|

市場調查報告書

商品編碼

1685797

亞太生物刺激素:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)Asia-Pacific Biostimulants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

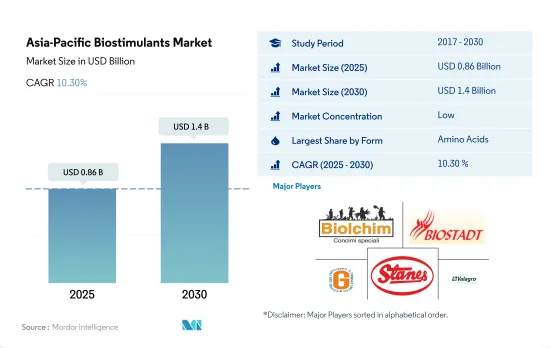

亞太生物刺激素市場規模預計在 2025 年為 8.6 億美元,預計到 2030 年將達到 14 億美元,預測期內(2025-2030 年)的複合年成長率為 10.30%。

- 現代農業在解決人類面臨的一些最嚴峻挑戰中發揮核心作用。隨著亞太地區人口的成長,農業部門面臨著滿足日益成長的糧食需求和實現糧食安全目標的壓力。

- 土壤品質惡化是該地區農民和農業工人最關心的問題。其結果是生育力、生物多樣性和生產能力的喪失。農業領域面臨的最大挑戰是擴大使用合成肥料和殺蟲劑來促進農業生產。研究表明,過量使用化學肥料可能會加速氣候危機。

- 因此,採用創新解決方案的環保、永續的農業方法已成為現代農業的標準實踐。為了確保充足的糧食生產,農業部門必須採用提高資源效率的新解決方案和方法。在這方面,生物刺激素已成為現代農業的環保且有前景的創新。胺基酸、腐植酸、富裡酸酸、海藻萃取物和蛋白質水解物是最常用的生物刺激素。

- 胺基酸是亞太地區最常用的生物刺激素,2022 年佔據最大的市場佔有率,為 25.2%。這是因為它們能夠提高植物的生產力,尤其是在生物和生物壓力條件下。

- 印度和中國等該地區領先的農業國家已經採取各種措施來推廣有機農業和永續農業投入品的使用。這些國家提供各種獎勵來推動市場發展,預計 2023 年至 2029 年期間市場價值的複合年成長率將達到 11.9%。

- 亞太地區對有機食品的需求顯著成長,從而帶動生物刺激素市場蓬勃發展。隨著印度、中國、澳洲和日本等國家大力推廣有機農業,有機種植面積預計將從2017年的310萬公頃增加到2022年的380萬公頃。因此,生物刺激素市場在2017年至2022年期間的成長率為11.5%。

- 氣候變遷的影響嚴重影響作物的生產,因此必須使用生物刺激素來緩解乾旱、鹽鹼化和溫度變化等氣候壓力。生物刺激素的使用已被證明對植物有正面的影響,有助於維持農業生態系統的生態學,減少對農藥和化學肥料的需求。

- 在亞太地區,中國、印度和澳洲已成為生物刺激素的主要業務區域。 2022年,中國將以27.6%的佔有率佔據生物刺激素市場的主導地位,其次是印度和澳洲。這些國家的政府透過提供獎勵、投資研發和設定目標來鼓勵農民採用永續的農業實踐。例如,日本設定了2050年將化學肥料和農藥使用量分別減少30.0%和50.0%的目標。

- 由於有機農業面積的不斷擴大以及對永續農業的需求,亞太地區對生物刺激素的需求正在上升。亞太生物刺激素市場預計將在未來幾年進一步成長,因為它有潛力幫助應對氣候變遷對農業的不利影響。

亞太地區生物刺激素市場趨勢

中國、印度、印尼和澳洲等國政府的支持日益增強,有助於推動該地區的有機農業

- 根據FiBL統計,2021年亞太地區有機農地面積超過370萬公頃,佔全球有機農地面積的26.4%。 2017 年至 2022 年,有機種植面積增加了 19.3%。截至 2020 年,該地區約有 183 萬家有機生產商,其中印度以 130 萬家位居榜首。中國、印度、印尼和澳洲是該地區有機種植面積最大的國家。中國和印度等國家的政府部門正在不斷推廣有機農業,以減少作物種植對化學投入的依賴。例如,印度實施了「Paramparagat Krishi Vikas Yojana」和「全印度有機農業網路計畫」(AI-NPOF)等計畫。

- 2021年,中國佔最大佔有率,為250萬公頃,佔66.1%,其次是印度、印尼和澳大利亞,分別佔19.3%、1.5%和1.4%。有機農地分為三種:連續作物、園藝作物和經濟作物。連作作物佔該地區有機農地的67.5%,2021年達250萬公頃。該地區種植的主要連作作物包括水稻、小麥、豆類、大豆和小米。

- 經濟作物將佔據第二大佔有率,到2021年將達到70萬公頃,佔有機農地的18.5%。全球對糖和有機茶等有機經濟作物的需求正在增加。中國和印度分別是世界上最大的有機綠茶和有機紅茶生產國。由於國際需求不斷成長,該地區有機種植面積預計會增加。

澳洲人均有機產品支出居首,中國有機食品市場成長強勁

- 2021 年亞太地區有機產品人均支出為 85.1 美元。 2021 年澳洲有機產品人均支出較高,為 58.3 美元,主要是由於消費者認為有機食品更健康,導致需求不斷成長。根據全球有機貿易組織的數據,2021 年澳洲有機包裝食品和飲料市場價值 8.852 億美元。

- 預計2021年中國有機食品市場將成長13.3%,預計2023年至2029年期間此積極成長模式將持續,複合年成長率約為7.1%。隨著年輕一代越來越重視有機產品,職業母親人數增加,以及健康和保健趨勢的日益普及,推動了對有機嬰兒食品的需求,預計到2025年有機產品的價值將達到64億美元。

- 印度的有機產品遠遠落後於全球需求的 1.0%,2021 年的人均支出僅 0.08 美元。然而,印度預計在未來幾年成為一個充滿希望的市場,到 2025 年將達到 1.533 億美元。目前,該地區的有機市場高度分散,有機產品僅在少數超級市場和專賣店有售。消費者知識和購買意願的提高將有助於更好地了解該地區有機食品的永續性屬性。人均收入的增加,加上消費者對食用有機食品重要性的認知不斷提高,有可能增加亞太地區人均有機食品支出。

亞太生物刺激素產業概況

亞太生物刺激素市場較為分散,前五大企業佔8.79%的市佔率。市場的主要企業有:Biolchim SpA、Biostadt India Limited、Gujarat State Fertilizers & Chemicals Ltd.、T. Stanes and Company Limited 和 Valagro(按字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 有機種植區

- 有機產品人均支出

- 法律規範

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 菲律賓

- 泰國

- 越南

- 價值鍊和通路分析

第5章市場區隔

- 形式

- 胺基酸

- 富裡酸

- 腐植酸

- 蛋白質水解物

- 海藻萃取物

- 其他生物刺激素

- 作物類型

- 經濟作物

- 園藝作物

- 田間作物

- 原產地

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 菲律賓

- 泰國

- 越南

- 其他亞太地區

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介.

- Agrinos

- Atlantica Agricola

- Biolchim SpA

- Biostadt India Limited

- Coromandel International Ltd

- Gujarat State Fertilizers & Chemicals Ltd.

- Plant Response Biotech Inc.

- Rallis India Ltd

- T. Stanes and Company Limited

- Valagro

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

The Asia-Pacific Biostimulants Market size is estimated at 0.86 billion USD in 2025, and is expected to reach 1.4 billion USD by 2030, growing at a CAGR of 10.30% during the forecast period (2025-2030).

- Modern agriculture plays a central role in solving some of humanity's most challenging problems. As the population in the Asia-Pacific region grows, the agricultural sector is under pressure to meet the rising demand for food and achieve food security goals.

- The deterioration of soil quality has become a major concern among farmers and agriculturists in the region. This has resulted in a loss of fertility, biodiversity, and production capacity. The agriculture sector's most significant challenge is the increasing use of synthetic fertilizers and pesticides to boost agricultural production. According to studies, excessive fertilizer use could hasten the climate crisis.

- As a result, environmentally friendly and sustainable farming practices with innovative solutions are now standard practices in modern agriculture. To ensure adequate food production, the agricultural sector must embrace new solutions and approaches to improve resource utilization efficiency. Biostimulants have emerged as an environmentally friendly and promising innovation for modern agriculture in this regard. Amino acids, humic acid, fulvic acid, seaweed extract, and protein hydrolysates are among the most commonly used biostimulants.

- Amino acids are the most commonly used biostimulants in the Asia-Pacific region, with the largest market share of 25.2% in 2022. This is due to their ability to enhance plant productivity, especially under abiotic and biotic stress conditions.

- Major agricultural countries in the region, such as India and China, have launched various initiatives to promote organic farming and the use of sustainable agricultural inputs. They offer various incentives that may drive the market, and as a result, the market value is anticipated to record a CAGR of 11.9% between 2023 and 2029.

- The Asia-Pacific region has witnessed a remarkable increase in the demand for organically grown food, resulting in a surge in the biostimulants market. With countries like India, China, Australia, and Japan promoting organic farming, the area under organic cultivation increased from 3.1 million hectares in 2017 to 3.8 million hectares in 2022. As a result, the biostimulants market experienced a growth rate of 11.5% between 2017-2022.

- The impact of climate change has severely affected crop production, making it imperative to use biostimulants to mitigate climate-induced stresses like drought, salinity, and temperature variations. The application of biostimulants has proven to have a positive impact on plants and helps maintain the ecological balance of agroecosystems, reducing the need for pesticides and chemical fertilizers.

- China, India, and Australia have emerged as the major business areas for biostimulants in the Asia-Pacific region. In 2022, China dominated the biostimulants market with a 27.6% share, followed by India and Australia. The governments of these countries are encouraging farmers to adopt sustainable agricultural practices by providing incentives, investing in research and development, and setting targets to meet. For instance, Japan has set a goal to reduce the usage of chemical fertilizers and pesticides by 30.0% and 50.0%, respectively, by 2050.

- The demand for biostimulants in the Asia-Pacific region is on the rise due to the increasing area under organic farming and the need for sustainable agricultural practices. The biostimulants market in the Asia-Pacific region is expected to witness further growth in the coming years, with the potential to help combat the adverse effects of climate change on agriculture.

Asia-Pacific Biostimulants Market Trends

Growing government support in countries like China, India, Indonesia, and Australia, boosts organic farming in the region

- In 2021, the area of organic agricultural land in the Asia-Pacific region exceeded 3.7 million hectares, representing 26.4% of the global organic area, according to FiBL statistics. The organic area under cultivation grew by 19.3% between 2017 and 2022. As of 2020, the region had about 1.83 million organic producers, with India leading the way with 1.3 million organic producers. China, India, Indonesia, and Australia are the major countries with large organic cultivation areas in the region. Government authorities in countries such as China and India are continuously promoting organic agriculture to reduce reliance on chemical inputs for crop cultivation. India, for instance, has implemented schemes like Paramparagat Krishi Vikas Yojana and the All India Network Programme on Organic Farming (AI-NPOF).

- In 2021, China accounted for the largest share at 66.1% with 2.5 million hectares, followed by India, Indonesia, and Australia with shares of 19.3%, 1.5%, and 1.4%, respectively. The total organic land is divided into three crop types: row crops, horticultural crops, and cash crops. Row crops occupy the largest share of organic agricultural land in the region, accounting for 67.5% with 2.5 million hectares in 2021. Major row crops grown in the region include paddy, wheat, pulses, soybeans, and millets.

- Cash crops held the second largest share, with 0.7 million hectares in 2021, accounting for an 18.5% share of organic cropland. The demand for organic cash crops, such as sugar and organic tea, is increasing globally. China and India are the largest producers of organic green tea and organic black tea, respectively, globally. The growing international demand is expected to increase the organic acreages in the region.

Per capita spending on organic product predominant in Australia and China's organic food market growing significantly

- The per capita spending on organic products in the Asia-Pacific region was recorded at USD 85.1 in 2021. Australia witnessed a higher per capita spending on organic products, with USD 58.3 in 2021, which was attributed to the higher demand due to consumers' perception of organic food as healthy. According to Global Organics Trade, the organic packed food and beverage market in Australia stood at USD 885.2 million in 2021.

- China's organic food market grew by 13.3% in 2021, and the positive growth pattern is expected to continue with an estimated CAGR of 7.1% between 2023 and 2029. With an increasing emphasis on the importance of organic products among the younger generation and a rise in demand for organic baby food due to the growing number of working mothers and the increasing adoption of the health and wellness trend, organic products are expected to reach a value of USD 6.4 billion by 2025.

- Organic products in India represent far less than 1.0% of global demand, with a per capita expenditure of just USD 0.08 in 2021. However, India represents a promising market over the coming years, reaching a value of USD 153.3 million by 2025. Currently, the market for organic goods in the region is very fragmented, with just a few supermarkets and specialty stores selling them, as only people from higher-income families are potential customers. Growing consumer knowledge and buying motivations will lead to a better understanding of the sustainability qualities of organic food in the region. Increasing per capita income, along with increased consumer awareness of the importance of organic food intake, has the potential to raise per capita expenditure on organic food items in the Asia-Pacific region.

Asia-Pacific Biostimulants Industry Overview

The Asia-Pacific Biostimulants Market is fragmented, with the top five companies occupying 8.79%. The major players in this market are Biolchim SpA, Biostadt India Limited, Gujarat State Fertilizers & Chemicals Ltd., T. Stanes and Company Limited and Valagro (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Philippines

- 4.3.7 Thailand

- 4.3.8 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Form

- 5.1.1 Amino Acids

- 5.1.2 Fulvic Acid

- 5.1.3 Humic Acid

- 5.1.4 Protein Hydrolysates

- 5.1.5 Seaweed Extracts

- 5.1.6 Other Biostimulants

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Philippines

- 5.3.7 Thailand

- 5.3.8 Vietnam

- 5.3.9 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Agrinos

- 6.4.2 Atlantica Agricola

- 6.4.3 Biolchim SpA

- 6.4.4 Biostadt India Limited

- 6.4.5 Coromandel International Ltd

- 6.4.6 Gujarat State Fertilizers & Chemicals Ltd.

- 6.4.7 Plant Response Biotech Inc.

- 6.4.8 Rallis India Ltd

- 6.4.9 T. Stanes and Company Limited

- 6.4.10 Valagro

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

全球生物刺激素市場 - 2025 至 2032 年

全球生物刺激素市場 - 2025 至 2032 年 北美生物刺激素:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)

北美生物刺激素:市場佔有率分析、產業趨勢與成長預測(2025-2030 年) 南美生物刺激素:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)

南美生物刺激素:市場佔有率分析、產業趨勢與成長預測(2025-2030 年) 生物刺激素:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

生物刺激素:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 美國生物刺激素市場:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)

美國生物刺激素市場:市場佔有率分析、產業趨勢與成長預測(2025-2030 年) 非洲生物刺激素:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)

非洲生物刺激素:市場佔有率分析、產業趨勢與成長預測(2025-2030 年) 2025年生物刺激素全球市場報告

2025年生物刺激素全球市場報告 腐植酸生物刺激素全球市場報告 2025

腐植酸生物刺激素全球市場報告 2025 2025-2033 年按產品類型、作物類型、形式、原產地、配銷通路、應用、最終用戶和地區分類的生物促效劑市場報告

2025-2033 年按產品類型、作物類型、形式、原產地、配銷通路、應用、最終用戶和地區分類的生物促效劑市場報告 生物刺激素市場規模、佔有率、成長分析,按活性成分、作物類型、應用、地區 - 產業預測,2024-2031

生物刺激素市場規模、佔有率、成長分析,按活性成分、作物類型、應用、地區 - 產業預測,2024-2031