|

市場調查報告書

商品編碼

1644866

美國設施管理:市場佔有率分析、產業趨勢、統計數據、成長預測(2025-2030 年)United States Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

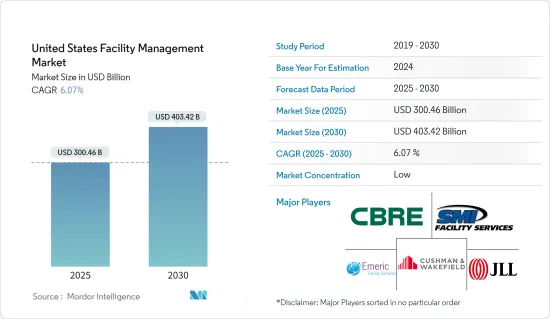

美國設施管理市場規模預計在 2025 年為 3,004.6 億美元,預計到 2030 年將達到 4,034.2 億美元,預測期內(2025-2030 年)的複合年成長率為 6.07%。

推動美國設施管理服務市場成長的關鍵因素之一是對內部和外包設施管理的各種客製化解決方案的需求激增。

主要亮點

- 美國各大城市的住宅和商業建築數量不斷增加,對設施管理服務的需求也日益成長。預計,人們對綜合設施管理服務的日益關注和基礎設施建設的進步將對市場產生積極影響。

- 為了跟上不斷變化的科技時代,機器人設備監控和與物聯網結合的擴增實境等工具在國內正在穩步增加。因此,越來越多的軟體供應商正在加強技術創新,為設施管理市場的人工智慧和機器人創造空間。

- 2023 年 3 月,設施服務、基礎設施解決方案和停車管理提供者 ABM 簽署了一份多年期契約,為 Tropicana Field 和 Al Lang Stadium 提供優質的客房服務解決方案,並管理日常業務和活動人員。透過此次夥伴關係,ABM 將作為單一供應商,為兩個體育場超過 100 萬平方英尺的空間配備專業清潔人員,致力於提供清潔服務,提升球迷體驗。

- 根據美國人口普查局的數據,2023年11月的總建築支出經季節性已調整的後年化率預計約為2.0501兆美元,較10月份修訂後的2.0425兆美元成長0.4%。預計整體建築支出的增加將為市場創造巨大的成長機會。

- 限制該市場成長的主要因素之一是對設備和網路安全的安全問題。預計,在整個預測期內,日益增多的安全漏洞和有組織犯罪集團的威脅將阻礙市場的成長。

美國設施管理市場趨勢

增加對醫療基礎設施和醫療設施建設的投資

- 隨著患者數量的不斷成長以及公共和私人醫療支出的不斷上升,醫療保健已成為美國最重要的行業之一。根據美國醫療補助服務中心和醫療保險中心提供的資料,2018年至2027年間,美國全國醫療保健支出預計將以每年5.5%的速度成長,達到約6兆美元。

- 醫療保健支出的快速成長導致了醫院和診所中許多不同類型的護理設施的發展。此外,美國醫療保健產業設施管理服務的外包顯著增加,包括療養院、醫院和第三方專家。因此,醫療保健產業對設施管理服務的需求日益增加。

- 醫療保健機構每天都會產生大量有害和無害廢棄物。如果處理不當,危險廢棄物可能會影響患者照護的品質。它還會導致環境污染和感染疾病的傳播。

- 在美國,Medxcel 是規模最大、最受推崇的醫療設施服務提供者之一。在過去四年中,Medxcel 已為其客戶節省了 8,000 萬美元的設施管理費用。

- 根據美國國家人口問題研究所的人口快報《美國老化》,到 2060 年,美國總數預計將達到約 9,500 萬人。大多數老年人面臨精神疾病、慢性病、傷害和殘疾。美國醫療保健產業面臨著提供優質護理、高科技醫療設備以及滿足新的消費者偏好的壓力。

商業領域推動市場需求

- 商業建築旨在透過新建築(主要是辦公室和工業設施)開展業務。服務提供者主要提供建築物的整個基本基礎設施,包括電梯維護、建築維修、窗戶清潔、油漆、門和天花板護理等。

- 在職場,智慧建築技術在協助設施管理人員創造更節能、更舒適的環境、管理建築資產和系統以及規劃未來需求方面發揮關鍵作用。

- 2023 年 11 月,建築領域的 3D數位雙胞胎平台供應商 Matterport Inc. 和網路基礎設施數位化解決方案的全球供應商 Belden Inc. 建立了新的夥伴關係,為工業自動化、智慧建築、寬頻和設施管理提供支援 3D數位雙胞胎的連接解決方案。

- 多年來,具有永續IT基礎設施的彈性工作空間在美國東北部得到了顯著發展。該地區擁有一些最清潔的機制、計劃和政策,鼓勵採用綠色技術。由於「綠色清潔技術」越來越受歡迎,美國的專業清潔服務正在經歷顯著成長。使用涉及專門化學品、設備和技術的永續清洗產品是推動整個市場成長的關鍵因素。

- 零售業設施管理的主要職責是保持商店區域清潔、安全和有吸引力。 NEST 的零售客戶表示,在 COVID-19 疫情期間,他們的客流量超出了預期。 NEST 在美國和加拿大管理 60,000 家零售店,其中大部分位於美國。 NEST 提供將財務洞察和業務分析與糾正性和預防性維護整體諮詢方法相結合的綜合解決方案。

美國設施管理產業概況

由於本地和全球領先公司的存在,美國設施管理市場比較分散。設施管理服務需求的不斷成長預計將吸引更多參與者並加劇競爭。 Compass Group PLC、Sodexo Inc.、CBRE Group Inc.、Ingersoll Rand (Trane)、Ecolab、ISS Facilities Services Inc.、G4S PLC、Jones Lang LaSalle Incorporated (JLL)、EMCOR Group Inc. 和 Cushman &Wakefield 是市場上一些知名的參與者。

- 2024 年 1 月,世邦魏理仕集團 (CBRE Group Inc.) 和 Brookfield Properties 宣佈建立策略夥伴關係,將利用兩家公司的綜合優勢來提高租戶滿意度和物業表現。透過此次合作,世邦魏理仕與 Brookfield Properties 將相互提供全方位的物業管理服務,包括為全美超過 6,500 萬平方英尺的辦公空間提供建設業務、物業會計、採購業務和技術支援。

- 2024 年 1 月,Cushman & Wakefield 的另類專業資產管理部門 Nuvama Wealth Management Limited 和 Nuvama Asset Management 宣布由 Nuvama 與 Cushman & Wakefield Management Private Limited(「NCW」)成立新的 50:50 合資營業單位。新公司將成為強大的商業房地產投資全方位服務平台。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 購買者/消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 宏觀經濟因素對產業的影響

第5章 市場動態

- 市場促進因素

- 美國醫療基礎設施投資和醫療建設增加

- 商業建築對建築資訊模型 (BIM) 的需求

- 市場限制

- 資料外洩和安全威脅日益增多

第6章 市場細分

- 設施管理類型

- 內部設施管理

- 外包設施管理

- 單調頻

- 捆綁 FM

- 整合調頻

- 按服務

- 硬體維修

- 軟調頻

- 按最終用戶

- 商業

- 設施

- 公共/基礎設施

- 工業的

- 其他最終用戶

第7章 競爭格局

- 公司簡介

- CBRE Group Inc.

- Jones Lang LaSalle Incorporated

- Cushman & Wakefield PLC

- Emeric Facility Services

- SMI Facility Services

- Sodexo Inc.

- AHI Facility Services Inc.

- ISS Facility Services Inc.

- Shine Management & Facility Services

- Guardian Service Industries Inc.

第8章投資分析

第9章:未來市場展望

The United States Facility Management Market size is estimated at USD 300.46 billion in 2025, and is expected to reach USD 403.42 billion by 2030, at a CAGR of 6.07% during the forecast period (2025-2030).

The surge in demand for various customized solutions for different in-house and outsourced facility management is one of the significant factors driving the growth of the facility management service market in the United States.

Key Highlights

- The growing number of residential and commercial buildings in major cities is enhancing the overall need for facility management services throughout the country. With an increase in focus on integrated facility management services and the rising developments in the infrastructure, the market is expected to experience a positive impact.

- To comply with the changing technological age, tools like robot facility monitoring and augmented reality that are integrated with IoT are steadily increasing in the country. Hence, more and more software providers are now committed to innovation, making room for AI and robotics in the facility management market.

- In March 2023, ABM, a provider of facility services, infrastructure solutions, and parking management, signed a multi-year agreement to provide first-class housekeeping solutions and to manage day-to-day and event staffing for Tropicana Field and Al Lang Stadium. With this partnership, ABM would serve as a single source for deploying a professional workforce that is mainly dedicated to delivering janitorial services that augment the fan experience across over one million square feet of stadium space at the venues.

- According to the US Census Bureau, total construction spending in November 2023 was estimated at a seasonally adjusted annual rate of approximately USD 2,050.1 billion, up by 0.4% from October's revised figure of USD 2,042.5 billion. This rise in overall construction spending is expected to amplify the market's growth opportunities significantly.

- One of the key factors limiting the growth of this market is safety concerns related to device and network security. A growing number of security breaches and the increased threats posed by organized crime groups are expected to hamper the market's growth throughout the forecast period.

United States Facility Management Market Trends

Increasing Investments in Healthcare Infrastructure and the Construction of Healthcare Facilities

- Due to a growing number of patients and higher healthcare expenditures by the public and private players, healthcare has become one of the most important sectors within the United States. It is estimated that national healthcare spending will increase at an annual rate of 5.5% from 2018 to 2027 in the United States, reaching approximately USD 6 trillion, according to data provided by the Centers for Medicaid Services and Medicare.

- The extraordinary growth in healthcare spending led to the development of a number of different types of care facilities at hospitals and clinics. In addition, the outsourcing of facility management services by healthcare sectors, such as nursing homes, hospitals, and third-party professionals, has significantly increased in the United States. As a result, the demand for facility management services in the healthcare industry has increased.

- Healthcare facilities generate a large volume of both hazardous and non-hazardous waste daily. The quality of patient care may be compromised by hazardous waste if not properly handled. It may cause environmental pollution and the spread of infections.

- In the United States, Medxcel is one of the biggest and most respected providers of healthcare facility services. Over the past four years, Medxcel has provided customers with savings of USD 80 million on facility management expenditures.

- As per the Population Reference Bureau's Population Bulletin, "Aging in the United States," the overall number of Americans who are aged 65 and above is predicted to reach around 95 million by 2060. The majority of elders face mental illnesses, chronic diseases, injuries, and disabilities. The healthcare sector in the United States is under pressure to provide quality care services, high-technology healthcare equipment, and respond to new consumer preferences.

Commercial Segment to Drive Major Market Demand

- Commercial construction is mainly for the purpose of business through new buildings like offices or a new industrial facility. A service provider mainly provides the entire basic infrastructure of the building, which includes maintenance of lifts, building repair, cleaning of windows, painting, and care of doors, ceilings, and many more.

- In the workplace, smart building technology also plays a key role in assisting facilities managers in building a more energy-efficient, comfortable environment, managing building assets and systems, and planning for future needs.

- In November 2023, Matterport Inc., the 3D digital twin platform provider for the built world, and Belden Inc., a worldwide supplier of network infrastructure and digitization solutions, signed a new partnership with the aim to provide 3D digital twin-powered connectivity solutions for facilities management across industrial automation, smart buildings, broadband, and many others.

- Flexible workspaces with sustainable IT infrastructure have grown significantly in the northeastern United States over the years. The region has the cleanest mechanisms, programs, and policies that augment the adoption of green technology. The US professional cleaning services are experiencing tremendous growth on account of the amplified popularity of "green cleaning technology." The use of sustainable washing agents, which involve special chemicals, equipment, and techniques, is a key factor aiding the overall growth of the market.

- The prime responsibility for facilities management in the retail sector involves keeping the store area clean, safe, and attractive. The retail clients of NEST stated that they received more foot traffic than expected during the COVID-19 pandemic. NEST manages 60,000 retail locations throughout the United States and Canada, with the majority in the United States, and provides an integrated solution that pairs financial acumen and business analytics with an overall consultative approach for both reactive and preventative maintenance.

United States Facility Management Industry Overview

The US facility management market is fragmented owing to the presence of major local and global players. The growing demand for facility management services is expected to attract more players, which will intensify the competition. Compass Group PLC, Sodexo Inc., CBRE Group Inc., Ingersoll Rand (Trane), Ecolab, ISS Facilities Services Inc., G4S PLC, Jones Lang LaSalle Incorporated (JLL), EMCOR Group Inc., and Cushman & Wakefield are some of the notable players in the market.

- In January 2024, CBRE Group Inc. and Brookfield Properties announced a strategic partnership that leverages the combined power of both firms to drive tenant satisfaction and property performance. The partnership will allow CBRE and Brookfield Properties to provide one another with a full range of real estate management services for more than 65 million square feet of office space in the United States, which include construction operations, property accounting, procurement work, and technology support.

- In January 2024, Nuvama Asset Management, the alternatives-focused asset management arm of Nuvama Wealth Management Ltd and Cushman & Wakefield, announced the formation of a new 50:50 joint venture entity, Nuvama and Cushman & Wakefield Management Private Limited ("NCW"). The new entity will act as a powerful platform offering a full suite of capabilities for investing in commercial real estate.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Force Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of Macro-Economic Factors on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Investments in Healthcare Infrastructure and the Construction of Healthcare Facilities in the United States

- 5.1.2 Requirement of Building Information Modeling (BIM) in Commercial Buildings

- 5.2 Market Restraints

- 5.2.1 Increased instances of Data Breaches and Security Threats

6 MARKET SEGMENTATION

- 6.1 By Type of Facility Management Type

- 6.1.1 Inhouse Facility Management

- 6.1.2 Outsourced Facility Mangement

- 6.1.2.1 Single FM

- 6.1.2.2 Bundled FM

- 6.1.2.3 Integrated FM

- 6.2 By Offerings

- 6.2.1 Hard FM

- 6.2.2 Soft FM

- 6.3 By End User

- 6.3.1 Commercial

- 6.3.2 Institutional

- 6.3.3 Public/Infrastructure

- 6.3.4 Industrial

- 6.3.5 Other End Users

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 CBRE Group Inc.

- 7.1.2 Jones Lang LaSalle Incorporated

- 7.1.3 Cushman & Wakefield PLC

- 7.1.4 Emeric Facility Services

- 7.1.5 SMI Facility Services

- 7.1.6 Sodexo Inc.

- 7.1.7 AHI Facility Services Inc.

- 7.1.8 ISS Facility Services Inc.

- 7.1.9 Shine Management & Facility Services

- 7.1.10 Guardian Service Industries Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

印尼的設施管理市場:各類型,模式別,各產業類型,各終端用戶,各地區,機會,預測,2018年~2032年日本的設施管理市場:各類型,模式別,各產業類型,各終端用戶,各地區,機會,預測,2018年~2032年義大利設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)英國設施管理產業:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)菲律賓設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)設施管理的泰國市場評估:各類型,模式別,各產業類型,各終端用戶,各地區,機會,預測(2018年~2032年)

印尼的設施管理市場:各類型,模式別,各產業類型,各終端用戶,各地區,機會,預測,2018年~2032年日本的設施管理市場:各類型,模式別,各產業類型,各終端用戶,各地區,機會,預測,2018年~2032年義大利設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)英國設施管理產業:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)菲律賓設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)設施管理的泰國市場評估:各類型,模式別,各產業類型,各終端用戶,各地區,機會,預測(2018年~2032年) 精神服務市場-全球產業分析、規模、佔有率、成長、趨勢及預測(2025-2035)

精神服務市場-全球產業分析、規模、佔有率、成長、趨勢及預測(2025-2035) 全球整合性機構管理(IFM) 市場:產業分析、規模、佔有率、成長、趨勢與預測(2025-2032 年)2025 年設施管理服務全球市場報告2018 年至 2032 年全球綜合設施管理市場類型、服務前景、最終用戶、地區、機會和預測評估

全球整合性機構管理(IFM) 市場:產業分析、規模、佔有率、成長、趨勢與預測(2025-2032 年)2025 年設施管理服務全球市場報告2018 年至 2032 年全球綜合設施管理市場類型、服務前景、最終用戶、地區、機會和預測評估