|

市場調查報告書

商品編碼

1651059

北美郵政服務:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)North America Postal Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

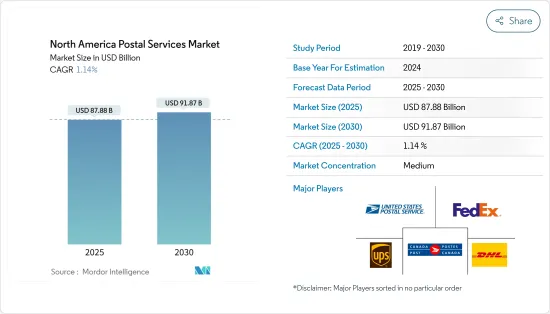

北美郵政服務市場規模預計在 2025 年為 878.8 億美元,預計到 2030 年將達到 918.7 億美元,預測期內(2025-2030 年)的複合年成長率為 1.14%。

主要亮點

- 在北美,數位通訊的興起正在減少傳統郵件的數量。同時,電子商務的興起也刺激了宅配和最後一哩路物流的需求增加。這些相互關聯的趨勢正在改變郵政業,迫使郵政業者擴大服務並實現業務現代化。美國郵政服務(USPS)是美國官方郵政營業單位。與美國郵政快遞直接競爭的聯邦快遞和聯合包裹服務公司 (UPS) 都提供緊急信件和小包裹的全國遞送服務。

- 美國郵政局利用其壟斷權力,限制其他宅配業者投遞非緊急信件,並禁止將其運送到美國住宅和商業地點的郵箱。除少數例外,美國郵政總局對信件投遞享有合法壟斷權,並受到私人快捷郵件法規的支持,根據該法規,私人郵遞員將面臨罰款,甚至監禁。在加拿大,加拿大郵政佔據主導地位,處理大部分小包裹和傳統郵件。該政府營運的服務受到許多加拿大人的信賴,每三個小包裹中就有兩個由該政府寄送。

- 2023年,美國小包裹收入將出現七年來首次下降,從2022年的1,984億美元降至1,979億美元。儘管小包裹總出貨量從 2022 年的 215 億件小幅成長 0.5% 至 2023 年的 217 億件,但仍出現了這一下降。根據年度美國宅配運輸指數,在四大運輸提供商(美國郵政服務、亞馬遜物流、UPS和聯邦快遞)中,僅亞馬遜物流錄得顯著成長,與前一年同期比較成長了15.7%。此外,亞馬遜物流在小包裹數量上已經超越聯邦快遞和UPS,並正在迅速接近市場領導USPS。消息人士稱,「其他」類別包括規模較小的承運商,其銷量和包裹數量將實現強勁成長,其市場佔有率將增加 28.5%,到 2023 年達到約 3%(約 6 億件小包裹)。消息人士透露,2023年USPS將成為最大的小包裹處理公司,包裹數量為66億件(與前一年同期比較下降約1%),其次是亞馬遜物流,包裹數量為59億件(比上年成長15.7%),UPS,包裹數量為46億件(比上年下降10.3%),聯邦快遞件數量為396.196.1666.666.666.6666.66.66.66.66.66.666.4666.66.46.266.26.26.26.26.26.296.96.26.96)。

- 近年來,北美郵政服務業面臨數位化顛覆。隨著越來越多的交流轉移到線上,傳統的郵政投遞業務正在穩步下滑。同時,隨著電商小包裹市場的不斷擴大,產業競爭也愈發激烈。因此,郵政和郵寄營業單位正在從國有壟斷企業演變為擁有多元化投資組合的營利性公司。

北美郵政服務市場趨勢

美國在市場上有明顯優勢

疫情爆發後,美國電子商務經歷了前所未有的成長,與許多其他國家的趨勢相似。美國人口為3.32億,是繼印度和中國之後世界第三人口大國。值得注意的是,近80%的美國網友在網路購物。電子商務的激增為郵政服務帶來了巨大的機會。隨著消費者擴大轉向新興的電子商務平台和傳統的線上實體店,對高效的配送和收集管道的需求也日益成長。透過利用其已建立的全國網路和最後一哩投遞專業知識,郵政服務將自己定位為這個不斷發展的環境中寶貴的合作夥伴。到2024年第二季度,美國電子商務銷售額將達到2,916.4億美元,佔零售總額的15.9%。今年上半年美國電子商務銷售額飆升至 5,794.5 億美元,一些預測預計到年終將達到 1.22 兆美元。電子商務的持續成長凸顯了郵政服務在支持數位經濟方面的重要作用。

信件數量正在下降

美國郵政服務(USPS)是美國官方郵政管理機構。自 2006 年達到約 2,130 億件的峰值以來,USPS 的郵件數量每年都在持續下降。到 2023 年,包裹遞送量將驟降至僅 1,161.5 億件。下降主要是由於傳統郵件、行銷資料和出版刊物的數量減少。相較之下,小包裹遞送的收入卻大幅成長。這種轉變的主要催化劑是技術。隨著越來越多的美國人使用電子郵件,對傳統郵件的需求減少。此外,美國的線上零售額在過去十年中加倍,增加了小包裹遞送的需求。加拿大官方郵政服務加拿大郵政也反映了這一趨勢。

北美郵政服務業概況

目前該行業比較分散。大公司因其廣泛的基礎設施和服務多樣性而具有優勢。小企業透過專業化進行競爭。國營郵局通常壟斷郵件投遞,但面臨來自私人包裹投遞公司的激烈競爭。競爭營業單位結盟,以發揮彼此的優勢。例如,大型快捷郵件公司聯邦快遞(FedEx)和聯合包裹服務公司(UPS)委託某些住宅快遞業務外包給美國郵政服務(USPS),而USPS委託空運業務外包給FedEx和UPS。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態與洞察

- 當前市場狀況

- 市場促進因素

- 電子商務成長

- 擴大當日及隔日送達服務

- 市場限制

- 人事費用上升

- 網路安全和電子郵件安全

- 市場機會

- 自動化和技術改進

- 價值鏈/供應鏈分析

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 購買者/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第5章 市場區隔

- 按類型

- 快捷郵件專遞服務

- 標準郵政服務

- 按項目

- 信

- 小包裹

- 按目的地

- 國內的

- 國際的

- 按地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭格局

- 市場集中度概覽

- 公司簡介

- USPS

- Canada Post Corporation

- UPS

- DHL

- FedEX

- Purolator

- Correos de Mexico

- Estafeta

- GLS

- APC Postal Logistics

- Santa Lucia Post

- Grenada Postal Corporation

- Paquetexpress

第7章:市場的未來

第 8 章 附錄

- 總體經濟指標

- 運輸和倉儲對GDP的貢獻

The North America Postal Services Market size is estimated at USD 87.88 billion in 2025, and is expected to reach USD 91.87 billion by 2030, at a CAGR of 1.14% during the forecast period (2025-2030).

Key Highlights

- In North America, the rise of digital communication has diminished the volume of traditional mail. At the same time, the flourishing e-commerce sector has spurred greater demand for parcel delivery and last-mile logistics. These interconnected trends are transforming the industry, prompting postal operators to expand their services and modernize their operations. The United States Postal Service (USPS) is the official postal entity in the USA. FedEx and UPS, in direct competition with USPS's Express Mail, provide nationwide delivery services for urgent letters and packages.

- Leveraging its monopoly, USPS restricts other U.S. couriers from delivering non-urgent letters and prohibits them from shipping to U.S. mailboxes at residential and business locations. With few exceptions, USPS maintains a legal monopoly on letter delivery, backed by the Private Express Statutes, which impose fines and potential imprisonment on private letter carriers. In Canada, Canada Post is the dominant player, overseeing the majority of both package and traditional mail shipments. This government-run service enjoys the trust of many Canadians, managing the shipment of two out of every three parcels.

- In 2023, US parcel revenue saw its first dip in seven years, falling from USD198.4bn in 2022 to USD197.9bn. This decline came despite a modest 0.5% uptick in total parcel volume, which rose from 21.5 billion in 2022 to 21.7 billion in 2023. The annual US Parcel Shipping Index reveals that among the four primary carriers (USPS, Amazon Logistics, UPS, and FedEx), only Amazon Logistics registered a significant year-over-year (YoY) volume surge of 15.7%. Moreover, Amazon Logistics has surpassed both FedEx and UPS in parcel volumes and is rapidly approaching the market leader, USPS. Sources indicate that the 'others' category, which includes smaller carriers, saw a substantial uptick in both revenue and volume, enhancing their market share by 28.5% in 2023, bringing it to nearly 3%, or about 0.6 billion parcels. According to the sources, in 2023, USPS led in parcel volume with 6.6 billion parcels (a nearly 1% YoY decline), followed by Amazon Logistics at 5.9 billion parcels (a 15.7% increase), UPS with 4.6 billion parcels (a 10.3% decrease), and FedEx at 3.9 billion parcels (down 6.1%).

- In recent years, North America's postal service industry has faced disruptions from the digital landscape. As communication increasingly migrates online, the traditional mail delivery business is witnessing a decline. Concurrently, the industry is grappling with fierce competition in the expanding e-commerce parcel market. As a result, postal and mailing entities are evolving from state-owned monopolies to commercial firms with diversified portfolios.

North America Postal Services Market Trends

United States exhibits a clear dominance in the market

In the wake of the pandemic, e-commerce in the United States has experienced unprecedented growth, mirroring trends seen in many other countries. With a population of 332 million, the U.S. ranks as the world's third most populous nation, trailing only India and China. Notably, nearly 80% of American internet users engage in online shopping. This surge in e-commerce presents a significant opportunity for postal services. As consumers increasingly turn to both emerging e-commerce platforms and traditional brick-and-mortar stores transitioning online, the demand for efficient delivery and collection channels has intensified. Leveraging their established national networks and expertise in last-mile delivery, postal services are positioning themselves as valuable partners in this evolving landscape. By Q2 2024, e-commerce sales in the U.S. reached USD 291.64 billion, constituting 15.9% of the nation's total retail sales. In the first half of the year, U.S. e-commerce sales soared to USD 579.45 billion, with projections suggesting a climb to USD 1.22 trillion by year's end. The continued growth of e-commerce underscores the critical role of postal services in supporting the digital economy.

Letter Volume is on Decline

The U.S. Postal Service (USPS) stands as the official postal authority in the United States. After peaking at approximately 213 billion units in 2006, USPS has witnessed a consistent annual decline in mail volume. By 2023, deliveries had plummeted to a mere 116.15 billion units. This decline is primarily due to reduced volumes in traditional mail, marketing materials, and periodicals. In contrast, revenue from package shipping has surged. Technology is the primary catalyst for this transformation. An increasing number of Americans are turning to email, leading to a reduced appetite for traditional mail. Additionally, U.S. online retail sales have doubled in the last decade, heightening the demand for package deliveries. Canada Post, Canada's official postal service, mirrors this trend.

North America Postal Services Industry Overview

The industry is currently fragmented. Large companies have advantages in widespread infrastructure and diversity of services. Small companies compete by specializing. Government-owned postal agencies typically have a monopoly on mail delivery but face heavy competition from private package delivery companies. The competing entities form partnerships to capitalize on each other's strengths. For instance, major express delivery companies Federal Express (FedEx) and United Parcel Service (UPS) contract certain residential deliveries to the US Postal Service (USPS), while the USPS contracts air transportation out to FedEx and UPS.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Market Drivers

- 4.2.1 Rise In Ecommerce

- 4.2.2 Expansion of Same Day and Next- Day Delivery

- 4.3 Market Restraints

- 4.3.1 Rising Labor Costs

- 4.3.2 Cybersecurity and Mail Security

- 4.4 Market Opportunities

- 4.4.1 Increased Automation and Technology

- 4.5 Value Chain / Supply Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Express Postal Services

- 5.1.2 Standard Postal Services

- 5.2 By Item

- 5.2.1 Letter

- 5.2.2 Parcel

- 5.3 By Destination

- 5.3.1 Domestic

- 5.3.2 International

- 5.4 By Geography

- 5.4.1 US

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 USPS

- 6.2.2 Canada Post Corporation

- 6.2.3 UPS

- 6.2.4 DHL

- 6.2.5 FedEX

- 6.2.6 Purolator

- 6.2.7 Correos de Mexico

- 6.2.8 Estafeta

- 6.2.9 GLS

- 6.2.10 APC Postal Logistics

- 6.2.11 Santa Lucia Post

- 6.2.12 Grenada Postal Corporation

- 6.2.13 Paquetexpress*

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators

- 8.2 Contribution of Transportation and Storage to GDP

中歐和東歐快遞、快遞和包裹 (CEP):市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

中歐和東歐快遞、快遞和包裹 (CEP):市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 北美快遞包裹 (CEP):市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

北美快遞包裹 (CEP):市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 南美快遞、快遞、包裹 (CEP):市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

南美快遞、快遞、包裹 (CEP):市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 德國快遞包裹 (CEP):市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

德國快遞包裹 (CEP):市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 東協快遞包裹 (CEP):市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

東協快遞包裹 (CEP):市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 歐洲快遞包裹 (CEP):市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

歐洲快遞包裹 (CEP):市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 美國國內宅配:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

美國國內宅配:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 美國宅配、快捷郵件和小包裹(CEP) 市場 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

美國宅配、快捷郵件和小包裹(CEP) 市場 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 2025 年全球當日送達服務市場報告

2025 年全球當日送達服務市場報告 2025 年至 2033 年快遞、快遞和包裹市場報告,按服務類型(B2B、B2C、C2C)、目的地、類型、最終用途行業(服務、批發和零售貿易、製造業、建築和公用事業等)和地區分類

2025 年至 2033 年快遞、快遞和包裹市場報告,按服務類型(B2B、B2C、C2C)、目的地、類型、最終用途行業(服務、批發和零售貿易、製造業、建築和公用事業等)和地區分類