|

市場調查報告書

商品編碼

1685818

北美資料中心冷卻:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)North America Data Center Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

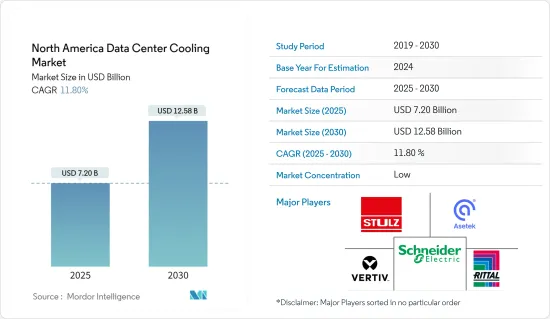

北美資料中心冷卻市場規模預計在 2025 年為 72 億美元,預計到 2030 年將達到 125.8 億美元,在市場估計和預測期(2025-2030 年)內複合年成長率為 11.8%。

各種貨櫃化、模組化和性能最佳化的資料中心(POD)設施的快速發展預計將推動資料中心對各種冷卻系統的整體需求,從而廣泛推動市場成長。

美國主導整個北美資料中心冷卻市場,這得益於超過 100MW 的主機託管和超大規模設施的發展。對具有成本效益和效率的資料中心的需求激增、擁有資料中心的企業的健康成長、各種針對環境友善資料中心解決方案的綠色舉措以及功率密度預計將推動市場成長。

此外,可攜式和液體冷卻技術的出現以及對模組化資料中心冷卻方法的日益成長的需求預計將為北美資料中心冷卻市場提供豐厚的機會。北美資料中心冷卻市場主要由日益採用的節能、經濟、環保的冷卻解決方案主導,這些解決方案符合政府機構提供的各種嚴格的環境安全法規。

此外,市場正在見證積極的產品發布和技術創新,從而極大地推動市場發展。例如,維吉尼亞州 Modine Rockbridge 工廠將於 2023 年 6 月運作5 兆瓦的先進測試實驗室,進一步擴展 Modine 為資料中心客戶提供的 Airedale 服務,並滿足資料中心產業對檢驗的永續冷卻解決方案日益成長的需求。新實驗室可容納高達 2.1 MW 的風冷式冷凍和高達 5 MW 的水冷式冷凍,可對所有空調設備進行測試。

然而,對專門基礎設施的需求、高昂的投資成本以及停電期間的各種冷卻挑戰預計將在整個預測期內限制北美資料中心冷卻市場的成長。

COVID-19 疫情讓資料中心陷入了未知領域。供應鏈中斷很常見,世界各地的停電對系統的平穩運作產生了重大影響。由於運輸中斷和工廠關閉影響了資料中心設備的交付,營運商已經找到了應對挑戰的解決方法。然而,在 COVID-19 後的預測期內,市場預計將見證各種有利可圖的成長機會。

北美資料中心冷卻市場趨勢

建築業的成長將推動對家具產品的需求

- 資訊科技(IT)產業主要包括各種營業單位(例如獨資企業、組織和夥伴關係)對資訊科技(IT)服務和相關商品的整體銷售,主要涉及使用電腦、電腦周邊設備和通訊設備搜尋、儲存、傳輸和處理資料。 IT市場還包括電腦網路、系統設計服務、廣播和資訊傳遞技術(如電話和電視)以及在此過程中使用的其他設備。這些巨大的需求正在推動整個資料中心冷卻市場的需求,因為設備需要適當的冷卻系統才能正常運作。

- 在 IT 產業,各種業務不僅需要內部私有資料存儲,還需要超大規模資料中心來滿足組織規模的需求。多年來,該地區雲端儲存的採用呈指數級成長,尤其是由於 SaaS 供應商的成長,預計將最大限度地增加對資料中心冷卻系統的需求,因為它使雲端儲存供應商能夠擴展其容量。

- 冷卻系統在 IT 和資料中心領域至關重要,主要是因為需要各種增強型和高品質的冷卻解決方案,這些解決方案的效率要比傳統的風冷解決方案高得多。此外, IT基礎設施技術創新的不斷增加以及各智慧型手機製造商對溫度控管冷卻系統的需求不斷增加也大大推動了市場的成長。

- 美國在建立推動市場成長率的各種驅動力方面發揮著至關重要的作用。這主要是由於該地區主要市場參與者增加投資和建立資料中心。例如,亞馬遜網路服務公司在2023年1月宣布,計畫在2040年投資約350億美元在維吉尼亞建立多個資料中心園區。

亞太地區預計將佔據主要市場佔有率

- 在北美,由於存在大量服務供應商,以及主機託管提供商和超大規模資料中心營運商的高額投資,預計市場將由美國主導。近年來,資料中心的數量大幅增加。為了提高資料中心的效能,在給定的空間內使用了大量處理器,從而增加了密度。密度的增加帶來電力和冷卻需求的增加。

- 美國也為銀行、IT、金融服務、保險 (BFSI)、零售和醫療保健行業的全球資料中心需求做出了重大貢獻。由於資料中心的數量及其擴張,市場利潤豐厚,該地區的資料中心服務提供者正在尋求控制其營運成本。

- 資料中心每機架功率密度平均增加1.5kW,導致氣流受限、發熱量增加。通常,IT 設備每千瓦需要 100-160 cfm 的空氣,但在高密度環境中,這一數字會降至 100 以下,導致熱量輸出增加並顯著推動市場成長。

- 行動寬頻的擴展、5G的出現、巨量資料分析和雲端運算的成長是推動美國新資料中心基礎設施需求的關鍵因素。網路供應商致力於快速部署5G,以實現更好的創新。這些發展進一步推動了美國企業對高效率資料中心冷卻解決方案和服務的需求。

- 據Cloudscene稱,截至2023年9月,美國共有5,375個資料中心,德國以522個位居第二。就資料中心總數而言,英國以517個位居第三,中國以448個位居第三。預計美國大量資料中心的存在將在整個預測期內加速市場的成長。

北美資料中心冷卻產業概況

北美資料中心冷卻市場競爭激烈且分散。施耐德電氣 SE、Black Box Corporation、Asetek、Nortek Air Solutions LLC、艾默生電氣公司、日立有限公司、Rittal GmbH &Co.KG、富士通有限公司、Stulz GmbH 和 Vertiv。隨著對創新的關注度不斷提高,對液體和可攜式冷卻技術等新技術的需求也在不斷成長,這推動了該地區進一步發展的投資。

2024 年 5 月,Stulz 推出了最新創新:CyberCool 冷卻液管理和分配裝置 (CDU)。此產品系列包含四種型號,有兩種不同尺寸。這些裝置的熱交換容量範圍很廣,從 345 kW 到 1,380 kW。 Stulz 將設施供水系統的額定供水溫度設定為 32°C,將技術冷卻系統的液體供應溫度設定為 36°C。

2024 年 3 月,Rittal Private Limited 在其位於印度班加羅爾的製造工廠開設了一個新的整合中心,專門從事冷卻裝置和液體冷卻包 (LCP) 解決方案。這項策略性舉措不僅將增強公司的生產能力,而且還將滿足日益成長的工業冷卻解決方案的需求。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況(範圍:包括與資料中心冷卻相關的當前區域趨勢的詳細分析。)

- 冷卻的主要成本考量

- 分析與資料中心營運相關的主要成本開銷,重點關注資料中心冷卻

- 資料中心冷卻的關鍵創新和發展

- 資料中心採用的主要節能技術

第5章 市場動態

- 市場促進因素(關鍵因素包括日益關注能源消耗以及轉向綠色解決方案,這些因素基於未來 5-7 年的相對影響進行繪製)

- 市場動態(根據未來5-7年內監管的動態性質和不斷變化的客戶需求等關鍵因素的相對影響繪製市場動態圖)

- 市場機會

- 封閉式與非封閉式架空地板

- 產業生態系統分析

6. 區域資料中心足跡現況分析

- 資料中心 IT 負載能力與麵積分佈區域分析(2017-2030 年)

- 對北美成熟的 DC 市場和新興 DC 熱點進行區域分析,包括重點介紹主要成熟和新興 DC 市場。

- 直流冷卻法規結構的區域分析

第 7 章資料中心冷卻市場細分

- 依冷卻技術分類(主要趨勢、市場規模、2022-2029 年估計與預測、未來展望)

- 空氣冷卻

- CRAH

- 冷卻器和節熱器

- 冷卻塔(涵蓋直接冷卻、間接冷卻及雙級冷卻)

- 其他

- 液體冷卻

- 浸入式冷卻

- 晶片直接冷卻

- 後門式熱交換器

- 空氣冷卻

- 按行業

- 資訊科技和電信

- 零售和消費品

- 衛生保健

- 媒體與娛樂

- 聯邦政府

- 其他最終用戶

- 按國家

- 美國

- 加拿大

第8章 競爭格局

- 公司簡介

- Vertiv Group Corp.

- Stulz GmbH

- Schneider Electric SE

- Rittal GmbH & Co. KG

- Asetek A/S

- Alfa Laval AB

- Iceotope Technologies Limited

- Green Revolution Cooling Inc.

- Chilldyne Inc.

- Airedale International Air Conditioning Ltd.

第9章投資分析

第10章 市場機會與未來趨勢

The North America Data Center Cooling Market size is estimated at USD 7.20 billion in 2025, and is expected to reach USD 12.58 billion by 2030, at a CAGR of 11.8% during the forecast period (2025-2030).

The rapid development of various containerized, modular, and performance-optimized data center (POD) facilities is anticipated to boost the overall demand for various cooling systems that can be utilized in the data centers, driving the market's growth extensively.

The United States dominated the total North American data center cooling market mainly due to the growth in the development of colocation and hyperscale facilities with over 100 MW power capacity. A surge in the need for cost-effective and efficient data centers, healthy growth of enterprises with data centers, various green initiatives for eco-friendly data center solutions, and power density are expected to drive the market's growth.

In addition, the emergence of portable cooling and liquid-based cooling technologies and growth in the need for a modular data center cooling approach are expected to offer lucrative opportunities for the North American data center cooling market. The solution segment had ruled the North American data center cooling market primarily due to the rising adoption of energy-efficient, cost-effective, and environment-friendly cooling solutions in line with various stringent environmental safety rules offered by governmental bodies.

Moreover, the market witnessed significant product launches and innovations, driving the market significantly. For instance, in June 2023, a 5MW, state-of-the-art testing laboratory was commissioned at the Modine Rockbridge facility in Virginia, further expanding the services that Airedale by Modine can provide data center customers and meet growing demand from the data center industry for validated, sustainable cooling solutions. The new lab can test a complete range of air conditioning equipment, accommodating air-cooled chillers up to 2.1MW and water-cooled chillers up to 5MW.

However, the need for specialized infrastructure, higher investment costs, and various cooling challenges during a power outage are expected to restrict the growth of the North American data center cooling market throughout the forecast period.

The COVID-19 pandemic placed data centers in unchartered territory. There were many supply chain disruptions, and due to lockdowns globally, the smooth operations of the systems were hugely impacted. Owing to shipping disruptions and factory closures that affected the delivery of data center equipment, operators found workarounds to meet the challenges. However, during the post-COVID-19 period, the market is expected to witness various lucrative growth opportunities throughout the forecast period.

North America Data Center Cooling Market Trends

Growth in the Construction Sector Boosting the Demand for Furniture Products

- The information technology (IT) industry primarily consists of the overall sales of information technology (IT) services and related goods by various entities such as sole traders, organizations, and partnerships that mainly apply computers, computer peripherals, and telecommunications equipment to retrieve, store, transmit and maneuver data. The IT market also involves computer networking, systems design services, broadcasting, information distribution technologies like telephones and television, and several other equipment used during the process. These huge requirements require a proper cooling system for the devices to perform normally, thereby driving the overall demand for the data center cooling market.

- The IT industry needs on-premise private data storage as well as hyperscale data centers for its various operations according to the organization's size. The rise in the adoption of cloud storage has drastically increased over the years within the region, especially due to growth in SaaS providers, allowing cloud storage providers to extend their capacities, which is anticipated to maximize the demand for data center cooling systems.

- The cooling system is essential in the IT and data center sector, primarily due to the need for various enhanced high-quality cooling solutions that are quite efficient than the traditional air-cooling solution. Also, the rise in technological innovation in the IT infrastructure, coupled with the increase in the demand for cooling systems among the various smartphone manufacturers for thermal management, is also driving the market growth extensively.

- The United States plays a very significant role in terms of establishing various driving the market's growth rate, which is mainly due to the rising investments and establishments of the data center by the key major market players within the region. For instance, in January 2023, Amazon Web Services intends to invest a sum of around USD 35 billion by 2040 to establish various multiple data center campuses across Virginia.

Asia-Pacific is Expected to Hold Significant Market Share

- The United States is poised to dominate the market in North America, owing to the presence of many services and software providers as well as high investments by colocation providers and hyper-scale data center operators. In the last few years, there has been a significant rise in the number of data centers. A considerable number of processors are being utilized in a given space to increase data centers' performance, which results in increased density. The requirement for power and cooling has grown along with increased density.

- The United States also contributes substantially to the global data center requirements from the banking, IT, financial services, and insurance (BFSI), retail, and healthcare industries. Data center service providers in the region are prompted to manage their operating costs, as the region is a lucrative market, considering the number of data centers and their expansions.

- Data centers' power density experiences growth by an average of 1.5 kW per rack, which results in limited air distribution and enhanced heat generation. In general, IT equipment typically needs between 100 and 160 cfm of air per kW, but in a dense environment, it diminishes to less than 100, which results in higher heat generation, driving the market's growth significantly.

- The expansion of mobile broadband, the emergence of 5G, growth in Big Data analytics, and cloud computing are the primary factors driving the demand for new data center infrastructures in the United States. Network providers are working to ensure the rapid implementation of 5G for better innovation. Such developments are further driving the demand for efficient data center cooling solutions and services among United States's enterprises.

- As per Cloudscene, as of September 2023, the total count of data centers in the United States was 5,375, whereas Germany ranked second with an overall count of 522 data centers. The United Kingdom ranked 3rd among countries in terms of the total number of data centers, with 517, while China recorded 448. This possession of a significant number of data centers in the United States is expected to amplify the market's growth throughout the forecast period.

North America Data Center Cooling Industry Overview

The North American data center cooling market is highly competitive and fragmented. Market penetration is growing with a strong presence of major players, such as Schneider Electric SE, Black Box Corporation, Asetek, Nortek Air Solutions LLC, Emerson Electric Co., Hitachi Ltd, Rittal GmbH & Co. KG, Fujitsu Ltd, Stulz GmbH, and Vertiv, in established markets. With the increasing focus on innovation, the demand for new technologies, such as liquid-based cooling and portable cooling technologies, is also growing, which, in turn, is driving investments for further developments in the region.

In May 2024, Stulz unveiled its latest innovation, the CyberCool Coolant Management and Distribution Unit (CDU), specifically engineered to optimize heat exchange efficiency in liquid cooling solutions. The product line comprises four models, available in two distinct sizes. These units boast an impressive heat exchange capacity, ranging from 345 kW to 1,380 kW. Stulz has set the rated water supply temperature for the facility water system at 32°C (89.6°F), with the liquid supply temperature for the technology cooling system pegged at 36°C (96.8°F).

In March 2024, Rittal Private Limited marked the opening of its new Integration Center, specifically tailored for Cooling Units and Liquid Cooling Package (LCP) solutions, at its Bangalore, India manufacturing plant. This strategic move not only bolsters the company's production capabilities but also positions it to cater to the escalating demand for Industrial Cooling Solutions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview (Coverage: A detailed analysis of the current regional trends related to Data Center Cooling are included in this section)

- 4.2 Key cost considerations for Cooling

- 4.2.1 Analysis of the key cost overheads related to DC operations with an eye on DC Cooling

- 4.2.2 Key innovations and developments in Data Center Cooling

- 4.2.3 Key energy efficiency practices adopted in Data Centers

5 MARKET DYNAMICS

- 5.1 Market Drivers (Key factors such as the increased emphasis on energy consumption, move towards green solutions are mapped based on their relative impact over the next 5-7 years)

- 5.2 Market Challenges (Key factors such as the dynamic nature of regulations, evolving customer needs are mapped based on their relative impact over the next 5-7 years)

- 5.3 Market Opportunities

- 5.4 Comparison of raised floor with containment & raised floor without commitment

- 5.5 Industry Ecosystem Analysis

6 ANALYSIS OF THE CURRENT REGIONAL DATA CENTER FOOTPRINT

- 6.1 Regional Analysis of IT Load Capacity & Area Footprint of Data Centers (for the period of 2017-2030)

- 6.2 Regional Analysis of the Established DC Markets and Emerging DC Hotspots in North America region (we will include coverage by highlighting major established and emerging DC markets)

- 6.3 Regional Analysis of Regulatory Framework On DC Cooling

7 DATA CENTER COOLING MARKET SEGMENTATION

- 7.1 By Cooling Technology (Key trends, market size estimates & projections for the period of 2022-2029 and future outlook)

- 7.1.1 Air-based Cooling

- 7.1.1.1 CRAH

- 7.1.1.2 Chiller and Economizer

- 7.1.1.3 Cooling Tower (covers direct, indirect & two-stage cooling)

- 7.1.1.4 Others

- 7.1.2 Liquid-based Cooling

- 7.1.2.1 Immersion Cooling

- 7.1.2.2 Direct-to-Chip Cooling

- 7.1.2.3 Rear-Door Heat Exchanger

- 7.1.1 Air-based Cooling

- 7.2 By End-user Vertical

- 7.2.1 IT & Telecom

- 7.2.2 Retail & Consumer Goods

- 7.2.3 Healthcare

- 7.2.4 Media & Entertainment

- 7.2.5 Federal & Institutional agencies

- 7.2.6 Other end-users

- 7.3 By Country

- 7.3.1 United States

- 7.3.2 Canada

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Vertiv Group Corp.

- 8.1.2 Stulz GmbH

- 8.1.3 Schneider Electric SE

- 8.1.4 Rittal GmbH & Co. KG

- 8.1.5 Asetek A/S

- 8.1.6 Alfa Laval AB

- 8.1.7 Iceotope Technologies Limited

- 8.1.8 Green Revolution Cooling Inc.

- 8.1.9 Chilldyne Inc.

- 8.1.10 Airedale International Air Conditioning Ltd.

9 INVESTMENT ANALYSIS

10 MARKET OPPORTUNITIES AND FUTURE TRENDS

資料中心冷卻市場規模、佔有率及成長分析(按組件、資料中心類型、冷卻類型、最終用途產業和地區)-2025-2032 年產業預測

資料中心冷卻市場規模、佔有率及成長分析(按組件、資料中心類型、冷卻類型、最終用途產業和地區)-2025-2032 年產業預測 資料中心浸入式冷卻市場按技術類型、組件和最終用戶分類 - 2025-2030 年全球預測

資料中心浸入式冷卻市場按技術類型、組件和最終用戶分類 - 2025-2030 年全球預測 2025年資料中心冷卻全球市場報告2030 年資料中心冷卻市場預測:按資料中心類型、組件、冷卻技術、最終用戶和地區進行的全球分析

2025年資料中心冷卻全球市場報告2030 年資料中心冷卻市場預測:按資料中心類型、組件、冷卻技術、最終用戶和地區進行的全球分析 中國資料中心冷卻:市場佔有率分析、產業趨勢與統計、成長預測(2025-2031)中東和非洲的資料中心冷卻:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)亞太資料中心冷卻:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)拉丁美洲資料中心冷卻:市場佔有率分析、產業趨勢與成長預測(2025-2031)歐洲資料中心冷卻:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)資料中心冷卻:市場佔有率分析、產業趨勢與統計、成長預測(2025-2031)

中國資料中心冷卻:市場佔有率分析、產業趨勢與統計、成長預測(2025-2031)中東和非洲的資料中心冷卻:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)亞太資料中心冷卻:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)拉丁美洲資料中心冷卻:市場佔有率分析、產業趨勢與成長預測(2025-2031)歐洲資料中心冷卻:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)資料中心冷卻:市場佔有率分析、產業趨勢與統計、成長預測(2025-2031)