|

市場調查報告書

商品編碼

1683961

北美汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)North America Automotive LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

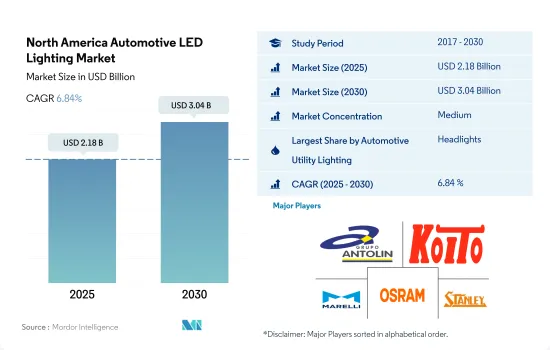

北美汽車 LED 照明市場規模預計在 2025 年為 21.8 億美元,預計到 2030 年將達到 30.4 億美元,預測期內(2025-2030 年)的複合年成長率為 6.84%。

事故率上升、 LED燈普及率上升、電動車銷售成長,推動市場成長

- 就以金額為準,2022 年前照燈將佔據最大佔有率,其次是其他(小型 LED 燈、LED 牌照燈、霧燈、內部 LED 燈)、方向燈(DSL)、日間行車燈和煞車燈。預計 All Lite 的市場佔有率將保持平穩,其他和 DSL 的市場佔有率將略有下降,而 Headlight 的市場佔有率將成長。隨著事故趨勢的上升, LED燈的普及率也預計將增加。在美國,2022 年機動車死亡人數預計將達到 46,000 人,與大流行前相比增加近 22%。

- 從出貨量來看,2022年方向燈將佔最大佔有率,其次是頭燈、其他(小型LED燈、LED牌照燈、霧燈、車內LED燈)和煞車燈。戶外燈是任何類型車輛的主要部件,在輕微至重大事故中都可能受到影響並需要更換。

- 2022年新型輕型汽車銷量達1370萬輛。預計 2022 年新車銷售量將與前一年同期比較減 8.2%,主要原因是微晶片短缺持續以及供應鏈進一步中斷。混合動力汽車、插電混合動力汽車混合動力車和電池電動車(BEV)將佔2022年所有新車銷量的12.3%,比2021年成長2.7%。因此,汽車銷售的增加導致對LED照明的需求增加。

新興國家電動車的發展以及有利於發展當地汽車產業的立法將推動 LED 照明的需求

- 以以金額為準,美國LED照明市場將在2022年佔據大部分市場佔有率,其次是北美地區(RONA)。預計未來幾年市場佔有率將保持相對穩定,美國佔有率將下降,而北美其他地區的市場佔有率將上升。美國國內汽車產量將從2021年的910萬輛增加至2022年的1,006萬輛。汽車產量包括乘用車和商用車。在加拿大,預計 2022 年汽車產量將比 2021 年增加 10.2%,達到 120 萬輛。國內汽車產量的增加,將帶動市場對車用LED的需求增加。

- 許多北美國家對電動車的需求不斷成長。 2022 年墨西哥新車銷量將達到 108 萬輛,比 2021 年成長 7%,而 2022 年美國電動車銷量將成長 65%。

- 在汽車行業子部門中,美國和墨西哥的商業服務在原始設備零件、售後市場和電動車(EV)零件方面經歷了強勁機會。墨西哥為OEM和售後市場生產的汽車零件預計將從 2020 年的 784 億美元增加到 2021 年的 947 億美元,2022 年將達到 1,010 億美元以上。

- 《美國-墨西哥-加拿大協定》(USMCA)於2020年7月1日生效。 USMCA要求汽車75%的零件必須在北美生產,核心汽車零件原產於美國、加拿大或墨西哥。考慮到上述因素,例如電動車的採用和發展當地汽車產業的有利立法,預計未來幾年 LED 將在北美地區蓬勃發展。

北美汽車 LED 照明市場趨勢

電動車和電池製造商的投資推動了 LED 市場的發展,以提高汽車產量

- 預計2022年北美汽車總產量將達1,454萬輛,2023年將達1,506萬輛。汽車業是北美最大的製造業部門之一。然而,新冠疫情為該地區的汽車產業帶來了兩次重大衝擊,對2020年和2021年的生產、銷售和對外貿易產生了顯著的負面影響。因此,汽車供應鏈和生產的中斷對該地區的LED照明業務產生了負面影響。

- 3月美國輕型汽車產量與去年同期相比下降了近31%。由於 4 月底只有一家工廠運作一周,因此需要更高水準的輕型汽車生產。汽車業也對供應鍊錶示擔憂。德國供應商ZF在美國設有工廠,並宣布計畫在2020年5月底前在全球裁員10%。全球供應鏈中斷影響了美國製造業:梅賽德斯-奔馳於4月27日重新開放其位於阿拉巴馬州萬斯的工廠,但由於零件短缺,於5月15日被迫停產。此次動盪導致汽車業使用的半導體價格下跌。

- 此外,在政府的主導,北美對電動車的需求正在激增。 《通膨削減法案》將於2022年8月簽署成為法律,從法案簽署到2023年3月,主要電動車和電池製造商已宣布向北美電動車供應鏈投資至少520億美元。這些有利於消費者和製造商的舉措預計將促進該地區的 LED 照明業務發展。

政府投資推動電動車銷售和LED照明成長

- 北美地區電動車銷量大部分來自美國、加拿大和墨西哥。 2022 年,美國純電動車銷量預計將比 2021 年成長 65%,特斯拉將繼續主導電動車市場。 2022年,墨西哥109萬輛汽車的總銷量中僅有0.5%是純電動車,這一比例明顯低於中國、歐洲和美國等其他市場。在加拿大,2022 年第四季新註冊的電池電動車 (BEV) 數量為 27,754 輛,新註冊的插電式混合動力車 (PHEV) 數量為 5,645 輛。

- 為了進一步擴大規模,美國政府於 2021 年宣布了一項 1 兆美元的基礎設施法案,其中撥款 75 億美元用於在 2030 年前額外建造 50 萬個公共電動車充電樁,同時透過為購買在美國組裝的電動車提供 7,500 美元的稅收優惠來投資電動汽車製造業。此外,主要企業之一特斯拉承諾到年終為美國所有品牌的電動車提供約 3,500 個超級充電站和 4,000 個二級充電座。

- 通用汽車加拿大公司正在加拿大投資超過 20 億美元,將位於英格索爾和奧沙瓦的製造工廠改造為 2022 年底年終生產電動車。到 2030 年,喬治亞、肯塔基州和密西根州預計將佔據美國電動車電池製造的大部分佔有率。這種電動車電池製造能力將促進每年生產 1,000 萬至 1,300 萬個全電動汽車電池,使美國成為全球電動車競爭對手。因此,上述案例將由於電動車需求的增加而引發新發電廠的開發和生產,從而推動該地區對汽車 LED 的需求。

北美汽車 LED 照明產業概況

北美汽車LED照明市場呈現中度整合態勢,前五大廠商合計佔52.69%的市佔率。該市場的主要企業有:GRUPO ANTOLIN IRAUSA,SA、KOITO MANUFACTURING、Marelli Holdings、OSRAM GmbH。以及史丹利電氣(按字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章執行摘要和主要發現

第2章 報告要約

第 3 章 簡介

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 汽車產量

- 人口

- 人均收入

- 汽車貸款利率

- 充電站數量

- 汽車持有量

- LED進口總量

- 家庭數量

- 道路網路

- 滲透率

- 法律規範

- 美國

- 價值鏈與通路分析

第5章 市場區隔

- 汽車實用照明

- 日間行車燈 (DRL)

- 轉向指示燈

- 頭燈

- 倒車燈

- 紅綠燈

- 尾燈

- 其他

- 汽車照明

- 二輪車

- 商用車

- 搭乘用車

- 國家名稱

- 美國

- 北美其他地區

第6章 競爭格局

- 主要策略趨勢

- 市場佔有率分析

- 業務狀況

- 公司簡介(包括全球概況、市場層級概況、主要業務部門、財務狀況、員工人數、關鍵資訊、市場排名、市場佔有率、產品和服務、最新發展分析)

- GRUPO ANTOLIN IRAUSA, SA

- HELLA GmbH & Co. KGaA(FORVIA)

- Hyundai Mobis

- KOITO MANUFACTURING CO., LTD.

- Marelli Holdings Co., Ltd.

- Nichia Corporation

- OSRAM GmbH.

- Stanley Electric Co., Ltd.

- Valeo

- ZKW Group

第7章:執行長的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源和進一步閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

The North America Automotive LED Lighting Market size is estimated at 2.18 billion USD in 2025, and is expected to reach 3.04 billion USD by 2030, growing at a CAGR of 6.84% during the forecast period (2025-2030).

Rising accident trend, penetration rate of fog LED lamps, and increasing sales of electric vehicles drive market growth

- In terms of value, in 2022, headlights accounted for a major share, followed by others (miniature LED lights, LED license plate lights, fog lights, and interior LED lights), directional signal lights (DSLs), daytime running lights, and stop lights. The market share is expected to remain the same for all lights, with a small reduction in others and DSLs, and grow for headlights. With the rising accident trend, the penetration rate of fog LED lamps is anticipated to rise. In the US, the number of motor vehicle deaths reached an estimated 46,000 in 2022 compared to the pre-pandemic death rate, an increase of nearly 22%.

- In terms of volume, in 2022, directional signal lights accounted for a major share, followed by headlights, others (miniature LED lights, LED license plate lights, fog lights, and interior LED lights), and stop lights. External lights are the prime parts that have a high probability of getting affected in minor to major accidents in all types of vehicles and require replacement.

- The year 2022 ended with new light-vehicle sales reaching 13.7 million units. The Y-o-Y 2022 sales decreased by 8.2% compared to 2021, with the decrease primarily attributed to the ongoing microchip shortage and additional supply chain disruptions. With sales of hybrid, plug-in hybrid, and battery electric vehicles (BEVs) accounting for 12.3% of all new vehicle sales in 2022, an increase of 2.7% from 2021, alternative fuel vehicles gained market share. Thus, the increase in vehicle sales resulted in an increase in the requirement for LED lights.

Adoption of EVs across countries and favorable laws to develop local automotive industry drive the demand for LED lighting

- In terms of value, in 2022, the US LED light market accounted for the majority of the share, followed by the Rest of North America (RONA). The market share is expected to decline for the US and increase for the Rest of North America, with less fluctuation in the coming years. The domestic vehicle production in the US increased from 9.1 million units in 2021 to 10.06 million units in 2022. The vehicle production includes cars and commercial vehicles. In Canada, in 2022, vehicle production increased by 10.2% compared to 2021, accounting for 1.2 million units. The increase in domestic vehicle production creates more demand for automotive LEDs in the market.

- The demand for EVs grew across many countries in North America. Mexico saw 1.08 million new car sales in 2022, a 7% improvement from 2021, and US EV sales increased by 65% in 2022.

- In sub-sectors of the automotive industry, the US and Mexican commercial services experienced strong opportunities in OE parts, aftermarket, and electric vehicle (EV) parts. The value of Mexican automotive parts for OEMs and aftermarket production increased from USD 78.4 billion in 2020 to USD 94.7 billion in 2021, and it is expected to reach more than USD 101 billion by 2022.

- The United States, Mexico, Canada Agreement (USMCA) went into effect on July 1, 2020. The USMCA requirement stated that 75% of a vehicle's content must be produced in North America and that core auto parts originate from the United States, Canada, or Mexico. Considering the above-mentioned factors, such as the adoption of EVs and favorable laws to develop the local automotive industry, the growth of LEDs is expected across North America in the coming years.

North America Automotive LED Lighting Market Trends

The LED market is driven by investments by EVs and battery producers to increase automotive production

- The total automobile vehicle production in North America was 14.54 million units in 2022, and it is expected to reach 15.06 million units in 2023. One of the biggest manufacturing sectors in North America is the automotive sector. However, the COVID-19 pandemic caused two significant shocks to the region's automobile industry, which had a significant negative impact on production, sales, and foreign trade in 2020 and 2021. Thus, the disruption in the supply chain and production of automotive vehicles negatively affected the LED lighting business in the region.

- March saw an almost 31% year-over-year fall in the US light car production. Only one plant was operating for one week at the end of April, so there needed to be a higher level of light vehicle production. The auto industry also voiced concerns regarding its supply networks. ZF, a German supplier, has facilities in the United States and revealed plans to reduce its global employment by 10% by the end of May 2020. Several worldwide supply chain disruptions impacted manufacturing in the United States: Mercedes-Benz resumed its Vance, Alabama, facility on April 27; however, due to a scarcity of parts, production had to be briefly halted on May 15. This disruption created a downfall in semiconductors used in the automotive industry.

- Further, the demand for EVs is rapidly increasing in North America due to government initiatives. The Inflation Reduction Act was passed in August 2022, and between that time and March 2023, major EV and battery producers announced investments in North American EV supply chains worth at least USD 52 billion. Such initiatives in the interest of consumers and manufacturers will boost the LED lighting business in the region.

Government investments to drive the sales of electric vehicle and propel the growth of LED lighting

- Most of the EV sales in the North American region come from the US, Canada, and Mexico. In 2022, US BEV sales increased by 65% compared to 2021, and Tesla continues to dominate the EV market. In 2022, Mexico sales were only 0.5% of 1,090,000 total vehicle sales were fully electric, a percentage that falls well below other markets, such as China, Europe, and the United States. In Canada, during Q4 2022, battery electric vehicles (BEVs) alone had 27,754 new registrations, and plug-in hybrid electric vehicles (PHEVs) had 5,645 new registrations.

- To expand further, the US government issued a trillion-dollar infrastructure bill in 2021 that allocates USD 7.5 billion toward building 500,000 more public EV chargers by 2030 and also made investments in EV manufacturing by providing tax benefits of USD 7,500 for purchasing an EV assembled in the US. Also, Tesla, one of the significant players in EVs, committed to delivering around 3,500 of its US Supercharger stations and 4,000 Level 2 charging docks available to all brands of electric vehicles by the end of 2024.

- GM Canada invested more than USD 2 billion in Canada to transform manufacturing facilities in Ingersoll and Oshawa and expects electric vehicle production by the end of 2022. By 2030, Georgia, Kentucky, and Michigan are expected to dominate electric vehicle battery manufacturing in the United States. This EV battery manufacturing capacity will facilitate the production of 10 to 13 million batteries for all-electric vehicles per year, positioning the United States as a global EV competitor. Thus, the above instances lead to the development and production of new power stations because of the growing demand for EVs, which boosts the demand for automotive LEDs in the region.

North America Automotive LED Lighting Industry Overview

The North America Automotive LED Lighting Market is moderately consolidated, with the top five companies occupying 52.69%. The major players in this market are GRUPO ANTOLIN IRAUSA, S.A., KOITO MANUFACTURING CO., LTD., Marelli Holdings Co., Ltd., OSRAM GmbH. and Stanley Electric Co., Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Automotive Production

- 4.2 Population

- 4.3 Per Capita Income

- 4.4 Interest Rate For Auto Loans

- 4.5 Number Of Charging Stations

- 4.6 Number Of Automobile On-road

- 4.7 Total Import Of Leds

- 4.8 # Of Households

- 4.9 Road Networks

- 4.10 Led Penetration

- 4.11 Regulatory Framework

- 4.11.1 United States

- 4.12 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Automotive Utility Lighting

- 5.1.1 Daytime Running Lights (DRL)

- 5.1.2 Directional Signal Lights

- 5.1.3 Headlights

- 5.1.4 Reverse Light

- 5.1.5 Stop Light

- 5.1.6 Tail Light

- 5.1.7 Others

- 5.2 Automotive Vehicle Lighting

- 5.2.1 2 Wheelers

- 5.2.2 Commercial Vehicles

- 5.2.3 Passenger Cars

- 5.3 Country

- 5.3.1 United States

- 5.3.2 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 GRUPO ANTOLIN IRAUSA, S.A.

- 6.4.2 HELLA GmbH & Co. KGaA (FORVIA)

- 6.4.3 Hyundai Mobis

- 6.4.4 KOITO MANUFACTURING CO., LTD.

- 6.4.5 Marelli Holdings Co., Ltd.

- 6.4.6 Nichia Corporation

- 6.4.7 OSRAM GmbH.

- 6.4.8 Stanley Electric Co., Ltd.

- 6.4.9 Valeo

- 6.4.10 ZKW Group

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

中國汽車 LED 照明:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)中東和非洲汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)亞太地區汽車 LED 照明:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)南美汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)印度汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)德國汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)日本汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)歐洲汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)法國汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

中國汽車 LED 照明:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)中東和非洲汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)亞太地區汽車 LED 照明:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)南美汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)印度汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)德國汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)日本汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)歐洲汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)法國汽車 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)