|

市場調查報告書

商品編碼

1683948

汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Automotive LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

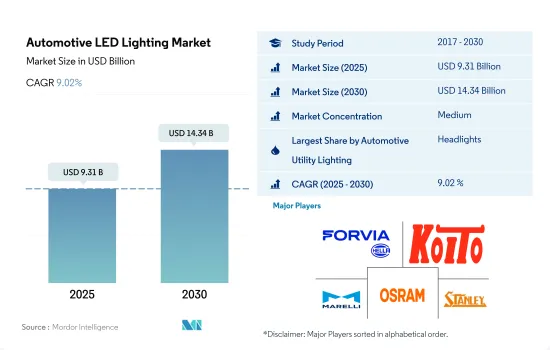

預計2025年汽車LED照明市場規模為93.1億美元,2030年將達到143.4億美元,預測期間(2025-2030年)的複合年成長率為9.02%。

事故率上升、電動車需求成長以及政府支持政策正在推動市場成長

- 就金額佔有率而言,2022 年前照燈將佔據大部分市場佔有率(51.8%),其次是其他 (小型 LED 燈、LED 牌照燈、霧燈、內部 LED 燈)、轉向燈 (DSL)、日間行車燈和煞車燈。預計未來頭燈領域將佔據較高的市場佔有率。隨著事故數量的增加, LED燈和頭燈的採用率預計也將增加。全球每年約有130萬人死於道路交通事故。

- 從出貨量佔有率來看,2023年DSL將佔大部分市場佔有率(27.9%),其次是頭燈(17.7%)、其他(小型LED燈、LED牌照燈、霧燈、車內LED燈)(16.4%)和煞車燈。預測期內,所有細分市場的市場佔有率預計將保持穩定,其他細分市場和煞車燈細分市場的佔有率將略有下降,而 DSL 和頭燈細分市場的佔有率將有所成長。外部燈光(主要是訊號燈)在所有類型的車輛中都可能受到影響,需要更換。

- 電動車是全球汽車LED需求快速成長的主要驅動力之一。中國將引領電動車市場,佔2022年全球電動車銷量的60%,其次是歐洲和美國,分別達到15%和55%的強勁成長。

- 歐盟的「Fit for 55」計畫和美國的「抑制通膨法案」等主要國家的雄心勃勃的政策計畫預計將提升電動車的市場佔有率。市場主要參與者也正致力於在已開發國家擴建電動車工廠。

電動車、自動駕駛汽車的成長以及政府獎勵預計將推動汽車產業對 LED 燈的採用。

- 從金額佔有率來看,2022年亞太地區將佔據汽車LED照明市場的主導地位,其次是北美和歐洲。預計 2029 年亞太地區的市場佔有率將會增加,因為大多數亞洲國家(即中國、日本、泰國、台灣、馬來西亞和印度)都推出了保護國內市場佔有率和為汽車製造商提供優惠待遇等激勵獎勵來促進汽車行業的發展。

- 從銷售佔有率來看,2022年亞太地區將佔據汽車LED照明市場的大部分佔有率,其次是歐洲和北美。在歐洲,電動車的興起和車輛所用燃料類型的技術進步正在改變該地區的汽車工業。目前,歐盟電池式電動車銷量正在快速成長。例如,2022年歐盟市場上銷售的910萬輛汽車中,有12.1%是純電動車。相較之下,2019 年這一比例僅 1.9%,2021 年則為 9.1%。

- 電氣化是全球汽車產業正在經歷的最大轉型。另一個趨勢是自動駕駛汽車。重要的是,該技術有助於汽車公司實現碳中和目標。中東是日產的重要市場。許多現代汽車變得更聰明、更互聯。它將配備與日產 Ariya 類似的智慧移動和自動駕駛功能。該地區的其他地區也正在發生類似的轉變。因此,該地區汽車產業的成長可能會推動LED市場的滲透。

全球汽車LED照明市場趨勢

電動車需求增加預計將推高市場價值

- 預計 2022 年全球汽車產量將達到 1.4396 億輛,2023 年將達到 1.5092 億輛。收集到的資料顯示,2020 年全球汽車產量將下降 16%,而 2019 年全球汽車產量已下降了約 5%。歐洲平均降幅超過21%。所有主要生產國的降幅均約11%至40%。歐洲製造業約佔總產量的22%。 2020年,美洲地區的汽車產量佔全球產量的20%。美洲大陸的製造業已暴跌35%以上。同時,亞洲表現良好,降幅僅 10%。根據提供的數據,COVID-19 疫情對汽車產業產生了重大影響,減少了對 LED 的需求。

- 大眾集團、Stellantis、梅賽德斯-奔馳、寶馬、保時捷、Hurtan、GTA Motors、奧迪、塔塔汽車、馬恆達、上汽汽車、現代汽車、起亞汽車、KG Mobility 和雷諾韓國汽車是世界上一些主要的汽車製造公司。預計2022年全球電動車銷量將突破1,000萬輛,2023年將成長35%,達到1,400萬輛。這種快速擴張使得電動車的市場佔有率從2020年的4%上升到2022年的14%。此外,隨著電動車越來越受歡迎,每輛車將擁有比傳統汽車更多的處理器,這將推動對車載半導體晶片的需求。預計LED照明市場將受益於汽車產業對半導體日益成長的需求。

電池更換站和電池回收服務店的增加以及對電動車的需求不斷成長預計將推動市場成長。

- 電動車市場正在迅速擴張,預計到 2022 年銷量將超過 1,000 萬輛。 2022 年,電動車將佔所有新車銷量的 14%,高於 2021 年的 9% 左右和 2020 年的不到 5%。全球銷售由三個市場推動。中國處於領先地位,佔全球電動車銷量的近60%。中國佔全球電動車保有量的一半以上,政府已超額完成了2025年新能源車銷售目標。

- 至2022年,全國將擁有換電站1973座(其中2022年建成675座),動力電池回收服務門市將超過10,000家。因此,充電設施的快速增加表明該國新能源汽車(NEV)產業的蓬勃發展。 2022年10月,德國政府宣布了加強電動車充電基礎設施的計畫。該計劃包括一項耗資 63 億歐元(61.7 億美元)的提案,旨在到 2030 年將全國充電站的數量增加到 100 萬個。

- 在主要市場中,2022 年的電動車銷量處於典型的低水平,但印度、泰國和印尼卻經歷了成長的一年。這些國家的電動車銷量自2021年以來成長了兩倍多,達到8萬輛。在美國,通貨膨脹削減法案(IRA)加上許多州採用加州的《高級清潔汽車 II》法規,很可能會使電動車的市場佔有率到 2030 年達到 50%,與國家目標一致。考慮到上述案例,預計全球各大廠商將進一步增加對車用LED研發和生產的投資。

汽車 LED 照明產業概況

汽車LED照明市場格局適度整合,前五大廠商佔51.31%。該市場的主要企業有:HELLA GmbH & Co. KGaA (FORVIA)、KOITO MANUFACTURING、Marelli Holdings、OSRAM GmbH。以及史丹利電氣(按字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章執行摘要和主要發現

第2章 報告要約

第 3 章 簡介

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 汽車產量

- 人口

- 人均收入

- 汽車貸款利率

- 充電站數量

- 行駛車輛數

- LED進口總量

- 家庭數量

- 道路網路

- 滲透率

- 法律規範

- 阿根廷

- 巴西

- 中國

- 法國

- 德國

- 波灣合作理事會

- 印度

- 日本

- 南非

- 韓國

- 西班牙

- 英國

- 美國

- 價值鏈與通路分析

第5章 市場區隔

- 汽車實用照明

- 日間行車燈 (DRL)

- 轉向指示燈

- 頭燈

- 倒車燈

- 紅綠燈

- 尾燈

- 其他

- 汽車照明

- 二輪車

- 商用車

- 搭乘用車

- 地區

- 亞太地區

- 歐洲

- 中東和非洲

- 北美洲

- 南美洲

第6章 競爭格局

- 主要策略趨勢

- 市場佔有率分析

- 業務狀況

- 公司簡介(包括全球概況、市場層級概況、主要業務部門、財務狀況、員工人數、關鍵資訊、市場排名、市場佔有率、產品和服務、最新發展分析)

- GRUPO ANTOLIN IRAUSA, SA

- HELLA GmbH & Co. KGaA(FORVIA)

- Hyundai Mobis

- KOITO MANUFACTURING CO., LTD.

- Marelli Holdings Co., Ltd.

- Nichia Corporation

- OSRAM GmbH.

- Signify(Philips)

- Stanley Electric Co., Ltd.

- Valeo

第7章:執行長的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源和進一步閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 50001646

The Automotive LED Lighting Market size is estimated at 9.31 billion USD in 2025, and is expected to reach 14.34 billion USD by 2030, growing at a CAGR of 9.02% during the forecast period (2025-2030).

The rising accident rates, growing demand for EVs, and supportive government policies drive the market's growth

- In terms of value share, in 2022, headlights accounted for most of the market share (51.8%), followed by others (miniature LED lights, LED license plate lights, fog Lights, and interior LED lights), directional signal lights (DSLs), day time running lights, and stop lights. The headlights segment is expected to gain a higher market share in the future. Along with the rising number of accidents, the penetration rate of fog LED lamps and headlamps is anticipated to rise. Approximately 1.3 million people die each year as a result of road traffic crashes globally.

- In terms of volume share, in 2023, DSLs accounted for most of the market share (27.9%), followed by headlights (17.7%), others (miniature LED lights, LED license plate lights, fog Lights, and interior LED lights) (16.4%), and stop lights. The market share is expected to remain the same for all the segments during the forecast period, with a slight reduction in the others and stop lights segment and an increase in the DSLs and headlights segments. External lights (primarily signal lights) are highly likely to be affected in minor to major accidents in all types of vehicles and require replacement.

- EVs are one of the primary drivers for the surging demand for automotive LEDs globally. China led the EV market, accounting for 60% of global electric car sales in 2022, followed by Europe and the United States, which saw strong sales growth of 15% and 55%, respectively.

- The ambitious policy programs in major economies, such as the Fit for 55 package in the European Union and the Inflation Reduction Act in the United States, are expected to boost the market share of EVs. Key players in the market are also focusing on expanding their EV plants in developed nations.

Growth in EVs, autonomous vehicles, and government incentives are expected to boost the adoption of LED lights in the automotive industry

- In terms of value share, the Asia-Pacific automotive LED lighting market accounted for the majority share in 2022, followed by North America and Europe, respectively. The market share is expected to increase for Asia-Pacific in 2029, as most of the six Asian countries, such as China, Japan, Thailand, Taiwan, Malaysia, and India, have introduced incentives such as protecting their domestic markets and giving preferential treatment to automakers in promoting their automobile industries.

- In terms of volume share, the Asia-Pacific automotive LED lighting market accounted for the majority share in 2022, followed by Europe and North America. In Europe, the rise of electric vehicles and technological advances in the types of fuels used in vehicles are transforming the region's automotive industry. Sales of battery electric vehicles in the European Union are still growing rapidly. For example, 12.1% of the 9.1 million cars sold on the EU market in 2022 were pure battery electric vehicles. By contrast, in 2019, this share was just 1.9%, and in 2021 it was 9.1%.

- Electrification is the most significant transformation the industry is undergoing worldwide. Another trend rising is autonomous vehicles. It is important to note that technology contributes to auto companies' carbon-neutral goals. The Middle East is an important market for Nissan. Many modern vehicles are getting smarter and more connected. It will be equipped with intelligent mobility and autonomous driving, similar to the Nissan Ariya. Such transformations are undertaken in other parts of the region. Thus, growth in the regional automotive segment may increase the penetration of LEDs in the market.

Global Automotive LED Lighting Market Trends

The increasing demand for EVs is anticipated to raise the market value

- The total automobile production globally was 143.96 million units in 2022, and it was expected to reach 150.92 million units in 2023. The gathered data indicated a 16% reduction in the manufacturing of automotive cars in 2020, following a dismal 2019, which already showed a noticeable decline of roughly 5% in global auto output. The average decline across all of Europe was more than 21%. Sharp decreases in all major producing nations ranged from 11% to roughly 40%. Manufacturing in Europe accounted for roughly 22% of the total production. Vehicle manufacturing in the Americas accounted for 20% of global production in 2020. The African continent had a severe decrease of more than 35% in manufacturing. Asia, on the other hand, held up very well, with a decline of only 10%. According to the numbers provided, the COVID-19 pandemic had a tremendous impact on the automotive industry, which decreased the demand for LEDs.

- Volkswagen Group, Stellantis, Mercedes-Benz, BMW, Porsche, Hurtan, GTA Motors, Audi, TATA Motors, Mahindra & Mahindra, SAIC Motor, Hyundai Motor Company, Kia Corporation, KG Mobility, and Renault Korea Motors are the major automotive manufacturing companies globally. In 2022, there were more than 10 million electric vehicle sales worldwide, and the sales in 2023 were anticipated to increase by another 35% to a total of 14 million. Due to this rapid expansion, the market share of electric automobiles increased from 4% in 2020 to 14% in 2022. In addition, as more electric vehicles are being used, there is a rising demand for automotive semiconductor chips because they require more processors per vehicle than conventional cars. The market for LED lighting is expected to benefit from the increase in semiconductor demand in the automobile industry.

The increasing number of battery swapping stations and battery recycling service outlets and the rising demand for EVs are expected to drive the growth of the market

- The EV markets are expanding at an exponential rate, with sales exceeding 10 million in 2022. In 2022, electric vehicles accounted for 14% of all new vehicle sales, up from roughly 9% in 2021 and less than 5% in 2020. Global sales were led by three markets. China was the leader, accounting for almost 60% of global electric vehicle sales. China accounts for more than half of all the electric vehicles on the road worldwide, and the government has already exceeded its 2025 target for new energy vehicle sales.

- By 2022, China had 1,973 battery swapping stations, including 675 built in 2022 and over 10,000 power battery recycling service outlets. Thus, the rapid growth of charging facilities indicates the booming new energy vehicle (NEV) sector in the country. In October 2022, the German government unveiled plans to boost charging infrastructure for electric vehicles. The plan consisted of a EUR 6.3 billion (USD 6.17 billion) proposal that would increase the number of charging points across the country to 1 million by 2030.

- In major markets, electric car sales were normally low in 2022, but it was a growth year in India, Thailand, and Indonesia. Sales of electric vehicles in these countries more than tripled since 2021, reaching 80,000 units. In the United States, the Inflation Reduction Act (IRA), combined with a number of states adopting California's Advanced Clean Cars II rule, is likely to produce a 50% market share for electric cars in 2030, in line with the national target. Considering the abovementioned instances, key manufacturers across the world are expected to invest more in developing and producing automotive LEDs.

Automotive LED Lighting Industry Overview

The Automotive LED Lighting Market is moderately consolidated, with the top five companies occupying 51.31%. The major players in this market are HELLA GmbH & Co. KGaA (FORVIA), KOITO MANUFACTURING CO., LTD., Marelli Holdings Co., Ltd., OSRAM GmbH. and Stanley Electric Co., Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Automotive Production

- 4.2 Population

- 4.3 Per Capita Income

- 4.4 Interest Rate For Auto Loans

- 4.5 Number Of Charging Stations

- 4.6 Number Of Automobile On-road

- 4.7 Total Import Of Leds

- 4.8 # Of Households

- 4.9 Road Networks

- 4.10 Led Penetration

- 4.11 Regulatory Framework

- 4.11.1 Argentina

- 4.11.2 Brazil

- 4.11.3 China

- 4.11.4 France

- 4.11.5 Germany

- 4.11.6 Gulf Cooperation Council

- 4.11.7 India

- 4.11.8 Japan

- 4.11.9 South Africa

- 4.11.10 South Korea

- 4.11.11 Spain

- 4.11.12 United Kingdom

- 4.11.13 United States

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Automotive Utility Lighting

- 5.1.1 Daytime Running Lights (DRL)

- 5.1.2 Directional Signal Lights

- 5.1.3 Headlights

- 5.1.4 Reverse Light

- 5.1.5 Stop Light

- 5.1.6 Tail Light

- 5.1.7 Others

- 5.2 Automotive Vehicle Lighting

- 5.2.1 2 Wheelers

- 5.2.2 Commercial Vehicles

- 5.2.3 Passenger Cars

- 5.3 Region

- 5.3.1 Asia-Pacific

- 5.3.2 Europe

- 5.3.3 Middle East and Africa

- 5.3.4 North America

- 5.3.5 South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 GRUPO ANTOLIN IRAUSA, S.A.

- 6.4.2 HELLA GmbH & Co. KGaA (FORVIA)

- 6.4.3 Hyundai Mobis

- 6.4.4 KOITO MANUFACTURING CO., LTD.

- 6.4.5 Marelli Holdings Co., Ltd.

- 6.4.6 Nichia Corporation

- 6.4.7 OSRAM GmbH.

- 6.4.8 Signify (Philips)

- 6.4.9 Stanley Electric Co., Ltd.

- 6.4.10 Valeo

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

中國汽車 LED 照明:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)中東和非洲汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)亞太地區汽車 LED 照明:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)南美汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)印度汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)德國汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)日本汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)歐洲汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)法國汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

中國汽車 LED 照明:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)中東和非洲汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)亞太地區汽車 LED 照明:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)南美汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)印度汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)德國汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)日本汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)歐洲汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)法國汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

▼