疫情迫使更多人遠距工作,遠端勞動力管理軟體對於企業來說變得至關重要,因為它可以幫助企業有效地管理遠端勞動力。

- 私人公司透過私有雲端提供勞動力管理解決方案,以提供多層次的實體和邏輯安全功能。許多企業領導者轉向基於雲端基礎的勞動力管理的主要原因之一是希望獲得統一的解決方案。這包括銷售團隊、入境行銷軟體、行銷自動化軟體、勞動力管理軟體和業務分析工具等服務,以深入了解您企業的商業、業務和財務方面。

- 大多數 SaaS 評估專注於根據您目前的痛點衡量功能集並找到表現良好的供應商。但實施新的勞動力管理軟體可能是一個昂貴且耗時的過程,需要正確完成才能獲得任何組織所尋求的利益。

歐洲勞動力管理軟體市場趨勢

物聯網 (IoT) 和雲端基礎的解決方案的日益普及將推動市場成長

- 技術主導的勞動力管理系統提高了整體績效管理和分析能力。物聯網 (IoT) 就是這樣一種技術,它可以提高業務效率,從而提高員工績效,並將所有相關人員聚集在一個地方,以監督和簡化所有行動。物聯網的應用範圍從資產管理到勞動力自動化框架,以實現最高的工作效率。

- 各行業的企業之間的競爭日益激烈,並將在刺激歐洲成長和創造就業方面發揮關鍵作用。在歐洲,SD Worx 去年 10 月進行的一項調查發現,目前有六成的公司正在使用人力資源和人才分析來深入了解人才短缺和缺勤等領域。此外,21% 的受訪者表示他們希望在明年使用這些工具,比去年增加了 15%。

- 根據歐洲法院(ECJ)的一項裁決,現在歐洲各地的雇主都必須記錄員工的出勤情況。因此,歐洲法院裁定,成員國必須要求雇主建立記錄每日工作時間的製度。這些規定增加了對工作時間追蹤軟體的需求。

- 物聯網被認為是辦公室、家庭和工業領域最受歡迎的技術之一,各種合作和夥伴關係正在為勞動力管理市場的成長注入動力。根據 Good Companies 的報告,大約 34% 的歐洲企業正在其業務流程中使用物聯網,另有 12% 的企業計劃很快這樣做。此外,正如歐盟委員會所指出的,許多本地公司正在選擇雲端處理,如圖所示。

- 例如,歐洲領先的診斷服務供應商 Unilabs 在去年 5 月為其瑞士業務選擇了基於雲端的 ATOSS 勞動力管理。不同州的所有 62 個地點都將連結到該軟體。該計劃旨在將員工納入工作時間管理流程,為研究所帶來更靈活的工作安排,同時提高與工作時間相關的所有事項的透明度。

英國可望佔據主要市場佔有率

- 全國各地企業/組織對適應性和靈活性的需求不斷成長,以及組織對提高工作效率和改善員工體驗的日益關注,預計將推動英國地區研究市場的成長。

- 私部門的就業也在增加,迫使許多組織,特別是人力資源部門,採用勞動力管理解決方案來管理各種職能。

- 製造業、旅遊和運輸業以及零售業正在迅速擴張,並在這些管理軟體系統的採用率方面引領市場,從而推動了所研究市場的成長。此外,提高生產力對於任何組織的成功至關重要。公司努力提高員工生產力、降低成本並提高業務流程的效率。

- 疫情帶來的遠距辦公轉變正在支持英國對公共雲端服務日益成長的需求。英國企業正在轉向雲端服務來實現遠距工作環境中所需的勞動力和業務流程的自動化。

- 尤其是醫療保健產業,在實施勞動力調度軟體方面投入了大量資金。例如,2021 年 1 月,護理部長宣布撥款 1,030 萬美元支持 38 個 NHS 信託機構進行數位化轉變組織,使工作人員能夠花更多時間與病患相處。該投資是3570萬美元國家基金的一部分,用於為所有 NHS 醫生、護士和其他臨床工作人員建立電子排班系統。

- 去年 3 月,英國政府啟動了一系列軟體和雲端服務契約,總價值可能達到 50 億英鎊(65.8 億美元)。在 GCloud13 的支持下,中央政府採購機構皇家商業服務局 (CCS) 已針對同名蓬鬆計算模型下的幾種技術發布了競標。

- 此外,該國正在推出許多新的勞動力管理解決方案。例如,去年 6 月,人力資源和薪資服務供應商SD Worx 推出了其歐洲市場領先的勞動力管理解決方案,為英國企業提供支援。 SD Worx 成為英國第一家提供完全整合勞動力管理 (WFM) SaaS 解決方案的薪資和人力資源供應商,該解決方案具有獨立 WFM 產品的所有功能。

歐洲勞動力管理軟體產業概況

歐洲勞動力管理軟體市場的競爭格局非常活躍。市場上沒有主導者,需要增強凝聚力。不斷變化的終端用戶行業需求正在推動市場創新。

- 2022 年 7 月 - SD Worx 收購位於克羅埃西亞薩格勒布的人力資源科技公司 HRPRO。透過此次收購,SD Worx 將其本地業務擴展到 18 個歐洲國家並進入東南歐市場,該公司認為該地區具有巨大的成長潛力,可以增強薪資核算和人力資源軟體產品組合。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 購買者/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 市場影響評估

第5章 市場動態

- 市場促進因素

- 物聯網 (IoT) 和雲端基礎的解決方案的日益普及將推動市場成長

- 中小企業擴大採用分析解決方案和 WFM 將推動市場成長

- 市場挑戰

- 實施和整合問題阻礙市場

第6章 市場細分

- 依部署方式

- 本地

- 雲

- 按組織規模

- 中小企業

- 大型企業

- 按類型

- 勞動力調度和勞動力分析

- 考勤管理

- 績效與目標管理

- 缺勤和休假管理

- 其他軟體(疲勞管理、任務管理等)

- 按最終用戶產業

- 衛生保健

- BFSI

- 製造業

- 消費品和零售

- 其他最終用戶產業

- 按國家

- 英國

- 法國

- 德國

- 西班牙

- 比荷盧

- 其他歐洲國家

第7章 競爭格局

- 公司簡介

- Active Operations Management International LLP

- NICE Systems Ltd.

- Oracle Corporation

- Ultimate Kronos Group

- People-Analytix AG

- Avature Company

- Talentsoft AG

- WorkForce Software LLC

- Workday Inc.

- Atos Software AG

- Quinyx AB

- IBM Corporation

- SAP SE

- ADP LLC

- Reflexis Systems Inc.

- SISQUAL Workforce Management Lda

- Zucchetti SpA

- Anviz Global Inc.

- Calabrio Inc.

- Tamigo UK Ltd.

- SD Worx Group NV

- MYOB(Roubler)UK Limited Company

- Sage Group PLC

- Mitrefinch Ltd.

第8章投資分析

第9章:市場的未來

The Europe Workforce Management Software Market size is estimated at USD 2.66 billion in 2025, and is expected to reach USD 4.03 billion by 2030, at a CAGR of 8.67% during the forecast period (2025-2030).

The growth is primarily driven by the need for improved productivity to maintain competitive advantage and the growing complexity of workforce-related standards, making it imperative for firms to rely on IT solutions to ensure compliance.

Key Highlights

- Given the evolving workplace nature, managing the workforce by maintaining spreadsheets and registers for all activities became highly time-consuming, cumbersome, and prone to errors. Workforce management software is essential in optimizing organizational performance by enabling effective administration of work schedules, business processes, labor costs, and talent management. Embedded with analytics and drill-down features for the data, it provides even deeper insights for better human capital management.

- The trend toward remote work is steadily growing for the past decade. However, the COVID-19 effect dramatically accelerated this trend in a brief period, forcing companies, irrespective of their size, to adapt quickly to the self-isolation measures that governments across the region were recommending. With the pandemic requiring more people to work remotely, remote workforce management software became essential for companies, as this software can help manage the remote workforce efficiently.

- Various companies offer workforce management solutions through the private cloud to provide multi-level physical and logical security features. One of the primary reasons for the inclination of many business leaders toward cloud-based workforce management is the desire to get in one solution. It may include services like salesforce, inbound marketing software, marketing automation software, workforce management software, and business analytical tools to achieve insights into commercial, operational, and financial aspects.

- Most software-as-a-service evaluations focus on measuring feature sets against any current problem areas and finding a vendor to work well. However, implementing new workforce management software can be an expensive and time-consuming process, one that needs to be performed right to reap the benefits that any organization seeks.

Europe Workforce Management Software Market Trends

Increasing Adoption of Internet of Things (IoT) and Cloud-based Solutions is Expanding the Market

- A technology-driven workforce management system improves overall performance management and analytics. The internet of things(IoT) is one such technology that increases the efficiency of operations, thereby increasing workforce performance to bring together all stakeholders on a single platform to supervise and streamline all actions. The applications of IoT range from asset management to automated frameworks of the workforce to bring out the best work rate.

- The competition among companies in every sector is becoming so intense and should play an important part in stimulating growth and job creation in Europe. In Europe, a survey by SD Worx in October last year shows that six out of ten companies today use HR and people analytics to gain insights into areas such as staff shortages and absenteeism. Also, 21% of those surveyed indicated they would like to start using these tools in the coming year, a 15% increase from last year.

- Employers across Europe are now obliged to track their employees' time and attendance following a ruling by the European Court of Justice (ECJ). As a result, the ECJ ruled that member states must oblige employers to set up a system for the daily recording of working time. Such regulation increased the demand for workforce management software.

- IoT is considered one of the most trending technologies being used in offices, homes, and industries, and various collaborations and partnerships are gaining momentum for market growth in workforce management. As per the report by Good firms, around 34% of organizations in Europe are using IoT for their business processes, and another 12% are planning to do so shortly. Further, as indicated by the European Commission, many regional enterprises opt for cloud computing, as shown in the graph.

- For instance, in May of the previous year, Unilabs, Europe's leading diagnostics service provider, opted for ATOSS workforce management in the cloud for its activities in Switzerland. All 62 sites in different cantons will be linked to the software. The project aims to integrate employees into the working time management processes and achieve more flexible duty scheduling in the laboratories while creating greater transparency in all matters revolving around working hours.

United Kingdom is Expected to Hold Significant Market Share

- The increasing demand from businesses/organizations across the country for adaptability and flexibility and the organization's rising focus on increasing workforce productivity and improved employee experience are expected to drive the studied market growth in the United Kingdom region.

- Employment in the private sector is also increasing, forcing many organizations, especially human resource management departments, to adopt workforce management solutions to manage various functions.

- The Manufacturing, Travel & Transport, and Retail sectors are expanding rapidly, leading the market in terms of the adoption rate of these management software systems, thus driving the studied market growth. Further, good productivity is crucial for the success of any organization. Enterprises are striving hard to enhance the productivity of their employees, reduce costs, and improve business process efficiency.

- The continued transition to remote working brought on by the pandemic helped to sustain the growing demand for public cloud services in the UK. To automate labor and business processes necessary for remote work environments, businesses in the UK are increasingly turning to cloud services.

- The country is witnessing significant investment in the deployment of workforce scheduling software, especially in the healthcare sector. For instance, in January 2021, the Minister of Care announced USD 10.3 million to support digital shift organizing across 38 NHS trusts, allowing staff to spend more time with patients. The investment is part of a USD 35.7 million national fund for all NHS doctors, nurses, and other clinical staff on e-rostering systems.

- In March last year, the UK government initiated an agreement series for software and cloud services that could total up to GBP 5 billion (USD 6.58 billion). The tender for several technologies under the fluffy eponymous computing model is released by the central government procurement authority Crown Commercial Services (CCS) under the aegis of G-Cloud 13.

- The country is also witnessing the launch of many new workforce management solutions. For instance, in June previous year, SD Worx, an HR and payroll services provider, empowered UK businesses with the launch of its European market-leading workforce management solution. SD Worx became the first UK Payroll and HR provider to offer a fully integrated workforce management (WFM) SaaS solution with all the capabilities of a stand-alone WFM product.

Europe Workforce Management Software Industry Overview

The competitive landscape for the European workforce management software market is very dynamic. The market needs to be more cohesive without any dominant player. The evolving needs of the end-user industries are driving innovations in the market.

- July 2022 - SD Worx acquired HRPRO, an HR tech company located in Zagreb, Croatia. With this acquisition, SD Worx will expand its local presence to 18 European countries and enter Southeastern Europe, where it sees a lot of growth potential in strengthening its payroll & HR software portfolio.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the COVID-19 Impact on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Internet of Things (IoT) and Cloud-based Solutions is Expanding the Market

- 5.1.2 Growing Adoption of Analytical Solutions and WFM by SMEs is Driving the Market Growth

- 5.2 Market Challenges

- 5.2.1 Implementation and Integration Concerns Hindering the Market

6 MARKET SEGMENTATION

- 6.1 By Deployment Mode

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.2 By Size of Organization

- 6.2.1 Small and Medium Enterprises

- 6.2.2 Large Enterprises

- 6.3 By Type

- 6.3.1 Workforce Scheduling and Workforce Analytics

- 6.3.2 Time and Attendance Management

- 6.3.3 Performance and Goal Management

- 6.3.4 Absence and Leave Management

- 6.3.5 Other Software (Fatigue Management, Task Management, etc)

- 6.4 By End-user Industry

- 6.4.1 Healthcare

- 6.4.2 BFSI

- 6.4.3 Manufacturing

- 6.4.4 Consumer Goods and Retail

- 6.4.5 Other End-user Industries

- 6.5 By Country

- 6.5.1 United Kingdom

- 6.5.2 France

- 6.5.3 Germany

- 6.5.4 Spain

- 6.5.5 Benelux

- 6.5.6 Rest of Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Active Operations Management International LLP

- 7.1.2 NICE Systems Ltd.

- 7.1.3 Oracle Corporation

- 7.1.4 Ultimate Kronos Group

- 7.1.5 People-Analytix AG

- 7.1.6 Avature Company

- 7.1.7 Talentsoft AG

- 7.1.8 WorkForce Software LLC

- 7.1.9 Workday Inc.

- 7.1.10 Atos Software AG

- 7.1.11 Quinyx AB

- 7.1.12 IBM Corporation

- 7.1.13 SAP SE

- 7.1.14 ADP LLC

- 7.1.15 Reflexis Systems Inc.

- 7.1.16 SISQUAL Workforce Management Lda

- 7.1.17 Zucchetti SpA

- 7.1.18 Anviz Global Inc.

- 7.1.19 Calabrio Inc.

- 7.1.20 Tamigo UK Ltd.

- 7.1.21 SD Worx Group NV

- 7.1.22 MYOB (Roubler) UK Limited Company

- 7.1.23 Sage Group PLC

- 7.1.24 Mitrefinch Ltd.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2025年行動工作人員管理全球市場報告2025年全球醫療保健勞動力管理系統市場報告

2025年行動工作人員管理全球市場報告2025年全球醫療保健勞動力管理系統市場報告 勞動力管理市場規模、佔有率和成長分析(按組件類型、部署、公司、解決方案、最終用戶產業和地區)- 產業預測 2025-2032

勞動力管理市場規模、佔有率和成長分析(按組件類型、部署、公司、解決方案、最終用戶產業和地區)- 產業預測 2025-2032 全球醫療保健勞動力管理系統市場趨勢、競爭格局和預測(2019-2031 年)- 按解決方案、交付類型、最終用戶和地區分類

全球醫療保健勞動力管理系統市場趨勢、競爭格局和預測(2019-2031 年)- 按解決方案、交付類型、最終用戶和地區分類 中東和非洲勞動力管理軟體:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)亞太地區人力資源管理軟體市場:佔有率分析、產業趨勢和成長預測(2025-2030 年)北美勞動力管理軟體:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)拉丁美洲勞動力管理軟體:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

中東和非洲勞動力管理軟體:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)亞太地區人力資源管理軟體市場:佔有率分析、產業趨勢和成長預測(2025-2030 年)北美勞動力管理軟體:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)拉丁美洲勞動力管理軟體:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 勞動力管理軟體市場,全球 2025-2029

勞動力管理軟體市場,全球 2025-2029 市場佔有率與預測:勞動力管理軟體(WMS),全球,2023年至2028年(2 份報告合集)

市場佔有率與預測:勞動力管理軟體(WMS),全球,2023年至2028年(2 份報告合集)