|

市場調查報告書

商品編碼

1636180

全球電動車鋰離子電池隔離膜市場:市場佔有率分析、產業趨勢與成長預測(2025-2030)Global Lithium-ion Battery Separator For Electric Vehicle Application - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

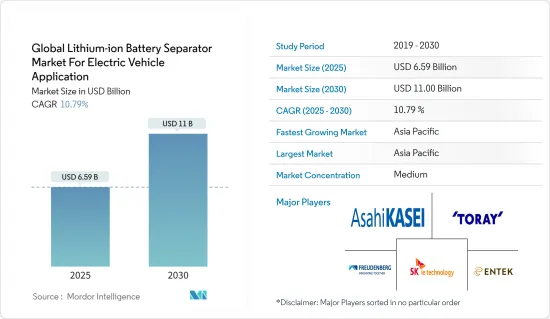

全球電動車鋰離子電池隔膜市場預計將從2025年的65.9億美元成長到2030年的110億美元,預測期間(2025-2030年)複合年成長率為10.79%。

主要亮點

- 從中期來看,電動車銷量增加和鋰離子電池成本下降等因素預計將成為預測期內全球電動車鋰離子電池隔膜市場的最大推動力之一。

- 另一方面,電池隔膜製造面臨複雜的供應鏈限制,在預測期內對電動車應用的全球鋰離子電池隔離膜市場構成威脅。

- 人們不斷努力開發增強型電池隔膜材料。預計這一因素未來將為全球電動車鋰離子電池隔膜市場創造多個機會。

- 預計亞太地區將出現強勁成長,並可能在預測期內實現最高的複合年成長率。這是因為該地區擁有大規模的電池及相關設備和材料製造業。

鋰離子電池隔離膜的全球趨勢

聚乙烯推動成長

- 聚乙烯(PE)已成為電動車應用鋰離子電池隔膜的關鍵材料。主要原因是其優異的化學穩定性、機械強度和生產薄多孔膜的能力。由於電動車行業的快速擴張以及對高性能、安全和具有成本效益的能源儲存解決方案的需求不斷增加,近年來電動車電池中聚乙烯隔膜的全球市場經歷了顯著成長。

- 聚乙烯隔膜,特別是高密度聚苯乙烯(HDPE) 和超高分子量聚乙烯 (UHMWPE) 隔膜,具有多種特性,使其適合在電動汽車電池的惡劣環境中使用。這些材料對鋰離子電池中使用的電解和電極材料表現出優異的耐化學性,同時提供熱穩定性,這對於防止電池系統的熱失控至關重要。

- 隨著全球電動車需求的擴大,電動車電池的需求將快速增加,導致聚乙烯作為電池隔膜材料的需求增加。這種需求的成長是由電動和混合動力汽車的,這些汽車需要高效、耐用的電池組件。此外,電池技術的進步進一步推動了對高品質聚乙烯隔膜的需求。

- 據獎勵總署(IEA) 稱,由於大眾採用永續交通解決方案的意識不斷增強以及地方政府對脫碳目標的承諾,近年來電動車銷量大幅成長。 2023年至2022年,電動車銷量將成長30.13%,2019年至2023年年平均成長超過100%。

- 在最近的趨勢中,製造商正在採用最新的製造技術,開發新的材料成分,並與其他材料一起開發新的材料化學。這些進步不僅提高了聚乙烯隔膜的功能特性,而且還有助於降低製造成本,使得聚乙烯隔膜越來越受到想要最佳化電池性能同時控制生產成本的電動車製造商的歡迎。

- 例如,2024年1月,近代物理研究所(IMP)和廣東省先進能源科學與技術實驗室的科學家開發了一種用於鋰離子電池的耐高溫聚對苯二甲酸乙二醇酯(PET)隔膜。隔膜作為鋰離子電池的關鍵部件,對於確保電池安全起著重要作用。它不僅使正負極絕緣,防止短路,還能促進鋰離子的傳輸。

- 因此,鑑於以上幾點,預計聚乙烯隔膜材料在預測期內將會成長。

亞太地區主導市場

- 亞太地區在全球電動車鋰離子電池隔膜市場中佔據主導地位,其影響力遠遠超出其地理界限。這項優勢源自於多種因素,包括該地區強大的製造能力、政府的大力支持、廣泛的研發舉措以及整個電動車供應鏈中關鍵參與企業的存在。

- 中國、日本、韓國以及最近的印度等國家正在利用其在電子、汽車製造和先進材料方面的現有優勢,為電池隔膜製造建立強大的生態系統,並成為這個快速發展行業的領跑者。該地區在這一市場的快速成長不僅歸功於其製造能力,還源於其認知到電動車將在未來全球交通中發揮關鍵作用的戰略遠見。

- 例如,國際能源總署(IEA)近年來電動車銷量顯著成長。 2022年至2022年,電動車銷量成長速度將超過24%,2019年至2023年,複合年成長率將接近100%。這意味著電動車正在獲得牽引力,從而為鋰離子電池隔膜市場帶來有利的市場環境。

- 這種認可導致了在產能擴張、技術創新以及培養專門從事電池和隔膜技術的熟練勞動力方面的大量投資。這種獨特的因素組合使亞太地區成為目前電動車鋰離子電池隔膜生產的領導者。隨著其他地區尋求發展這一重要技術領域的能力,亞太地區有能力在未來保持這一領先地位。

- 例如,旭化成公司計劃於2023年10月進行新的資本投資,以提高高孔鋰離子電池(LIB)隔膜的產能。該公司計劃在目前位於美國、日本和韓國的鋰離子電池隔膜工廠安裝新的塗層生產線。預計從 2026 年上半年開始分階段營運。這項策略性舉措將使旭化成能夠滿足約 170 萬輛電動車的電池需求。

- 旭化成公司的最新投資凸顯了其致力於推進電池技術以滿足電動車不斷成長的需求的承諾。旭化成公司旨在透過提高產能來鞏固其在全球鋰離子市場的地位。新的塗裝線將配備最新技術,以確保高品質和高效的生產過程。此次擴張符合旭化成支持向永續能源解決方案過渡的長期策略。

- 因此,如上所述,亞太地區預計將在預測期內主導市場。

全球鋰離子電池隔膜產業概況

全球電動車鋰離子電池隔膜市場呈現半截結構。該市場的主要企業(排名不分先後)包括旭化成公司、東麗電池隔膜、Freudenberg Performance Materials、SKie Technology Corporation Ltd 和 Entek International。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2029年之前的市場規模與需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規和措施

- 市場動態

- 促進因素

- 電動車銷量成長

- 鋰離子電池價格下降

- 抑制因素

- 供應鏈限制

- 促進因素

- 供應鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品/服務的威脅

- 競爭公司之間的敵對關係

- 投資分析

第5章市場區隔

- 材料

- 聚乙烯

- 聚丙烯

- 複合材料

- 其他

- 2029 年之前的市場規模和需求預測(按地區)

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 北歐的

- 俄羅斯

- 土耳其

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 澳洲

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 中東/非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 奈及利亞

- 埃及

- 卡達

- 南非

- 其他中東/非洲

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 北美洲

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略及SWOT分析

- 公司簡介

- Asahi Kasei Corporation

- Toray Battery Separator Film Co. Ltd

- Freudenberg Performance Materials

- SK ie Technology Corporation Ltd

- Entek International

- Sumitomo Chemical Co. Ltd

- Ube Maxell Co. Ltd

- W-Scope Corporation

- Daramic

- Amer SIL

- 其他知名公司名單

- 市場排名/佔有率(%)分析

第7章 市場機會及未來趨勢

- 強化隔膜材料的開發

The Global Lithium-ion Battery Separator Market For Electric Vehicle Application Industry is expected to grow from USD 6.59 billion in 2025 to USD 11.00 billion by 2030, at a CAGR of 10.79% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as rising growth in electric vehicle sales and declining cost of lithium-ion batteries are expected to be among the most significant drivers for the global lithium-ion battery separator market for electric vehicle applications during the forecast period.

- On the other hand, there are complex supply chain constraints for manufacturing battery separators that pose a threat to the global lithium-ion battery separator market for electric vehicle applications during the forecast period.

- Nevertheless, continued efforts are being made to develop enhanced battery separator materials. This factor is expected to create several opportunities for the global lithium-ion battery separator market for electric vehicle applications in the future.

- The Asia-Pacific region is expected to witness significant growth and is likely to register the highest CAGR during the forecast period. This is due to the presence of a significant battery and associated equipment and materials manufacturing industry in the region.

Global Lithium-ion Battery Separator Market Trends

Polyethylene to Witness Growth

- Polyethylene (PE) has emerged as a dominant material for lithium-ion battery separators in electric vehicle applications. This is mainly due to its excellent chemical stability, mechanical strength, and ability to be manufactured into thin, porous membranes. The global market for Polyethylene separators in electric vehicle batteries has seen substantial growth in recent years, driven by the rapid expansion of the electric vehicle industry and increasing demand for high-performance, safe, and cost-effective energy storage solutions.

- Polyethylene separators, particularly those made from high-density polyethylene (HDPE) and ultra-high molecular weight polyethylene (UHMWPE), offer a compelling combination of properties that make them well-suited for use in the demanding environment of electric vehicle batteries. These materials provide good thermal stability, which is crucial for preventing thermal runaway in battery systems, while also offering excellent chemical resistance to the electrolytes and electrode materials used in lithium-ion cells.

- As global electric vehicle demand escalates, the demand for batteries in electric vehicle applications is set to surge, consequently boosting the need for polyethylene in battery separator materials. This increase is driven by the growing production of electric and hybrid vehicles, which require efficient and durable battery components. Additionally, advancements in battery technology are further propelling the demand for high-quality polyethylene separators.

- According to the International Energy Agency (IEA), electric vehicle sales have witnessed a significant surge in recent years owing to the growing awareness of adopting sustainable transportation solutions amongst the public and various financial incentives offered by regional governments to meet their decarbonization targets. Between 2023 and 2022, electric vehicle sales witnessed an uptick of 30.13%, whereas the annual average growth rate between 2019 and 2023 was over 100%, signifying the growing traction for electric vehicles.

- In recent years, manufacturers have adopted the latest manufacturing techniques, developed new material compositions, and developed new material chemistries with other materials. These advancements have not only improved the functional properties of Polyethylene separators but have also contributed to reducing manufacturing costs, making them an increasingly attractive option for electric vehicle manufacturers looking to optimize battery performance while managing production expenses.

- For instance, in January 2024, Scientists at the Institute of Modern Physics (IMP) of the Chinese Academy of Sciences (CAS) and the Advanced Energy Science and Technology Guangdong Laboratory have developed high-temperature-resistant polyethylene terephthalate (PET) separators for lithium-ion batteries. The separator, a pivotal component of lithium-ion batteries, is instrumental in safeguarding battery safety. It not only insulates the cathode and anode to prevent short-circuiting but also facilitates the transport of lithium ions.

- Therefore, as per the points mentioned above, the polyethylene separator material is expected to witness growth during the forecast period.

Asia Pacific to Dominate the Market

- The Asia-Pacific region has emerged as the dominant force in the global lithium-ion battery separator market for electric vehicle applications, with its influence extending far beyond its geographical boundaries. This dominance is rooted in a variety of factors, including the region's robust manufacturing capabilities, significant government support, extensive research and development initiatives, and the presence of major players across the entire electric vehicle supply chain.

- Countries like China, Japan, South Korea, and, to a growing extent, India have positioned themselves at the forefront of this rapidly evolving industry, leveraging their existing strengths in electronics, automotive manufacturing, and advanced materials to create a formidable ecosystem for battery separator production. The region's rapid growth in this market is not only a result of its manufacturing prowess but also stems from its strategic foresight in recognizing the pivotal role that electric vehicles will play in the future of global transportation.

- For instance, the International Energy Agency has witnessed significant growth in electric vehicle sales in recent years. Between 2022 and 2022, the growth in electric vehicle sales increased by more than 24%, whereas between 2019 and 2023, the annual average growth rate was close to 100%. This signifies the growing traction for electric vehicles, which in turn developed favorable market conditions for the lithium-ion battery separator market.

- This recognition has led to substantial investments in capacity expansion, technological innovation, and the development of a highly skilled workforce specializing in battery and separator technologies. This unique combination of factors has established the Asia-Pacific as the current leader in lithium-ion battery separator production for electric vehicles. Still, it has also positioned itself to maintain this leadership well into the future, even as other regions seek to develop their capabilities in this critical technology sector.

- For instance, in October 2023, Asahi Kasei is set to invest in new equipment to bolster its production capacity for Hipore lithium-ion battery (LIB) separators. The company plans to set up fresh coating lines at its current LIB separator plants in the United States, Japan, and South Korea. Operations are slated to commence in stages, starting in the first half of fiscal year 2026. This strategic move will enable Asahi Kasei to cater to the battery needs of approximately 1.7 million electric vehicles.

- Asahi Kasei's investment underscores its commitment to advancing battery technology and meeting the growing demand for electric vehicles. By enhancing its production capabilities, the company aims to strengthen its position in the global lithium-ion market. The new coating lines will incorporate state-of-the-art technology to ensure high-quality and efficient production processes. This expansion aligns with Asahi Kasei's long-term strategy to support the transition to sustainable energy solutions.

- Therefore, as mentioned above, the Asia-Pacific region is expected to dominate the market during the forecast period.

Global Lithium-ion Battery Separator Industry Overview

The global lithium-ion battery separator market for electric vehicle applications is semi-fragmented. Some of the key players in this market (in no particular order) are Asahi Kasei Corporation, Toray Battery Separator Film Co. Ltd, Freudenberg Performance Materials, SK ie Technology Corporation Ltd, and Entek International.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Electric Vehicle Sales

- 4.5.1.2 Decreasing Lithium-ion Battery Price

- 4.5.2 Restraints

- 4.5.2.1 Supply Chain Constraints

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Material

- 5.1.1 Polyethylene

- 5.1.2 Polypropylene

- 5.1.3 Composite

- 5.1.4 Other Materials

- 5.2 Geography [Market Size and Demand Forecast till 2029 (for regions only)]

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 France

- 5.2.2.3 United Kingdom

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 NORDIC

- 5.2.2.7 Russia

- 5.2.2.8 Turkey

- 5.2.2.9 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Australia

- 5.2.3.4 Japan

- 5.2.3.5 South Korea

- 5.2.3.6 Malaysia

- 5.2.3.7 Thailand

- 5.2.3.8 Indonesia

- 5.2.3.9 Vietnam

- 5.2.3.10 Rest of Asia-Pacific

- 5.2.4 Middle East and Africa

- 5.2.4.1 Saudi Arabia

- 5.2.4.2 United Arab Emirates

- 5.2.4.3 Nigeria

- 5.2.4.4 Egypt

- 5.2.4.5 Qatar

- 5.2.4.6 South Africa

- 5.2.4.7 Rest of Middle East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Colombia

- 5.2.5.4 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted & SWOT Analysis for Leading Players

- 6.3 Company Profiles

- 6.3.1 Asahi Kasei Corporation

- 6.3.2 Toray Battery Separator Film Co. Ltd

- 6.3.3 Freudenberg Performance Materials

- 6.3.4 SK ie Technology Corporation Ltd

- 6.3.5 Entek International

- 6.3.6 Sumitomo Chemical Co. Ltd

- 6.3.7 Ube Maxell Co. Ltd

- 6.3.8 W-Scope Corporation

- 6.3.9 Daramic

- 6.3.10 Amer SIL

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Enhanced Separator Materials

2025 年至 2033 年鋰離子電池隔膜市場報告,按材料(聚丙烯 (PP)、聚乙烯 (PE)、尼龍等)、厚度(16µm、20µm、25µm)、最終用戶(工業、消費電子、汽車等)和地區分類

2025 年至 2033 年鋰離子電池隔膜市場報告,按材料(聚丙烯 (PP)、聚乙烯 (PE)、尼龍等)、厚度(16µm、20µm、25µm)、最終用戶(工業、消費電子、汽車等)和地區分類 電池隔膜市場,按電池、隔膜、材料、技術、應用、國家和地區分類 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

電池隔膜市場,按電池、隔膜、材料、技術、應用、國家和地區分類 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測 2025 年電池隔膜全球市場報告

2025 年電池隔膜全球市場報告 SLI用鉛酸電池隔離膜的全球市場:市場佔有率分析、產業趨勢與成長預測(2025-2030年)

SLI用鉛酸電池隔離膜的全球市場:市場佔有率分析、產業趨勢與成長預測(2025-2030年) 中國電動汽車電池隔膜:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

中國電動汽車電池隔膜:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 中東和非洲電動車電池分離器市場佔有率分析、產業趨勢、統計和成長預測(2025-2030)

中東和非洲電動車電池分離器市場佔有率分析、產業趨勢、統計和成長預測(2025-2030) 亞太地區電動汽車電池分離器:市場佔有率分析、產業趨勢與成長預測(2025-2030)

亞太地區電動汽車電池分離器:市場佔有率分析、產業趨勢與成長預測(2025-2030) 北美電動車電池分離器:市場佔有率分析、產業趨勢、成長預測(2025-2030)

北美電動車電池分離器:市場佔有率分析、產業趨勢、成長預測(2025-2030) 南美洲電動車電池分離器:市場佔有率分析、產業趨勢與成長預測(2025-2030)

南美洲電動車電池分離器:市場佔有率分析、產業趨勢與成長預測(2025-2030) 印度電動車電池分離器:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

印度電動車電池分離器:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)