|

市場調查報告書

商品編碼

1628708

日本塑膠包裝:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)Japan Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

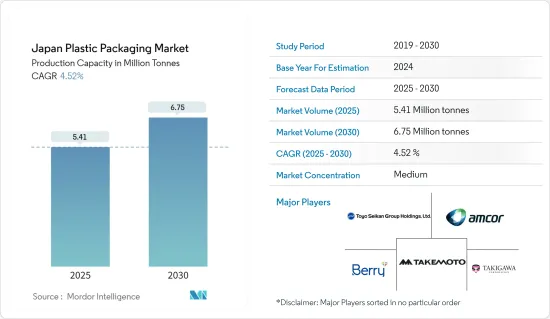

以產能計算,日本塑膠包裝市場規模預計將從2025年的541萬噸成長到2030年的675萬噸,預測期間(2025-2030年)複合年成長率為4.52%。

食品和飲料業正在推動日本的塑膠包裝市場。塑膠包裝因其重量輕、不易破碎且易於處理而深受消費者歡迎。

主要亮點

- 在日本,消費者青睞塑膠包裝,因為其耐用性、靈活性和成本效益。這種形式的包裝使用塑膠薄膜、容器和其他聚合物材料來形成針對外部因素的屏障。這種多功能性使其成為包裝各種產品的輕量級解決方案。食品和飲料、化妝品和藥品等行業越來越依賴塑膠包裝,這推動了對其產品的需求。

- 日本塑膠容器和包裝製造商透過專注於為不同的最終用途行業開發剛性和軟性包裝解決方案,有望實現顯著成長。 2024年10月,凸版株式會社與RM Tohcello和三井化學株式會社合作,成功開發出可大量生產的再生BOPP薄膜。樣品分發將於 2024 年 10 月開始。

- 新灌裝技術和耐熱寶特瓶的出現擴大了國內市場的可能性。為了滿足不斷成長的需求,飲料製造商正在日本提高寶特瓶的產量。

- 2024 年 9 月,可口可樂裝瓶日本公司 (CCBJI) 宣佈在愛知縣東海工廠建造一條新的無菌生產線。該生產線的生產能力約為每分鐘 600 個小寶特瓶,將增強 CCBJI應對力。

- 然而,塑膠廢棄物的激增導致日本消費者尋求更環保的包裝材料,例如玻璃和金屬。該地區鋁和玻璃的使用顯著增加,這些材料被認為是可回收且環保的。這種遠離塑膠的轉變可能會對未來的產品需求帶來挑戰。

日本塑膠包裝市場趨勢

瓶子和罐子主導市場的前景

- 塑膠的輕質特性正在推動需求成長。在日本,食品和飲料行業對寶特瓶和罐的依賴日益增加,推動了對塑膠包裝的需求。

- 寶特瓶的用途已擴展到飲料之外,目前在日本化妝品和製藥領域備受關注。隨著先進填充技術和耐熱寶特瓶的推出等創新,市場動態不斷發展。雖然寶特瓶在各個領域都處於領先地位,但聚乙烯 (PE) 瓶是飲料、化妝品、衛生用品和清潔劑等家用產品的首選。

- 日本公司正在增加飲料用寶特瓶的產量,這一趨勢將推動市場成長。 2024年3月,日本大塚食品公司宣布計劃推出碳酸維生素飲料「MATCH」系列兩款新產品:500ml寶特瓶「MATCH鳳梨汽水」和260g寶特瓶「MATCH鳳梨汽水」匹配果凍」。

- 日本軟性飲料協會的宏偉目標是到 2030 年實現 50% 的瓶對瓶回收率。工業公司正在努力使寶特瓶變得更輕,以減少 PET 樹脂的使用量。日本軟性飲料協會(JSDA)的資料顯示,在日本非酒精飲料領域, 寶特瓶已超過鋼瓶和玻璃瓶。此外,嚴格的政府法規使日本成為寶特瓶收集和回收的全球領導者,這是刺激市場成長的因素。

- 據經濟產業省報告稱,2023年日本塑膠包裝產量與前一年同期比較減少10萬噸(9.01%)。然而,預測顯示 2024 年將反彈至 109 萬噸,顯示市場潛在成長。

飲料業成長顯著

- 在健康飲料需求不斷成長的推動下,日本飲料業正在大幅擴張。消費者越來越傾向於那些承諾對健康有益的飲料,例如增強免疫力、改善消化和增強認知功能。這種趨勢在老年人和麵臨與生活方式相關的健康挑戰的人中尤其明顯。

- 在日本,硬質塑膠包裝(常見於寶特瓶和容器)廣泛支持食品和飲料應用。使用 HDPE 和寶特瓶包裝果汁、碳酸軟性飲料和其他飲料,大大推動了對這些產品的需求。值得注意的是,像東洋製罐這樣的製造商生產專門用於飲料用途的耐熱耐壓寶特瓶。

- 注重天然成分與科學進步結合的技術創新正在重塑日本的飲料產業。 2024年,軟性飲料、運動飲料、能量飲料等細分市場將代表消費者對機能飲料的多樣化偏好。透過優先考慮創新、有針對性的行銷和永續性,公司可以在日本快速成長的機能飲料領域中取得一席之地。

- 此外,根據美國農業部(USDA)的資料,2023年日本非酒精飲料市場價值約400億美元,其中進口額約為10億美元。美國是日本非酒精飲料的主要供應國,出口主要為礦泉水和果汁。健康飲料和無酒精啤酒正在成為主要消費趨勢,極大地影響了塑膠包裝的需求。

- 日本對非酒精飲料的強勁購買興趣正在加強塑膠包裝領域。日本領先企業朝日集團控股公司的報告顯示,到 2023 年,即飲茶將引領軟性飲料領域,約佔銷售額的 30%。日本非酒精飲料類型的多樣性推動了對剛性和軟包裝解決方案的需求。

日本塑膠包裝產業概況

日本塑膠包裝市場主要由 Amcor Group、Takemoto Yohki、Toyo Seikan Group Holdings Ltd、Berry Global Inc. 和 Takikawa Corporation 等公司組成,這些公司積極尋求產品創新、合作和併購,以擴大業務並提高產量。市場佔有率。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵對關係

第5章市場動態

- 市場促進因素

- 日本多個最終用戶產業對塑膠包裝解決方案的需求不斷成長

- 塑膠飲料瓶在日本越來越受歡迎

- 市場問題

- 日本對塑膠包裝回收的環境擔憂日益嚴重

第6章 行業法規、政策與標準

第7章 市場區隔

- 按包裝類型

- 軟質塑膠包裝

- 硬質塑膠包裝

- 依產品類型

- 瓶子和罐子

- 托盤和容器

- 小袋

- 包包

- 薄膜包裝

- 其他

- 按行業分類

- 食物

- 飲料

- 醫療保健

- 個人護理和家居產品

- 其他

第8章 競爭格局

- 公司簡介

- Amcor Group

- Takemoto Yohki Co. Ltd.

- Berry Global

- Takigawa Corporation

- Toyo Seiken Group Holdings Ltd.

- Sonoco Products Company

- Sealed Air Corporation

- Hosokawa Yoko Co. ltd.

- Toppan Inc.

- Kodama Plastics Co. Ltd.

- 熱圖分析

- 競爭對手分析 -新興企業與老牌公司

第9章投資分析

第10章市場的未來

The Japan Plastic Packaging Market size in terms of production capacity is expected to grow from 5.41 million tonnes in 2025 to 6.75 million tonnes by 2030, at a CAGR of 4.52% during the forecast period (2025-2030).

The food and beverage industry drives the plastic packaging market in Japan. Consumers favor plastic packaging for its lightweight and unbreakable nature, enhancing ease of handling.

Key Highlights

- In Japan, consumers favor plastic packaging for its durability, flexibility, and cost-effectiveness. This packaging form employs plastic films, containers, and other polymer-based materials, creating a barrier against external elements. This versatility makes it a lightweight solution for packaging various goods. Industries such as beverage, food, cosmetics, and pharmaceuticals increasingly rely on plastic container packaging, which drives the product demand.

- Japanese manufacturers of plastic packaging are poised for substantial growth by focusing on the development of both rigid and flexible packaging solutions tailored to diverse end-use industries. In October 2024, Toppan Inc., in collaboration with RM Tohcello Co. Ltd. and Mitsui Chemicals Inc., has successfully created a recycled BOPP film primed for mass production. Starting October 2024, these companies will commence the distribution of samples for this innovative film.

- New filling technologies and the advent of heat-resistant PET bottles have broadened market possibilities in the country. In response to rising demand, beverage manufacturers are ramping up PET bottle production in Japan.

- In September 2024, Coca-Cola Bottlers Japan Inc. (CCBJI) unveiled a new aseptic production line at its Tokai Plant in Aichi Prefecture. This line boasts a production capacity of around 600 small PET bottles per minute, bolstering CCBJI's ability to meet surging demand.

- However, a surge in plastic waste has led Japanese consumers to gravitate towards eco-friendlier packaging materials such as glass and metal. The region has seen a notable uptick in the adoption of aluminum and glass, celebrated for their recyclability and eco-friendly attributes. This shift away from plastic could pose challenges for product demand in the future.

Japan Plastic Packaging Market Trends

Bottles and Jars Segment is Expected to Dominate the Market

- The lightweight nature of plastics fuels their rising demand. In Japan, the food and beverage sector's increasing reliance on plastic bottles and jars propels the need for plastic packaging.

- Plastic bottles extend their utility beyond beverages, finding prominence in Japan's cosmetics and pharmaceuticals sectors. Market dynamics are evolving with innovations like advanced filling technologies and the launch of heat-resistant PET bottles. While PET bottles lead in various sectors, polyethylene (PE) bottles are the preferred choice for beverages, cosmetics, sanitary items, and household items such as detergents.

- Japanese companies are increasingly producing PET bottles for beverages, a trend poised to fuel market growth. In March 2024, Otsuka Foods Co., Ltd., a prominent player based in Japan, unveiled its plans to launch two new products in its MATCH line of carbonated vitamin drinks: MATCH Pineapple Soda in a 500-ml PET bottle and MATCH Jelly in a 260-gram PET bottle in the Japanese market.

- The Japan Soft Drink Association has set an ambitious goal of achieving 50% bottle-to-bottle recycling by 2030. Industry players are lightening the weight of PET bottles to reduce the amount of PET resin used. Data from the Japan Soft Drink Association (JSDA) highlights that PET bottles have overtaken steel and glass in the country's non-alcoholic beverage sector. Furthermore, stringent government regulations have positioned Japan as a global leader in PET bottle collection and recycling, a factor poised to stimulate market growth.

- As reported by the Ministry of Economy, Trade and Industry (METI) Japan, the country's plastic packaging production saw a dip of 0.1 million tons (-9.01 percent) in 2023 compared to the prior year. However, projections indicate a rebound to 1.09 million tons in 2024, signaling potential market growth.

Beverage Industry Set for Significant Growth

- Japan's beverage industry is expanding significantly, fueled by a rising demand for health-oriented drinks. Consumers are increasingly gravitating towards beverages that promise health benefits, including immunity enhancement, better digestion, and sharper cognitive functions. This trend is especially evident among the elderly and those facing health challenges linked to their lifestyles.

- In Japan, rigid plastic packaging, commonly found in plastic bottles and containers, is widely favored for food and beverage applications. The demand for these products is notably driven by the use of HDPE and PET bottles for packaging juices, carbonated soft drinks, and other beverages. Notably, manufacturers such as Toyo Seikan Co. Ltd. are producing heat and pressure-resistant PET bottles tailored specifically for beverage applications.

- Innovations are reshaping Japan's beverage landscape, with a focus on merging natural ingredients and scientific advancements. In 2024, segments such as soft drinks, sports drinks, and energy drinks are poised to showcase the varied consumer preferences for functional beverages. By prioritizing innovation, targeted marketing, and sustainability, companies can cement their foothold in Japan's burgeoning functional beverage arena.

- Additionally, data from the US Department of Agriculture (USDA) reveals that Japan's non-alcoholic beverage market was valued at approximately USD 40 billion in 2023, with imports accounting for about USD 1 billion. The U.S. stands as Japan's chief supplier of non-alcoholic drinks, with exports predominantly comprising mineral water and juices. Healthy beverages and non-alcoholic beers are emerging as leading consumer trends, significantly influencing the demand for plastic packaging.

- Japan's surging appetite for non-alcoholic drinks is bolstering its plastic packaging sector. As reported by Asahi Group Holdings, a prominent Japanese firm, Ready-to-Drink (RTD) tea led the soft drinks segment in 2023, capturing roughly 30% of sales. The diverse range of non-alcoholic beverages in Japan is driving a heightened demand for both rigid and flexible packaging solutions in the nation.

Japan Plastic Packaging Industry Overview

The Japanese plastic packaging market is moderately consolidated with the presence of global and domestic players such as Amcor Group, Takemoto Yohki Co. Ltd, Toyo Seikan Group Holdings Ltd, Berry Global Inc. and Takigawa Corporation. These companies are actively pursuing strategies such as product innovations, collaborations, mergers and acquisitions, and investments to expand their business and capture a larger market share.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand of Plastic Packaging Solutions for Multiple End-User Industries in Japan

- 5.1.2 Rising Popularity of Plastic Bottles for Beverage Industry in Japan

- 5.2 Market Challenges

- 5.2.1 Increasing Environmental Concerns Regarding Plastic Packaging Recycling in Japan

6 INDUSTRY REGULATION, POLICY AND STANDARDS

7 MARKET SEGEMENTATION

- 7.1 By Packaging Type

- 7.1.1 Flexible Plastic Packaging

- 7.1.2 Rigid Plastic Packaging

- 7.2 By Product Type

- 7.2.1 Bottles and Jars

- 7.2.2 Trays and containers

- 7.2.3 Pouches

- 7.2.4 Bags

- 7.2.5 Films and Wraps

- 7.2.6 Other Product Types

- 7.3 By End-User Vertical

- 7.3.1 Food

- 7.3.2 Beverage

- 7.3.3 Healthcare

- 7.3.4 Personal Care and Household

- 7.3.5 Other End-Users

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Amcor Group

- 8.1.2 Takemoto Yohki Co. Ltd.

- 8.1.3 Berry Global

- 8.1.4 Takigawa Corporation

- 8.1.5 Toyo Seiken Group Holdings Ltd.

- 8.1.6 Sonoco Products Company

- 8.1.7 Sealed Air Corporation

- 8.1.8 Hosokawa Yoko Co. ltd.

- 8.1.9 Toppan Inc.

- 8.1.10 Kodama Plastics Co. Ltd.

- 8.2 Heat Map Analysis

- 8.3 Competitor Analysis - Emerging vs. Established Players

9 INVESTMENT ANLAYSIS

10 FUTURE OF THE MARKET

北美塑膠包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

北美塑膠包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 2025 年軟塑膠包裝全球市場報告

2025 年軟塑膠包裝全球市場報告 聚丙烯瓦楞包裝市場規模、佔有率和成長分析(按包裝類型、分銷管道、最終用途和地區)- 產業預測 2025-2032

聚丙烯瓦楞包裝市場規模、佔有率和成長分析(按包裝類型、分銷管道、最終用途和地區)- 產業預測 2025-2032 軟塑膠包裝市場分析及預測至 2033 年:按類型、產品、材料類型、應用、技術、最終用戶、功能、形式和流程

軟塑膠包裝市場分析及預測至 2033 年:按類型、產品、材料類型、應用、技術、最終用戶、功能、形式和流程 一次性塑膠包裝:全球市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

一次性塑膠包裝:全球市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 中國塑膠包裝:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

中國塑膠包裝:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 中東和非洲的塑膠包裝:市場佔有率分析、產業趨勢和成長預測(2025-2030)

中東和非洲的塑膠包裝:市場佔有率分析、產業趨勢和成長預測(2025-2030) 亞太地區塑膠包裝:市場佔有率分析、產業趨勢和成長預測(2025-2030)

亞太地區塑膠包裝:市場佔有率分析、產業趨勢和成長預測(2025-2030) 印尼塑膠包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

印尼塑膠包裝:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 印度塑膠包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030)

印度塑膠包裝:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030)