|

市場調查報告書

商品編碼

1685790

作物保護化學品-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Crop Protection Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

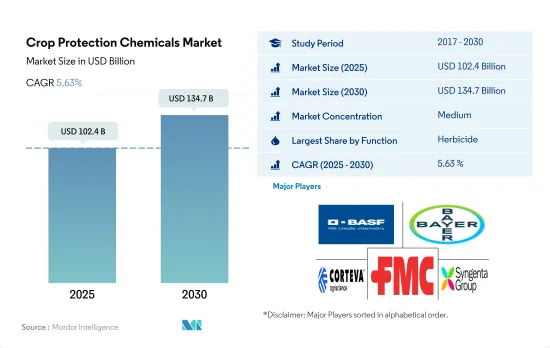

作物保護化學品市場規模預計在 2025 年為 1,024 億美元,預計到 2030 年將達到 1,347 億美元,預測期內(2025-2030 年)的複合年成長率為 5.63%。

病蟲害侵襲推動作物保護化學品市場

- 全球作物保護化學品市場經歷了顯著成長,預計未來將繼續擴大。預計 2022 年市場規模將達到 905.4 億美元,2029 年將達到 1,227.1 億美元,2023 年至 2029 年的複合年成長率為 4.5%。這一成長可歸因於病蟲害日益猖獗、氣候變遷以及對提高作物產量的日益重視。

- 除草劑在全球作物保護化學品市場中佔有很大的佔有率,2022 年以金額為準41.7%。預計它將成為成長最快的行業,2023 年至 2029 年的複合年成長率為 5.1%。作物損失的增加、確保最佳產量的需求以及種植面積的擴大預計將推動除草劑領域的成長。

- 就以金額為準,殺蟲劑領域預計在 2023 年至 2029 年期間的複合年成長率為 4.2%。由於氣候變化,農業中引入害蟲的風險正在增加。粘蟲、沙漠蝗蟲等植物害蟲以及其他幾種侵害重要農業作物的害蟲構成了重大威脅,這可能會在未來幾年推動對殺蟲劑的需求。

- 預計殺菌劑領域在 2023 年至 2029 年間將成長 42.3 億美元。小麥、大豆和馬鈴薯是全球主要種植作物,目前正受到各種真菌疾病的威脅。例如,小麥葉枯病(STB)是歐洲的一種主要病害。這些疾病的爆發每年給英國種植者造成約 2.63 億美元的產量損失。

- 由於保護農作物作物病蟲害侵襲的需求日益成長,預計作物以金額為準領域從 2023 年到 2029 年的複合年成長率將達到 4.5%。

主要國家因病蟲害造成的產量損失不斷增加,促使人們使用作物保護化學物質。

- 害蟲對農業構成重大挑戰。害蟲會損害農作物,降低產量並降低農產品的品質。昆蟲、雜草、真菌和其他生物等害蟲威脅農業生產力。有效的病蟲害管理對於確保糧食安全和維持穩定的糧食供應至關重要。 2017年至2022年,全球作物保護化學品市場成長了30.9%。

- 2022 年,南美洲佔全球農藥市場的大部分佔有率,為 30.4%。該地區包括阿根廷、巴西和智利等國家,其農業化學品市場正在成長。這些國家作為擁有大片農地的重要農業生產國,依靠農藥來有效控制害蟲,以最大限度地提高作物產量。預計 2023 年至 2029 年期間南美作物保護化學品產業的複合年成長率為 4.7%。

- 北美農業多種多樣,不同國家種植多種不同的作物。該地區氣候多樣,土壤肥沃,適合種植小麥、玉米、大豆、菜籽等作物以及各種水果和蔬菜。以價值計算,該地區在 2022 年佔整個作物保護化學品市場的第二大佔有率,為 25.2%。以 2022 年以金額為準,美國的佔有率最高,為 82.4%。然而,雜草和害蟲造成的產量損失對該國的生產和農民的經濟福祉構成了重大威脅。在該國,除草劑在 2022 年的以金額為準佔有率最高,為 52.5%。

- 預計 2023 年至 2029 年期間市場複合年成長率將達到 4.5%。農業部門的快速擴張以及氣候變遷和蟲害的侵擾正在推動市場成長。

全球作物保護化學品市場趨勢

氣候變遷導致農藥使用量增加

- 2022年全球作物保護化學品平均消費量為每公頃117.9公斤。由於農業擴張、集約化和單一耕作方式等因素,全球每公頃平均農藥消費量正在增加。氣溫升高、降水模式改變和極端天氣事件為害蟲繁殖和擴散到新地區創造了有利條件,導致化學農藥的使用增加。

- 2022年殺菌劑消費量將達到最高,達到每公頃48.4公斤,反映出對抗對作物生產構成重大威脅的真菌病害的迫切需求。這些疾病影響穀物、水果、蔬菜和觀賞植物,根據糧食及農業組織的報告,儘管廣泛使用殺菌劑,但仍造成約 2,200 億美元的重大經濟損失。

- 2022年,每公頃施用除草劑44.8公斤。由於雜草適應性強、繁殖迅速、抗藥性不斷增強,化學除草劑的使用量逐年增加,導致雜草侵占作物,造成嚴重的產量損失。例子包括抗Glyphosate的帕爾默莧菜和普通水麻,以及抗乙醯乳酸合成酶抑制除草劑的藜蘆。

- 全球暖化導致的氣候條件變化為某些害蟲的發生創造了有利條件,對農業生產構成了嚴重威脅。 2020年,蝗蟲對23個國家造成不利影響,其中包括東非大片地區的9個國家、東北非洲的11個國家和南亞的3個國家,造成的損失估計達85億美元。

2022 年,Cypermethrin是最昂貴的農藥,每噸售價 21,080 美元。

- Cypermethrin屬於擬除蟲菊酯類殺蟲劑,該類殺蟲劑是一種合成化學品,旨在模仿從菊花中提取的除蟲菊酯的天然殺蟲劑特性。Cypermethrin可有效控制多種害蟲,包括蚜蟲、介殼蟲、毛蟲、葉蟬和粉蝨。其作用機制是麻痺昆蟲的神經系統,最終導致死亡。 2022年Cypermethrin的價格為每噸21,080美元。

- Atrazine是一種廣泛用於控制玉米和水稻作物中的闊葉雜草和禾本科雜草(如稗草、莧菜屬和莧菜)的除草劑。 2022年該除草劑的價格評估為13,800美元。印度是世界上最大的莠Atrazine技術進口國,而中國是最大的出口國。

- Malathion是有機磷酸鹽殺蟲劑,這意味著它屬於有機磷酸鹽化學類別。Malathion的作用機制是抑制乙醯膽鹼酯酶,這種酶對於昆蟲的正常神經功能至關重要。 2022 年的價格為每噸 12,500 美元,是三種化學品中最便宜的。

- Mancozeb是一種屬於Dithiocarbamate的殺菌劑。它常用於防治馬鈴薯、番茄、葡萄、香蕉等作物的晚疫病、霜霉病、早疫病、炭疽病等真菌病害。代森錳鋅比其他殺菌劑具有更廣泛的活性頻譜,可作用於真菌細胞內的多個部位,因此更有效。代森錳鋅2022年的價格為7800美元。

- 丙森鋅和Glyphosate是主要的殺菌劑和除草劑,2022 年的價格分別為每噸 3,500 美元和 1,100 美元。

農化業概況

作物保護化學品市場適度整合,前五大公司佔57.17%的市場。市場的主要企業有:BASF公司、拜耳公司、科迪華農業科技公司、富美實公司和先正達集團。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 每公頃農藥消費量

- 活性成分價格分析

- 法律規範

- 阿根廷

- 澳洲

- 巴西

- 加拿大

- 智利

- 中國

- 法國

- 德國

- 印度

- 印尼

- 義大利

- 日本

- 墨西哥

- 緬甸

- 荷蘭

- 巴基斯坦

- 菲律賓

- 俄羅斯

- 南非

- 西班牙

- 泰國

- 烏克蘭

- 英國

- 美國

- 越南

- 價值鍊和通路分析

第5章市場區隔

- 功能

- 殺菌劑

- 除草劑

- 殺蟲劑

- 殺軟體動物劑

- 殺線蟲劑

- 執行模式

- 化學噴塗

- 葉面噴布

- 燻蒸

- 種子處理

- 土壤處理

- 作物類型

- 經濟作物

- 水果和蔬菜

- 糧食

- 豆類和油籽

- 草坪和觀賞植物

- 地區

- 非洲

- 按國家

- 南非

- 其他非洲國家

- 亞太地區

- 按國家

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 緬甸

- 巴基斯坦

- 菲律賓

- 泰國

- 越南

- 其他亞太地區

- 歐洲

- 按國家

- 法國

- 德國

- 義大利

- 荷蘭

- 俄羅斯

- 西班牙

- 烏克蘭

- 英國

- 其他歐洲國家

- 北美洲

- 按國家

- 加拿大

- 墨西哥

- 美國

- 北美其他地區

- 南美洲

- 按國家

- 阿根廷

- 巴西

- 智利

- 其他南美國家

- 非洲

第6章 競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Jiangsu Yangnong Chemical Co. Ltd

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 47583

The Crop Protection Chemicals Market size is estimated at 102.4 billion USD in 2025, and is expected to reach 134.7 billion USD by 2030, growing at a CAGR of 5.63% during the forecast period (2025-2030).

Rising pest and disease infestations are driving the market for crop protection chemicals

- The global crop protection chemicals market is experiencing significant growth and is expected to continue expanding in the coming years. In 2022, the size of the market reached USD 90.54 billion, and it is expected to register a CAGR of 4.5% between 2023 and 2029, reaching USD 122.71 billion by 2029. This growth can be due to the rising pest and disease infestations, climate changes, and increasing focus on improving crop yield.

- In the global crop protection chemicals market, herbicides hold the major share, accounting for 41.7% in 2022 by value. They are expected to be the fastest-growing segment, with a CAGR of 5.1% by value during 2023-2029. The rising crop losses and the need to ensure optimum yield, coupled with the expansion of cropland, are expected to fuel the growth of the herbicide segment.

- The insecticide segment is projected to register a 4.2% CAGR between 2023 and 2029 by value. The risk of pest infestation in agriculture is increasing due to climate change. Plant pests such as armyworms, desert locusts, and several other pests attacking agriculturally important crops are posing a significant threat, which may drive the demand for insecticides in the coming years.

- The fungicide segment is expected to grow by USD 4.23 billion between 2023 and 2029. Wheat, soybeans, and potatoes are some of the major crops grown globally, which are currently under threat due to various fungal diseases. For instance, Septoria tritici blotch (STB) is a major disease in Europe. Rising infestations of such diseases cost UK growers approximately USD 263 million of yield losses each year.

- The pesticide segment is expected to register a CAGR of 4.5% by value during 2023-2029 due to the rising need to protect crops from pest infestations.

The rise in yield losses by pests in major countries is driving the crop protection chemicals usage

- Pests pose significant challenges to agriculture. They can damage crops, reduce yields, and compromise the quality of harvested produce. Pests like insects, weeds, fungi, and other organisms threaten agricultural productivity. Managing pests effectively is essential for ensuring food security and maintaining a stable food supply. During 2017-2022, the global crop protection chemicals market grew by 30.9%.

- In 2022, South America held a substantial 30.4% share of the global pesticide market's value. This region, encompassing countries like Argentina, Brazil, and Chile, is witnessing growth in its pesticide market. Given their status as significant agricultural producers with extensive farmland, these nations rely on pesticides to effectively control pests and maximize crop yields. The South American crop protection chemicals sector is anticipated to experience a 4.7% CAGR between 2023 and 2029.

- Agriculture in North America is highly diverse, with a wide range of crops cultivated across different countries. The region's diverse climate and fertile land enable the cultivation of crops such as wheat, corn, soybean, canola, and various fruits and vegetables. The region occupied the second-highest share of 25.2% by the value of the overall crop protection chemicals market value in 2022. The United States occupied the highest share of 82.4% by value in 2022. However, yield losses due to weeds and pests are a major threat to the production and the economic well-being of farmers in the country. Herbicides occupied the highest share of 52.5% by value in 2022 in the country.

- The market is projected to register a CAGR of 4.5% during the period 2023-2029. The rapidly expanding agriculture sector, with changing climate and pest infestations, is driving the growth of the market.

Global Crop Protection Chemicals Market Trends

Unusual outbreaks of pests and diseases due to climate change are leading to higher application of pesticides

- The global average consumption of crop protection chemicals was recorded at 117.9 kg per hectare in 2022. The average per hectare consumption of pesticides in the world is increasing due to factors like expanding agriculture and intensive and monoculture farming practices. Rising temperatures, altered precipitation patterns, and extreme weather events create more favorable conditions for pest proliferation and expansion into new areas, leading to increased usage of chemical pesticides.

- In 2022, fungicides saw the highest per-hectare consumption at 48.4 kg, reflecting the critical need to combat fungal diseases that pose a significant threat to crop production. These diseases impact cereals, fruits, vegetables, and ornamentals, leading to substantial economic losses of approximately USD 220.0 billion despite the extensive use of fungicides, as reported by the Food and Agriculture Organization.

- Herbicides were applied at the rate of 44.8 kg per hectare in 2022. Chemical herbicide usage has been escalating every year due to the growing adaptability, rapid reproduction, and herbicide resistance of weeds, causing them to outcompete crops and resulting in significant yield losses. Examples include glyphosate-resistant Palmer amaranth and common water hemp, as well as acetolactate synthase-inhibiting herbicide-resistant Kochia.

- Changing climatic conditions caused by global warming create favorable conditions for certain pests, posing a severe threat to crop production. In 2020, a locust outbreak adversely impacted 23 countries, with nine in wider East Africa, 11 in North Africa & the Middle East, and three in South Asia, resulting in an estimated USD 8.5 billion loss.

Cypermethrin was the highest-priced pesticide, at USD 21.08 thousand per metric ton, in 2022

- Cypermethrin belongs to the class of pyrethroid insecticides, which are synthetic chemicals designed to mimic the natural insecticidal properties of pyrethrins derived from chrysanthemum flowers. Cypermethrin is used to effectively manage a wide range of pests, including aphids, beetles, caterpillars, leafhoppers, and whiteflies. Its mode of action involves disrupting the nervous systems of insects, leading to paralysis and, ultimately, their death. In 2022, cypermethrin was priced at USD 21.08 thousand per metric ton.

- Atrazine is an herbicide widely used for the control of broadleaf and grassy weeds like Echinocloa, Elusine spp., and Amaranthus viridis in maize and rice crops. The herbicide was valued at a price of USD 13.8 thousand in 2022. India is the world's largest importer of atrazine technical, with China being the largest exporter.

- Malathion is an organophosphate insecticide belonging to the chemical class of organophosphates. Malathion's mode of action involves inhibiting acetylcholinesterase, an enzyme essential for proper nerve function in insects. It is the most affordable chemical among the three, priced at USD 12.5 thousand per metric ton in 2022.

- Mancozeb is a fungicide belonging to the chemical class of dithiocarbamates. It is commonly used to control fungal diseases like late blight, downy mildew, early blight, and anthracnose in crops like potatoes, tomatoes, grapes, and bananas. Mancozeb has a broad spectrum of activity compared to other fungicides and acts on multiple sites within the fungal cell, making it more effective. Mancozeb was priced at USD 7.8 thousand in 2022.

- Propineb and glyphosate are important fungicides and herbicides, priced at USD 3.5 thousand and USD 1.1 thousand per metric ton in 2022, respectively.

Crop Protection Chemicals Industry Overview

The Crop Protection Chemicals Market is moderately consolidated, with the top five companies occupying 57.17%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, FMC Corporation and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Australia

- 4.3.3 Brazil

- 4.3.4 Canada

- 4.3.5 Chile

- 4.3.6 China

- 4.3.7 France

- 4.3.8 Germany

- 4.3.9 India

- 4.3.10 Indonesia

- 4.3.11 Italy

- 4.3.12 Japan

- 4.3.13 Mexico

- 4.3.14 Myanmar

- 4.3.15 Netherlands

- 4.3.16 Pakistan

- 4.3.17 Philippines

- 4.3.18 Russia

- 4.3.19 South Africa

- 4.3.20 Spain

- 4.3.21 Thailand

- 4.3.22 Ukraine

- 4.3.23 United Kingdom

- 4.3.24 United States

- 4.3.25 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Herbicide

- 5.1.3 Insecticide

- 5.1.4 Molluscicide

- 5.1.5 Nematicide

- 5.2 Application Mode

- 5.2.1 Chemigation

- 5.2.2 Foliar

- 5.2.3 Fumigation

- 5.2.4 Seed Treatment

- 5.2.5 Soil Treatment

- 5.3 Crop Type

- 5.3.1 Commercial Crops

- 5.3.2 Fruits & Vegetables

- 5.3.3 Grains & Cereals

- 5.3.4 Pulses & Oilseeds

- 5.3.5 Turf & Ornamental

- 5.4 Region

- 5.4.1 Africa

- 5.4.1.1 By Country

- 5.4.1.1.1 South Africa

- 5.4.1.1.2 Rest of Africa

- 5.4.2 Asia-Pacific

- 5.4.2.1 By Country

- 5.4.2.1.1 Australia

- 5.4.2.1.2 China

- 5.4.2.1.3 India

- 5.4.2.1.4 Indonesia

- 5.4.2.1.5 Japan

- 5.4.2.1.6 Myanmar

- 5.4.2.1.7 Pakistan

- 5.4.2.1.8 Philippines

- 5.4.2.1.9 Thailand

- 5.4.2.1.10 Vietnam

- 5.4.2.1.11 Rest of Asia-Pacific

- 5.4.3 Europe

- 5.4.3.1 By Country

- 5.4.3.1.1 France

- 5.4.3.1.2 Germany

- 5.4.3.1.3 Italy

- 5.4.3.1.4 Netherlands

- 5.4.3.1.5 Russia

- 5.4.3.1.6 Spain

- 5.4.3.1.7 Ukraine

- 5.4.3.1.8 United Kingdom

- 5.4.3.1.9 Rest of Europe

- 5.4.4 North America

- 5.4.4.1 By Country

- 5.4.4.1.1 Canada

- 5.4.4.1.2 Mexico

- 5.4.4.1.3 United States

- 5.4.4.1.4 Rest of North America

- 5.4.5 South America

- 5.4.5.1 By Country

- 5.4.5.1.1 Argentina

- 5.4.5.1.2 Brazil

- 5.4.5.1.3 Chile

- 5.4.5.1.4 Rest of South America

- 5.4.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Jiangsu Yangnong Chemical Co. Ltd

- 6.4.7 Nufarm Ltd

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

農作物保護化學品市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、來源、應用方式、地區和競爭細分,2020-2030 年預測

農作物保護化學品市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、來源、應用方式、地區和競爭細分,2020-2030 年預測 中國作物保護化學品市場:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

中國作物保護化學品市場:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 亞太地區作物保護化學品:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

亞太地區作物保護化學品:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 南美作物保護化學品:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

南美作物保護化學品:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 印度作物保護化學品-市場佔有率分析、產業趨勢與統計、2025-2030年成長預測

印度作物保護化學品-市場佔有率分析、產業趨勢與統計、2025-2030年成長預測 法國作物保護化學品市場:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

法國作物保護化學品市場:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 越南作物保護化學品市場 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

越南作物保護化學品市場 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 非洲作物保護化學品市場 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

非洲作物保護化學品市場 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 全球作物保護化學品市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年

全球作物保護化學品市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年 2025 年至 2033 年,作物保護化學品市場規模、佔有率、趨勢及預測(按產品類型、產地、作物類型、形式、應用方式和地區分類)

2025 年至 2033 年,作物保護化學品市場規模、佔有率、趨勢及預測(按產品類型、產地、作物類型、形式、應用方式和地區分類)

▼