|

市場調查報告書

商品編碼

1635455

日本容器玻璃:市場佔有率分析、產業趨勢、成長預測(2025-2030)Japan Container Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

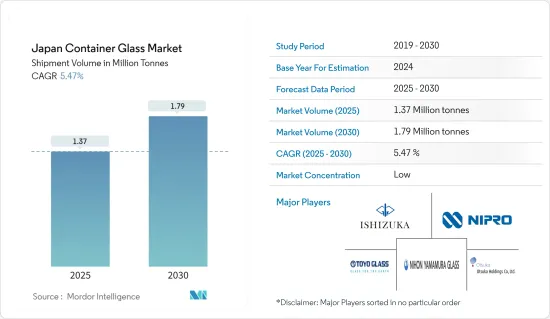

日本容器玻璃市場規模(以出貨量為準)預計將從2025年的137萬噸擴大到2030年的179萬噸,預測期間(2025-2030年)複合年成長率為5.47%。

主要亮點

- 由於玻璃容器無限的再生性使用性、可回收性、可再填充性以及各行業日益接受的推動,對玻璃容器的需求正在上升。這些優勢對於市場拓展發揮著重要的推動作用。

- 在日本,對更健康、更安全包裝的推動正在推動容器玻璃產業的成長。獨特的形狀、改進的美觀性和壓花等創新使包裝對消費者更具吸引力。此外,蓬勃發展的食品和飲料市場以及對生物分解性和環保產品不斷成長的需求進一步支持了玻璃包裝的成長。

- 在日本,玻璃瓶在飲料產業佔據主導地位。該行業擁有高效的瓶子回收系統。隨著對廢棄物和全球暖化的擔憂增加,對玻璃容器的需求持續增加。

- 根據美國農業部(USDA)統計,日本非酒精飲料市場價值約400億美元,其中進口額約10億美元。美國是日本非酒精飲料的主要供應國,主要出口礦泉水、胡蘿蔔汁和葡萄汁。這種湧入使得日本本土製造商有可能推出新的口味和類型,尤其是玻璃瓶裝的口味和類型,以應對不斷變化的消費者偏好,並保持與進口產品的競爭力,從而促進多元化。

- 日本兩個地球 (J2E) 研究著眼於透過人工智慧分類帶來的玻璃回收革命。這種人工智慧驅動的分類會隨著時間的推移而適應,透過準確分類玻璃顏色和類型來解決勞動力短缺問題並提高玻璃回收率。Ricoh集團旗下領先的掃描器製造商 PFU Corporation 推出了尖端的人工智慧工具。該工具採用影像識別技術,引導機械臂能夠區分棕色和不透明玻璃等顏色,每分鐘可分類 70 個瓶子。像弘前市的 Seinan Co., Ltd. 這樣的公司已經試行了這個人工智慧系統,以部分自動化玻璃瓶分類。

- 然而,玻璃生產是能源密集型的,並且在熔化過程中會從原料中排放二氧化碳。回收商務用玻璃容器面臨挑戰。日本玻璃產業正在積極採取措施減少玻璃對環境的影響,但這可能是抑制市場成長的因素。

日本容器玻璃市場的動向

醫藥產業大幅成長

- 日本是繼美國和中國之後的世界第三大醫藥市場。鑑於人口老化,日本政府正在加快創新藥物的核准流程並簡化生命科學法規。該策略旨在增強國內外製藥公司的實力,同時吸引新參與企業進入日本市場。世界經濟論壇強調了日本獨特的人口結構,指出日本超過10%的人口年齡超過80歲,使其成為世界上人口老化程度最高的國家。

- 據Adagos Pharma稱,截至2024年5月,日本市場的高估值證實了其巨大的潛力和醫療保健消費者的深度信任。美國著名製藥巨頭已在日本建立了強大的影響力,這證實了只要符合日本嚴格的品質標準,該市場就向外國公司開放。在政府的大力支持和充滿活力的研發環境下,生技藥品和專利藥物有望顯著成長。

- 日本製藥業實施嚴格的目視檢查、特殊包裝和細緻的標籤。材料和包裝技術的選擇不僅要符合當地法規,還要回應消費者的偏好。尤其是在人口老化的日本,易於使用、專為老年人設計的設計受到青睞。因此,以耐高溫且缺乏化學反應性而聞名的玻璃在日本的需求量很大。

- 透過消除全球投資障礙,日本政府正在刺激醫藥市場的擴張。隨著需求的增加,日本對玻璃容器的依賴預計將會增加。日本藥品批發商協會(JPWA)的資料顯示,日本倫理藥品市場中學名藥的銷售佔有率發生顯著變化,從 2020 年的 78.3% 上升至 2023 年的 80.2%。

- 各行業玻璃容器出貨量的激增進一步支持了市場擴張。玻璃容器優選用於包裝各種產品,包括易腐爛和不易腐爛的產品,以及液體藥品和化學品。此外,日本政府正在透過放鬆監管和鼓勵外國投資來促進這一成長。

飲料銷售推動市場成長

- 玻璃是包裝酒精飲料(尤其是烈酒)的首選材料。這種偏好是由該產品保持香氣和風味的獨特能力所驅動的。彩色玻璃瓶在葡萄酒包裝中尤其引人注目,在保護葡萄酒免受陽光照射方面發揮重要作用。隨著葡萄酒消費量持續增加,日本對玻璃容器和包裝的需求預計在預測期內也會增加。

- 日本酒精飲料部門在日本飲料製造領域佔有重要地位。據財務省稱,國內酒精飲料出口額將從2020年的710.3億日圓(6.7億美元)躍升至2023年的1,344.1億日圓(12.7億美元)。酒精飲料出口的激增將加強對國內玻璃容器的需求。

- 日本可口可樂公司在環保方面處於領先地位,取消了飲料上的塑膠標籤,並減少了自動販賣機的能源消費量。此舉符合可口可樂最近的全球承諾,到 2030 年使其 25% 的包裝可回收。可口可樂的策略重點是可重複使用的包裝,特別是可回收的玻璃瓶,這將加強玻璃容器的區域市場。

- 日本的一些城市支持玻璃瓶的回收和再利用,作為永續性舉措的一部分。例如,Circular Yokohama 是一個旨在振興橫濱市經濟的線上平台。橫濱可重複使用垃圾箱計劃由橫濱市資源回收商業合作社主導,專注於生產可重複使用的玻璃瓶。這項措施強調地產地銷,使環境和當地社區受益。

- 隨著消費者越來越重視便利性和隨身攜帶的選擇,包裝偏好也不斷改變。傳統上,由於玻璃瓶的重量和易碎性,玻璃瓶被認為不如塑膠和紙盒替代品方便,但現在它們越來越受歡迎。這種變化很大程度上歸功於輕質設計和防碎塗層等先進的包裝技術,使玻璃瓶對現代消費者更具吸引力。因此,飲料業預計玻璃瓶包裝將獲得更廣泛的接受,從而推動市場成長。

日本容器玻璃產業概況

日本容器玻璃市場較為分散,主要企業包括:東洋精工集團控股有限公司、日本山村硝子、日本精工硝子、石塚硝子等公司擁有重要的市場佔有率,並專注於透過合作和合併進行創新和業務擴張。

其他好處:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 容器玻璃進出口貿易資料

- 包裝用容器玻璃產業標準與法規

- 容器和包裝的永續性趨勢

- 日本容器用玻璃熔爐的容量和位置

第5章市場動態

- 市場促進因素

- 對環保和可重複使用產品的需求不斷成長

- 食品和飲料市場的需求不斷增加

- 市場限制

- 玻璃生產火熱且能源密集

- 日本在亞洲容器玻璃市場現況分析

- 貿易情景-日本容器玻璃產業進出口包裝的歷史與現狀分析

第6章 市場細分

- 按最終用戶產業

- 飲料

- 酒精飲料

- 葡萄酒和烈酒

- 啤酒/蘋果酒

- 其他酒精飲料

- 非酒精飲料

- 碳酸飲料

- 果汁

- 水

- 乳類飲料

- 調味飲料

- 其他非酒精飲料

- 食物

- 化妝品

- 藥品

- 其他最終用戶產業

- 飲料

第7章 競爭格局

- 公司簡介

- Toyo Seikan Group Holdings, Inc.

- Nihon Yamamura Glass Co. Ltd

- Japan Seiko Glass

- Otsuka Pharmaceutical Co., Ltd.

- KOA Glass Co., LTD

- Ishizuka Glass Co., Ltd.

- Nipro Corporation

- DAI-ICHI GLASS CO.,LTD

第8章補充通報-區域內主要容器玻璃廠主要窯爐供應商分析

第9章 市場未來展望

簡介目錄

Product Code: 91871

The Japan Container Glass Market size in terms of shipment volume is expected to grow from 1.37 million tonnes in 2025 to 1.79 million tonnes by 2030, at a CAGR of 5.47% during the forecast period (2025-2030).

Key Highlights

- Demand for glass containers is on the rise, driven by their endless reusability, recyclability, refillability, and growing acceptance across various industries. These benefits play a crucial role in fueling market expansion.

- In Japan, the push for healthier and safer packaging is driving the growth of the container glass industry. Innovations such as unique shapes, aesthetic enhancements, and embossing make packaging more attractive to consumers. Additionally, the booming food and beverage market, along with a rising demand for biodegradable and eco-friendly products, is further propelling the growth of glass packaging.

- In Japan, glass bottles dominate the beverage sector. The industry boasts efficient bottle recycling systems. As concerns about waste and global warming grow, the demand for glass containers continues to rise.

- As per the United States Department of Agriculture (USDA), Japan's non-alcoholic beverage market is valued at around USD 40 billion, with imports making up about USD 1 billion. The U.S. stands as the leading supplier of non-alcoholic beverages to Japan, with top exports being mineral water, carrot juice, and grape juice. This influx might encourage local Japanese producers to diversify their offerings, potentially introducing new flavors or types, especially those in glass bottles, to cater to changing consumer preferences and stay competitive against imports.

- Research by Japan 2 Earth (J2E) highlights a revolution in glass recycling through AI-powered sorting. This AI-driven sorting, which adapts over time, tackles labor shortages and enhances glass recycling rates by accurately categorizing glass by color and type. PFU Limited, a leading scanner manufacturer under the Ricoh Group, has introduced a cutting-edge AI tool. Leveraging image recognition technology, this tool guides robotic arms capable of sorting 70 bottles per minute, adept at distinguishing colors like brown or opaque glass. Companies like Hirosaki City's Seinan Corporation have piloted this AI system for partial automation of their glass bottle sorting.

- Nonetheless, glass production is energy-intensive, releasing CO2 from raw materials during melting. Recycling commercial glass containers poses challenges. The Japanese glass industry is actively working on initiatives to mitigate glass's environmental impact, a factor that could impede market growth.

Japan Container Glass Market Trends

Pharmaceutical Industry to Witness Significant Growth

- Japan ranks as the world's third-largest pharmaceutical market, following the United States and China. In light of its aging population, the Japanese government is expediting the approval process for innovative drugs and streamlining life science regulations. This strategy aims to strengthen both domestic and foreign pharmaceutical companies while attracting newcomers to Japan's market. The World Economic Forum highlights Japan's unique demographic, noting that over 10% of its population is aged 80 or older, making it home to the world's oldest populace.

- Adragos Pharma reports that as of May 2024, the market's lofty valuation underscores its immense potential and the deep trust it commands from healthcare consumers. Prominent U.S. pharmaceutical giants have cemented their presence in Japan, underscoring the market's openness to foreign entities, provided they meet Japan's rigorous quality benchmarks. With robust government support and a dynamic R&D landscape, biologics and patented drugs are set for substantial growth.

- Japan's pharmaceutical sector enforces rigorous visual inspections, specialized packaging, and meticulous labeling. The selection of materials and packaging technologies must not only comply with local regulations but also cater to consumer preferences. This is particularly crucial given the aging demographic in Japan, which favors user-friendly and senior-centric designs. As a result, glass, known for its ability to withstand high temperatures and chemical non-reactivity, sees heightened demand in the nation.

- By removing barriers to global investment, the Japanese government is fueling the expansion of its pharmaceutical market. With rising demand, Japan foresees an increased reliance on glass containers. Data from The Federation of Japan Pharmaceutical Wholesalers Association (JPWA) reveals a notable shift: the volume share of generics in Japan's prescription drug market climbed from 78.3% in 2020 to 80.2% in 2023.

- The market's expansion is further supported by a surge in glass container shipments across diverse sectors. Glass containers are preferred for packaging not only liquid pharmaceuticals and chemicals but also a wide array of perishable and non-perishable goods. Moreover, the Japanese government is nurturing this growth by relaxing regulations and promoting foreign investments.

Beverage Sales to Drive the Market Growth

- Glass stands out as the preferred material for packaging alcoholic beverages, especially spirits. Its distinct capability to maintain product aromas and flavors drives this preference. Tinted glass bottles, especially prominent in wine packaging, play a crucial role in shielding wine from sunlight. As wine consumption continues to rise, so too will the demand for glass packaging in the country during the forecast period.

- Japan's alcoholic beverage sector holds a significant position in the nation's beverage manufacturing arena. According to the Ministry of Finance Japan, exports of domestic alcoholic beverages jumped from JPY 71.03 billion (USD 670 million) in 2020 to JPY 134.41 billion (USD 1.27 billion) in 2023. This surge in alcoholic drink exports is poised to bolster the demand for glass containers domestically.

- Coca-Cola Japan is leading the charge in eco-friendliness, removing plastic labels from its beverages and cutting down energy consumption in its vending machines. This move is in line with Coca-Cola's recent global commitment to make 25% of its packaging recyclable by 2030. Their strategy emphasizes reusable packaging, especially returnable glass bottles, which is set to enhance the regional market for glass containers.

- Several cities in Japan are championing the recycling and reuse of glass bottles as part of their sustainability initiatives. For example, Circular Yokohama is an online platform aimed at boosting Yokohama city's economy. The Yokohama reuse bin project, spearheaded by the Yokohama City Resource Recycling Business Cooperative, focuses on creating reusable glass bottles. This initiative emphasizes local production and consumption, benefiting both the environment and the community.

- As consumers increasingly prioritize convenience and on-the-go options, packaging preferences are evolving. While glass bottles have traditionally been viewed as less convenient due to their weight and fragility compared to plastic or carton alternatives, they are now gaining popularity. This shift is largely due to advancements in packaging technology, such as lightweight designs and shatter-resistant coatings, making glass bottles more appealing to modern consumers. Consequently, the beverage sector is expected to embrace glass bottle packaging more widely, driving market growth.

Japan Container Glass Industry Overview

The Japan Glass Container Market is moderately fragmented, with key players such as Toyo Seikan Group Holdings, Inc., Nihon Yamamura Glass Co. Ltd, Japan Seiko Glass, Ishizuka Glass Co., Ltd., and more. These players have a significant market share and are focused on innovations and business expansion through collaboration and mergers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Import Export Trade Data of Container Glass

- 4.3 Industry Standards and Regulations for Container Glass Use for Packaging

- 4.4 Sustainability Trends for Packaging

- 4.5 Container Glass Furnace Capacity and Location in Japan

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand for Environmentally Friendly and Reusable Products

- 5.1.2 Increased Demand in the Food and Beverage Market

- 5.2 Market Restrain

- 5.2.1 Glass Production is Energy Intensive with High Temperatures for Manufacturing

- 5.3 Analysis of the Current Positioning of Japan in the Asian Container Glass Market

- 5.4 Trade Scenario - Analysis of the Historical and Current Export-Import Packaging for Container Glass Industry in Japan

6 MARKET SEGMENTATION

- 6.1 End-User Industry

- 6.1.1 Beverages

- 6.1.1.1 Alcoholic Beverages

- 6.1.1.1.1 Wines and Spirits

- 6.1.1.1.2 Beer and Cider

- 6.1.1.1.3 Other Alcoholic-Beverages

- 6.1.1.2 Non-Alcoholic Beverages

- 6.1.1.2.1 Carbonated Drinks

- 6.1.1.2.2 Juices

- 6.1.1.2.3 Water

- 6.1.1.2.4 Dairy-Based

- 6.1.1.2.5 Flavored Drinks

- 6.1.1.2.6 Other Non-Alcoholic Beverages

- 6.1.2 Food

- 6.1.3 Cosmetics

- 6.1.4 Pharmaceuticals

- 6.1.5 Other End-user Industries

- 6.1.1 Beverages

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Toyo Seikan Group Holdings, Inc.

- 7.1.2 Nihon Yamamura Glass Co. Ltd

- 7.1.3 Japan Seiko Glass

- 7.1.4 Otsuka Pharmaceutical Co., Ltd.

- 7.1.5 KOA Glass Co., LTD

- 7.1.6 Ishizuka Glass Co., Ltd.

- 7.1.7 Nipro Corporation

- 7.1.8 DAI-ICHI GLASS CO.,LTD

8 SUPPLEMENTARY COVERAGE - ANALYSIS OF MAJOR FURNACE SUPPLIERS TO MAJOR CONTAINER GLASS PLANTS IN THE REGION**

9 FUTURE OUTLOOK OF THE MARKET

02-2729-4219

+886-2-2729-4219

2025-2029年全球玻璃瓶與容器市場

2025-2029年全球玻璃瓶與容器市場 容器玻璃市場規模、佔有率、成長分析,按產品類型、按材料、按產能、按玻璃類型、按成型製程、按地區 - 產業預測,2025 年至 2032 年

容器玻璃市場規模、佔有率、成長分析,按產品類型、按材料、按產能、按玻璃類型、按成型製程、按地區 - 產業預測,2025 年至 2032 年 2025 年全球容器玻璃市場報告保溫瓶市場規模、佔有率和成長分析(按類型、材料、應用、分銷管道和地區)- 2025-2032 年產業預測

2025 年全球容器玻璃市場報告保溫瓶市場規模、佔有率和成長分析(按類型、材料、應用、分銷管道和地區)- 2025-2032 年產業預測 中東和非洲玻璃瓶和容器市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030)亞太地區玻璃瓶和容器:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)北美玻璃瓶/容器:市場佔有率分析、行業趨勢和成長預測(2025-2030)印度容器玻璃:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)拉丁美洲玻璃瓶和容器:市場佔有率分析、行業趨勢和成長預測(2025-2030)歐洲玻璃瓶和容器:市場佔有率分析、行業趨勢和成長預測(2025-2030)

中東和非洲玻璃瓶和容器市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030)亞太地區玻璃瓶和容器:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)北美玻璃瓶/容器:市場佔有率分析、行業趨勢和成長預測(2025-2030)印度容器玻璃:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)拉丁美洲玻璃瓶和容器:市場佔有率分析、行業趨勢和成長預測(2025-2030)歐洲玻璃瓶和容器:市場佔有率分析、行業趨勢和成長預測(2025-2030)

▼