|

市場調查報告書

商品編碼

1626313

拉丁美洲玻璃包裝:市場佔有率分析、行業趨勢、統計和成長預測(2025-2030)Latin America Glass Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

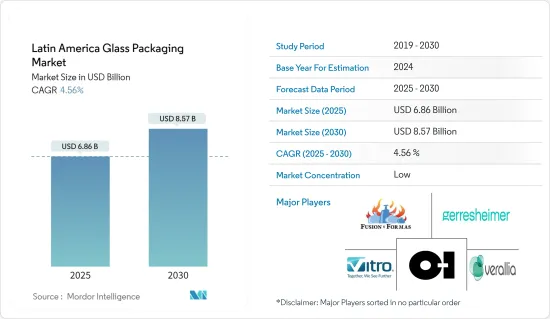

拉丁美洲玻璃包裝市場規模預計到2025年為68.6億美元,預計到2030年將達到85.7億美元,預測期內(2025-2030年)複合年成長率為4.56%。

對於注重健康、口味和環境安全的消費者來說,玻璃包裝是可靠的選擇。玻璃包裝因其奢華的感覺、保持產品新鮮度並確保保護而受到重視。此外,對環保產品的需求不斷成長以及食品和飲料市場的蓬勃發展正在推動玻璃包裝市場的成長。

主要亮點

- 隨著消費者關注安全和健康的包裝,玻璃包裝在多個類別中都在成長。此外,壓花、成型和藝術飾面等技術創新正在增加玻璃包裝對最終用戶的吸引力。

- 在都市化、消費者偏好變化以及對飲料和酒精飲料的需求不斷成長的推動下,越來越多的製造商開始採用玻璃包裝。據聯合國稱,拉丁美洲和加勒比地區是都市化最高的地區,80%的人口居住在都市區。鑑於這些動態,未來幾年市場可能會經歷適度成長。

- 儘管玻璃作為各種產品的包裝材料仍然受到青睞,但擴大採用塑膠作為替代品,這對市場成長構成了挑戰。此外,塑膠在更安全應用方面的進步進一步限制了玻璃作為包裝材料的範圍。

- 近年來,人們的環保意識有所增強。企業和消費者都越來越意識到他們的選擇如何影響地球。同時,政策制定者正在創建框架並做出決策,以加強永續性工作。因此,永續性已牢牢地列入全球議程,影響社會、經濟和政策辯論,並推動對玻璃包裝的需求。

- 市場也面臨挑戰。一些拉丁美洲國家的回收基礎設施不發達,導致玻璃廢棄物的收集和處理變得複雜。因此,玻璃廢棄物經常被送往掩埋或焚化廠。玻璃與塑膠等包裝材料競爭,塑膠具有成本優勢,應用範圍廣泛。

拉丁美洲玻璃包裝市場趨勢

飲料領域需求的增加預計將推動市場

- 近年來,拉丁美洲飲料的推出和銷售有所增加。對酒精和非酒精飲料玻璃包裝的需求不斷成長,促使公司在巴西建立製造地。

- 巴西成年人和年輕人每週飲用軟性飲料五天或以上的比例不斷增加,這表明巴西對軟性飲料的需求增加。這種消費量的成長可能會對軟性飲料產業對玻璃瓶的需求產生正面影響。

- 根據巴西地區統計研究所的數據,2019年烈酒和其他飲料生產收益為902.11美元,2023年將達到9.4932億美元。因此,隨著軟性飲料消費量的增加,對玻璃瓶作為滿足消費者偏好和市場需求的包裝選擇的需求也會隨之增加。

- 據哥蘭比亞營養公司稱,拉丁美洲對天然能量飲料的需求不斷成長。 69% 的墨西哥消費者對能為他們提供全天能量的產品感興趣,使他們更有可能更長時間地保持精力充沛。

- 此外,擴大轉向更健康、潔淨標示的選擇正在塑造拉丁美洲的機能飲料模式。未來主要的成長領域包括「蛋白質+」飲料,其中包括富含蛋白質的能量飲料,可以添加多種健康成分,而不添加糖或卡路里。對於希望進入拉丁美洲市場的製造商來說,與熟悉飲料創新和區域細微差別的飲料配料供應商合作至關重要。

預計墨西哥市場將穩定擴張

- 預計該國包裝設備的快速技術發展和生活方式的快速變化將推動預測期內的市場成長。墨西哥因其豐富的自然資源、低成本勞動力和不斷成長的消費者支出而吸引外國玻璃包裝製造商和其他公司。

- 根據國家統計和地理研究所(INEGI)的報告,墨西哥可樂飲料的產量正在增加,推動了對玻璃包裝的需求。 2023年4月,可樂飲料銷售量達到近11.1億公升,較上季增加。銷量的激增凸顯了玻璃包裝的需求,以適應飲料產業產量的增加。

- 此外,將小型生產商合併到 LaLa 和 Alpura 等大型合作社和公司中可以提高效率和規模經濟。液態奶產量的增加預計將支持乳製品行業對玻璃包裝的需求。隨著產量的增加,對包括玻璃瓶在內的包裝材料的需求預計也會增加,以適應流質食品產量的增加。據糧農組織和美國農業部稱,隨著酪農生產效率的提高,酪農行業對玻璃瓶等包裝解決方案的需求預計將會增加。

- 根據龍舌蘭酒監管委員會的數據,2019 年龍舌蘭酒產量為 351.7 公升。在墨西哥,人均純酒精消費量為4.9公升,男性消費量多於女性。值得注意的是,18-29歲年齡層的人均消費量為7.6公升,位居榜首。

- 此外,2023年10月,可口可樂將投資1.33億美元擴大其位於墨西哥哈利斯科州Jugos del Valle-Santa Clara工廠的乳製品和果汁生產,預計將增加對玻璃包裝的需求。隨著產量的增加,對包括玻璃瓶在內的包裝材料的需求可能會增加,以適應乳製品和果汁產品產量的增加。這項投資標誌著飲料產業(尤其是墨西哥)的成長,並可能刺激對玻璃包裝的需求。

拉丁美洲玻璃包裝產業概況

拉丁美洲玻璃包裝市場較為分散,國內和國際公司很少,包括: Vitro SAB de CV、Fusion y Formas SA de CV、Gerresheimer AG、Owens-Illinois Inc. 和 Verallia Group 為了維持市場佔有率,公司不斷創新並建立策略合作夥伴關係。

- 2024年7月,Vitro Glass Containers在墨西哥托盧卡工廠完成了一座新熔爐,將香水和酒精飲料產業的產能提高了50%以上。這座新熔爐投資 7,000 萬美元,日產量可達 230 噸。此次升級將使 Vitro 的托盧卡工廠躋身全球最大的玻璃容器製造商行列,專門生產化妝品、優質酒精飲料和特色產品。該熔爐採用尖端技術製造,旨在最佳化能源消耗並顯著減少二氧化碳排放。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買方議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 產業生態系統分析

第5章市場動態

- 市場促進因素

- 對環保產品的需求不斷增加

- 食品和飲料市場需求增加

- 市場限制因素

- 營運成本增加

- 擴大替代產品(塑膠)的使用

第6章 市場細分

- 依產品類型

- 瓶子

- 管瓶

- 安瓿

- 罐

- 其他產品類型

- 按最終用戶產業

- 飲料

- 酒精飲料

- 啤酒/蘋果酒

- 葡萄酒和烈酒

- 其他酒精飲料

- 非酒精性

- 碳酸飲料

- 牛奶

- 水

- 其他非酒精飲料

- 食品

- 個人護理和化妝品

- 醫療保健和製藥

- 其他最終用戶產業

- 飲料

- 按國家/地區

- 巴西

- 墨西哥

- 阿根廷

第7章 競爭格局

- 公司簡介

- Corning Incorporated

- Heinz-Glas Gmbh & Co. KgaA

- Verallia Group

- Owens-Illinois Inc.

- Gerresheimer AG

- Fusion and Forms SA de CV

- Vitro SAB de CV

- Saverglass SAS

第8章投資分析

第9章 市場的未來

The Latin America Glass Packaging Market size is estimated at USD 6.86 billion in 2025, and is expected to reach USD 8.57 billion by 2030, at a CAGR of 4.56% during the forecast period (2025-2030).

Glass packaging is a trusted choice for consumers prioritizing health, taste, and environmental safety. Glass packaging, valued for its premium nature, preserves product freshness and ensures protection. Additionally, the surging demand for eco-friendly products, coupled with a booming food and beverage market, propels the growth of the glass packaging market.

Key Highlights

- As consumers place a premium on safe and health-conscious packaging, glass packaging is experiencing growth across multiple categories. Furthermore, technological innovations, such as embossing, shaping, and artistic finishes, amplify the appeal of glass packaging for end users.

- Driven by urbanization, shifting consumer preferences, and rising demand for beverages and alcoholic drinks, manufacturers are increasingly turning to glass packaging solutions. The United Nations reports that with 80% of its population residing in cities, Latin America and the Caribbean stand out as the most urbanized regions. Given these dynamics, the market is set for moderate growth in the coming years.

- While glass continues to be the favored packaging material for a range of products, the rising adoption of plastics as a substitute poses a challenge to the market's growth. Moreover, plastic advancements for safer applications further limit the scope of glass as a packaging material.

- In recent years, environmental awareness has surged. Companies and consumers are increasingly mindful of how their choices impact the planet. Concurrently, policymakers are crafting frameworks and making decisions to bolster sustainability efforts. As a result, sustainability has firmly established itself on the global agenda, influencing societal, economic, and policy discussions and subsequently driving the demand for glass packaging.

- The market also faces challenges. Several Latin American nations need help with underdeveloped recycling infrastructures, which complicate the collection and processing of glass waste. Consequently, this often results in glass waste being diverted to landfills or incineration. Glass contends with packaging rivals like plastic, which frequently offer cost advantages and enjoy broader usage.

Latin America Glass Packaging Market Trends

Increasing Demand from the Beverages Segment is Expected to Drive the Market

- In Latin America, beverage launches and sales have risen over the past few years. The increasing demand for glass packaging from alcoholic and non-alcoholic beverages has drawn players to establish their manufacturing units in Brazil.

- The increase in the percentage of adults and young adults in Brazil consuming soft drinks five or more days per week, as reported by Ministerio daSaude, indicates an increasing demand for soft drinks in the country. This rise in consumption is likely to positively impact the demand for glass bottles in the soft drink industry.

- According to the Brazilian Institute of Geography and Statistics, the revenue from the manufacturing of spirits and other beverages in 2019 was USD 902.11 and reached USD 949.32 million in 2023. Therefore, as the consumption of soft drinks increases, there will likely be a corresponding increase in the demand for glass bottles as packaging options to meet consumer preferences and market demand.

- According to Glanbia Nutritionals, in Latin America, there is a rising demand for beverages that boost natural energy. A significant 69% of Mexican consumers express interest in products that sustain their energy throughout the day, underscoring the demand for prolonged vitality.

- Moreover, the ongoing shift toward healthier, clean-label choices is set to shape the functional beverage landscape in Latin America. Key growth areas on the horizon include "protein +" beverages, which encompass protein-infused energy drinks that can integrate a variety of healthy ingredients without sugar or calories. Partnering with a beverage ingredient supplier that is well-versed in beverage innovation and regional nuances is paramount for manufacturers eyeing the Latin American market.

Mexico is Expected to Witness Robust Expansion in the Market

- Rapid technological growth in packaging equipment and changing busy lifestyles in the country are anticipated to drive the market's growth during the forecast period. Mexico attracted foreign glass packaging makers and other companies owing to abundant natural resources, low-cost labor, and increasing consumer expenditure.

- The growing production of cola drinks in Mexico, as reported by the National Institute of Statistics and Geography (INEGI), is driving the demand for glass packaging. In April 2023, the sales volume of cola drinks totaled nearly 1.11 billion liters, marking an increase from the previous month. This surge in sales highlights the need for glass packaging to accommodate the rising production levels in the beverage industry.

- Additionally, integrating small-scale producers into larger cooperatives or companies, like LaLa and Alpura, enhances efficiency and economies of scale. This growth in fluid milk production is expected to support the demand for glass packaging in the dairy segment. With increased production levels, there will be a greater need for packaging materials, including glass bottles, to accommodate the expanded output of fluid milk. According to the FAO and the US Department of Agriculture, as dairy operations become more efficient, the demand for packaging solutions like glass bottles is expected to rise in the dairy industry.

- According to Consejo Regulador del Tequila, the production volume of tequila in 2019 was 351.7 liters. In Mexico, the average per capita consumption of pure alcohol stands at 4.9 liters, with men outpacing women in consumption. Notably, the 18-29 age group leads with a per capita consumption of 7.6 liters.

- Further, in October 2023, Coca-Cola's investment of USD 133 million to expand dairy and juice production at Jugosdel Valle-Santa Clara's plant in Jalisco, Mexico, is expected to support the demand for glass packaging. As production increases, there will likely be a corresponding need for packaging materials, including glass bottles, to accommodate the expanded output of dairy and juice products. This investment signals growth in the beverage sector, particularly in Mexico, which can stimulate demand for glass packaging.

Latin America Glass Packaging Industry Overview

The Latin American glass Packaging Market is fragmented, with few domestic and international players such as Vitro SAB de CV, Fusion y Formas SA de CV, Gerresheimer AG, Owens-Illinois Inc., and Verallia Group. To retain their market share, companies keep on innovating and entering into strategic partnerships.

- July 2024: Vitro Glass Containers completed the anniversary of a new furnace at its Toluca plant in Mexico, boosting its capacity to cater to the perfumery and liquor segments by over 50%. This USD 70 million investment in the new furnace is set to produce 230 tons daily. With this upgrade, Vitro's Toluca facility positions itself among the world's largest producers of glass containers, specifically targeting cosmetic products, premium liquors, and specialty items. The furnace, crafted with cutting-edge technology, aims to optimize energy consumption and significantly reduce CO2 emissions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Ecosystem Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Eco-friendly Products

- 5.1.2 Rising Demand from the Food and Beverage Market

- 5.2 Market Restraints

- 5.2.1 Rising Operational Costs

- 5.2.2 Growing Usage of Substitute Products (Plastic)

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Bottles

- 6.1.2 Vials

- 6.1.3 Ampoules

- 6.1.4 Jars

- 6.1.5 Other Product Type

- 6.2 By End-user Industry

- 6.2.1 Beverages

- 6.2.1.1 Alcoholic**

- 6.2.1.1.1 Beer and Cider

- 6.2.1.1.2 Wine and Spirit

- 6.2.1.1.3 Other Alcoholic Beverages

- 6.2.1.2 Non-Alcoholic**

- 6.2.1.2.1 Carbonated Soft Drinks

- 6.2.1.2.2 Milk

- 6.2.1.2.3 Water

- 6.2.1.2.4 Other Non-Alcoholic Beverages

- 6.2.2 Food

- 6.2.3 Personal Care and Cosmetics

- 6.2.4 Healthcare and Pharmaceutical

- 6.2.5 Other End-user Industries

- 6.2.1 Beverages

- 6.3 By Country

- 6.3.1 Brazil

- 6.3.2 Mexico

- 6.3.3 Argentina

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Corning Incorporated

- 7.1.2 Heinz-Glas Gmbh & Co. KgaA

- 7.1.3 Verallia Group

- 7.1.4 Owens-Illinois Inc.

- 7.1.5 Gerresheimer AG

- 7.1.6 Fusion and Forms SA de CV

- 7.1.7 Vitro SAB de CV

- 7.1.8 Saverglass SAS

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

中東和非洲的玻璃包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030)

中東和非洲的玻璃包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030) 亞太玻璃包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

亞太玻璃包裝:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 北美玻璃包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030)

北美玻璃包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030) 印度玻璃包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

印度玻璃包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 德國玻璃包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)

德國玻璃包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030) 法國玻璃包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

法國玻璃包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 美國玻璃包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030)

美國玻璃包裝:市場佔有率分析、產業趨勢、成長預測(2025-2030) 英國玻璃包裝:市場佔有率分析、產業趨勢與成長預測(2025-2030)

英國玻璃包裝:市場佔有率分析、產業趨勢與成長預測(2025-2030) 北美棕色玻璃包裝市場:市場規模、佔有率、趨勢分析(按產品、應用和地區)、細分市場預測(2025-2030 年)

北美棕色玻璃包裝市場:市場規模、佔有率、趨勢分析(按產品、應用和地區)、細分市場預測(2025-2030 年) 玻璃包裝市場市場規模、佔有率、成長分析,按材料、按產品、按應用、按地區 - 按行業預測,2024-2031 年

玻璃包裝市場市場規模、佔有率、成長分析,按材料、按產品、按應用、按地區 - 按行業預測,2024-2031 年