|

市場調查報告書

商品編碼

1636181

SLI用鉛酸電池隔離膜的全球市場:市場佔有率分析、產業趨勢與成長預測(2025-2030年)Global Lead-Acid Battery Separator For SLI Applications - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

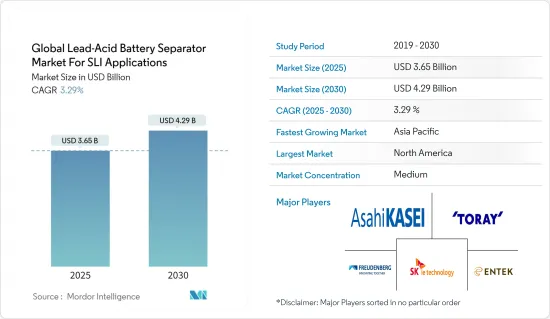

用於 SLI 應用的鉛酸電池隔膜的全球市場預計將從 2025 年的 36.5 億美元成長到 2030 年的 42.9 億美元,預測期內(2025-2030 年)複合年成長率為 3.29%。

主要亮點

- 從中期來看,自動化領域成長率的上升和鉛酸電池的成本效益等因素預計將成為預測期內SLI應用的鉛酸電池隔膜全球市場的最大驅動力之一。

- 同時,電池隔膜製造的複雜供應鏈限制威脅著預測期內的市場研究。

- 人們不斷努力開發增強型電池隔膜材料。由於這個因素,全球鉛酸電池隔膜市場預計未來將為SLI應用創造多個機會。

- 預計亞太地區將出現強勁成長,並可能在預測期內實現最高的複合年成長率。這是因為該地區電池及相關設備和材料的製造業規模較大。

全球鉛酸電池隔離膜市場趨勢

聚丙烯細分市場實現顯著成長

- 聚丙烯最近已成為全球鉛酸電池隔膜市場不可或缺的一部分,特別是在啟動、照明和點火 (SLI) 應用領域。這種多功能熱塑性聚合物具有優異的性能,包括優異的耐化學性、高機械強度和良好的電絕緣性。

- 聚丙烯的多功能性允許添加各種添加劑和表面處理,以增強其性能特徵並延長電池壽命。這種適應性使聚丙烯成為尋求提高產品效率和耐用性的電池製造商的有吸引力的選擇。隨著汽車產業面臨生產更有效率、更環保車輛的壓力,對高性能 SLI 電池的需求不斷成長,進一步鞏固了聚丙烯在隔膜市場的地位。

- 隨著全球汽車產量的增加,SLI應用的電池需求迅速增加,對聚丙烯作為電池隔膜材料的需求也不斷增加。這是由於電動和混合動力汽車的產量不斷增加,需要高效、耐用的電池組件。此外,電池技術的進步進一步推動了對高品質聚丙烯隔膜的需求。

- 根據國際汽車工業協會的數據,全球汽車產量已超過疫情前的水準。預計未來還將繼續保持同樣的成長趨勢。例如,2019年至2023年,年產能增幅超過2%,2022年至2023年,成長超過10%,顯示汽車產量正在擴張。

- 持續的研究和開發重點是改進聚丙烯隔膜技術。目前正在進行研究以增強聚丙烯隔膜已經令人印象深刻的能力,包括開發奈米複合材料和先進的表面改質。這些創新旨在提高電池性能、壽命和安全性,以滿足汽車產業和其他依賴鉛酸電池技術的領域不斷變化的需求。

- 例如,2024年2月,仁川大學的科學家開創了一種提高電池隔膜穩定性和性能的方法。此方法是塗上一層二氧化矽和其他特殊分子。這項研究結果發表在《能源儲存材料》雜誌上,證明了聚丙烯(PP)隔膜的有效接枝聚合可以引入一致的二氧化矽(SiO2)層。

- 因此,鑑於上述情況,聚丙烯隔膜材料領域預計在預測期內將成長。

亞太地區主導市場

- 亞太地區主導全球鉛酸電池隔離膜市場,特別是在 SLI 應用的聚丙烯領域。這一成長的關鍵因素是該地區蓬勃發展的汽車工業、快速工業化以及日益成長的能源儲存需求。

- 根據國際汽車工業組織預測,2022年至2023年亞太地區汽車產量將大幅成長。 2023年,該地區生產汽車55,115,837輛,恢復10%的成長速度。 2019年至2023年的複合年成長率超過12%,顯示該地區對齒輪的需求不斷增加。

- 中國、日本、韓國和印度處於這一市場擴張的前沿。這些國家強大的製造業和不斷成長的國內汽車需求對聚丙烯電池隔膜的採用做出了重大貢獻。

- 尤其是中國,在塑造該地區的市場動態方面發揮關鍵作用。中國作為全球最大的汽車市場和鉛酸電池的重要生產國,近年來對高品質聚丙烯隔膜的需求激增。中國對電動車和混合動力技術的推動反而增強了其 SLI 電池市場。

- 日本和韓國以其技術力實力而聞名,引領了聚丙烯隔膜製造的創新。這些國家的公司致力於開發具有增強性能的隔膜材料,例如提高抗穿刺性和降低電阻。這些進展不僅為國內市場做出了貢獻,而且對向區域內外國家出口高品質隔膜發揮了重要作用。

- 例如,2024年1月,韓國仁川大學的科學家開發了一項可提高隔膜穩定性和性能的技術。透過結合二氧化矽層和其他特殊分子,使用這種隔膜的電池提高了性能並抑制了侵入性根狀結構的生長。這項突破將促進更安全電池的開發,這對於電動車和尖端能源儲存解決方案的廣泛使用至關重要。

- 因此,如前所述,亞太地區預計將在預測期內主導市場。

全球鉛酸蓄電池隔膜產業概況

SLI 應用的全球鉛酸電池隔離膜市場處於半斷開狀態。該市場的主要企業(排名不分先後)包括旭化成公司、東麗電池隔膜、Freudenberg Performance Materials、SKie Technology Corporation Ltd 和 Entek International。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2029年之前的市場規模與需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規和措施

- 市場動態

- 促進因素

- 汽車工業的成長

- 成本效益

- 抑制因素

- 供應鏈限制

- 促進因素

- 供應鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品/服務的威脅

- 競爭公司之間的敵對關係

- 投資分析

第5章市場區隔

- 材料

- 聚乙烯

- 聚丙烯

- 其他

- 2029 年之前的市場規模和需求預測(按地區)

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 北歐的

- 俄羅斯

- 土耳其

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 澳洲

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

- 中東/非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 奈及利亞

- 埃及

- 卡達

- 南非

- 其他中東/非洲

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 南美洲其他地區

- 北美洲

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略及SWOT分析

- 公司簡介

- Asahi Kasei Corporation

- Toray Battery Separator Film Co. Ltd

- Freudenberg Performance Materials

- SK ie Technology Corporation Ltd

- Entek International

- Sumitomo Chemical Co. Ltd

- Ube Maxell Co. Ltd

- W-Scope Corporation

- Daramic

- Amer SIL

- 其他知名公司名單

- 市場排名/佔有率(%)分析

第7章 市場機會及未來趨勢

- 強化隔膜材料的開發

The Global Lead-Acid Battery Separator Market For SLI Applications Industry is expected to grow from USD 3.65 billion in 2025 to USD 4.29 billion by 2030, at a CAGR of 3.29% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as rising growth in the automation sector and the cost-effectiveness of lead-acid batteries are expected to be among the most significant drivers for the global lead-acid battery separator market for SLI applications during the forecast period.

- On the other hand, complex supply chain constraints for manufacturing battery separators threaten the market studied during the forecast period.

- Nevertheless, continued efforts are being made to develop enhanced battery separator materials. This factor is expected to create several opportunities for SLI applications in the global lead-acid battery separator market in the future.

- Asia-Pacific is expected to witness significant growth and will likely register the highest CAGR during the forecast period. This is due to the region's considerable battery and associated equipment and materials manufacturing industry.

Global Lead-Acid Battery Separator Market Trends

Polypropylene Segment to Witness Significant Growth

- Polypropylene has become essential in the global lead-acid battery separator market, especially for Starting, Lighting, and Ignition (SLI) applications in recent years. This versatile thermoplastic polymer offers optimal properties, including excellent chemical resistance, high mechanical strength, and good electrical insulation.

- Polypropylene's versatility allows for incorporating various additives and surface treatments, enhancing its performance characteristics and extending battery life. This adaptability has made it an attractive option for battery manufacturers looking to improve their products' efficiency and durability. As the automotive industry faces increasing pressure to produce more efficient and environmentally friendly vehicles, the demand for high-performance SLI batteries has grown, further solidifying polypropylene's position in the separator market.

- As global automobile manufacturing escalates, the demand for batteries in SLI applications is set to surge, consequently boosting the need for polypropylene in battery separator materials. This increase is driven by the growing production of electric and hybrid vehicles requiring efficient and durable battery components. Additionally, advancements in battery technology are further propelling the demand for high-quality polypropylene separators.

- According to the International Organization of Motor Vehicle Manufacturers, global automobile manufacturing has surpassed the pre-pandemic level. It is expected to continue on a similar growth trend in the coming years. For instance, between 2019 and 2023, the annual production capacity increased by more than 2%, whereas the growth rate between 2022 and 2023 was over 10%, signifying the growing production of automobiles.

- Ongoing research and development efforts are focused on improving polypropylene separator technology. Areas of exploration include developing nanocomposite materials and advanced surface modifications to enhance polypropylene separators' already impressive capabilities. These innovations aim to improve battery performance, longevity, and safety, meeting the evolving needs of the automotive industry and other sectors reliant on lead-acid battery technology.

- For instance, in February 2024, Scientists at Incheon National University pioneered a method to enhance battery separators' stability and properties. Their approach involves applying a layer of silicon dioxide and other specialized molecules. The findings, detailed in a publication in Energy Storage Materials, showcase the effective graft polymerization on a polypropylene (PP) separator, introducing a consistent layer of silicon dioxide (SiO2).

- Therefore, as per the above points, the polypropylene separator material segment is expected to grow during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific region has emerged as a dominant force in the global lead-acid battery separator market, particularly in the polypropylene segment for SLI applications. This growth is primarily driven by the region's booming automotive industry, rapid industrialization, and increasing energy storage needs.

- According to the International Organization of Motor Vehicle Manufacturers, automobile manufacturing in Asia-Pacific significantly rose between 2022 and 2023. In 2023, the region manufactured 55,115,837 automobiles, resuming a 10% growth rate. The annual average growth rate between 2019 and 2023 was over 12%, signifying the rising demand for gears in the region.

- China, Japan, South Korea, and India are at the forefront of this market expansion. Their robust manufacturing sectors and growing domestic vehicle demand contribute significantly to the uptake of polypropylene battery separators.

- China, in particular, plays a crucial role in shaping the regional market dynamics. As the world's largest automobile market and a significant producer of lead-acid batteries, China's demand for high-quality polypropylene separators has surged in recent years. The country's push toward electric vehicles and hybrid technologies has paradoxically bolstered the SLI battery market, as these vehicles still require traditional lead-acid batteries for their 12V systems.

- Japan and South Korea, known for their technological prowess, have driven innovations in polypropylene separator manufacturing. Companies in these countries have focused on developing separator materials with enhanced performance characteristics, such as improved puncture resistance and reduced electrical resistance. These advancements have served their domestic markets and positioned them as key exporters of high-quality separators to other countries in the region and beyond.

- For instance, in January 2024, Incheon National University scientists in South Korea pioneered a technique to enhance separator stability and characteristics. By incorporating a layer of silicon dioxide and other specialized molecules, batteries utilizing these separators showcased enhanced performance and curbed the growth of intrusive root-like structures. This breakthrough sets the stage for developing high-safety batteries, which are crucial for the widespread acceptance of electric vehicles and cutting-edge energy storage solutions.

- Therefore, as mentioned above, the Asia-Pacific region is expected to dominate the market during the forecast period.

Global Lead-Acid Battery Separator Industry Overview

The global lead-acid battery separator market for SLI applications is semi-fragmented. Some key players in this market (in no particular order) are Asahi Kasei Corporation, Toray Battery Separator Film Co. Ltd, Freudenberg Performance Materials, SK ie Technology Corporation Ltd, and Entek International.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growth in Automotive Industry

- 4.5.1.2 Cost Effectiveness

- 4.5.2 Restraints

- 4.5.2.1 Supply Chain Constraints

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Material

- 5.1.1 Polyethylene

- 5.1.2 Polypropylene

- 5.1.3 Others

- 5.2 Geography [Market Size and Demand Forecast till 2029 (for regions only)]

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 France

- 5.2.2.3 United Kingdom

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 NORDIC

- 5.2.2.7 Russia

- 5.2.2.8 Turkey

- 5.2.2.9 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Australia

- 5.2.3.4 Japan

- 5.2.3.5 South Korea

- 5.2.3.6 Malaysia

- 5.2.3.7 Thailand

- 5.2.3.8 Indonesia

- 5.2.3.9 Vietnam

- 5.2.3.10 Rest of Asia-Pacific

- 5.2.4 Middle East and Africa

- 5.2.4.1 Saudi Arabia

- 5.2.4.2 United Arab Emirates

- 5.2.4.3 Nigeria

- 5.2.4.4 Egypt

- 5.2.4.5 Qatar

- 5.2.4.6 South Africa

- 5.2.4.7 Rest of Middle East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Colombia

- 5.2.5.4 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted & SWOT Analysis for Leading Players

- 6.3 Company Profiles

- 6.3.1 Asahi Kasei Corporation

- 6.3.2 Toray Battery Separator Film Co. Ltd

- 6.3.3 Freudenberg Performance Materials

- 6.3.4 SK ie Technology Corporation Ltd

- 6.3.5 Entek International

- 6.3.6 Sumitomo Chemical Co. Ltd

- 6.3.7 Ube Maxell Co. Ltd

- 6.3.8 W-Scope Corporation

- 6.3.9 Daramic

- 6.3.10 Amer SIL

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Enhanced Separator Materials

2025 年至 2033 年鋰離子電池隔膜市場報告,按材料(聚丙烯 (PP)、聚乙烯 (PE)、尼龍等)、厚度(16µm、20µm、25µm)、最終用戶(工業、消費電子、汽車等)和地區分類

2025 年至 2033 年鋰離子電池隔膜市場報告,按材料(聚丙烯 (PP)、聚乙烯 (PE)、尼龍等)、厚度(16µm、20µm、25µm)、最終用戶(工業、消費電子、汽車等)和地區分類 電池隔膜市場,按電池、隔膜、材料、技術、應用、國家和地區分類 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

電池隔膜市場,按電池、隔膜、材料、技術、應用、國家和地區分類 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測 2025 年電池隔膜全球市場報告

2025 年電池隔膜全球市場報告 中國電動汽車電池隔膜:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

中國電動汽車電池隔膜:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 中東和非洲電動車電池分離器市場佔有率分析、產業趨勢、統計和成長預測(2025-2030)

中東和非洲電動車電池分離器市場佔有率分析、產業趨勢、統計和成長預測(2025-2030) 亞太地區電動汽車電池分離器:市場佔有率分析、產業趨勢與成長預測(2025-2030)

亞太地區電動汽車電池分離器:市場佔有率分析、產業趨勢與成長預測(2025-2030) 全球電動車鋰離子電池隔離膜市場:市場佔有率分析、產業趨勢與成長預測(2025-2030)

全球電動車鋰離子電池隔離膜市場:市場佔有率分析、產業趨勢與成長預測(2025-2030) 北美電動車電池分離器:市場佔有率分析、產業趨勢、成長預測(2025-2030)

北美電動車電池分離器:市場佔有率分析、產業趨勢、成長預測(2025-2030) 南美洲電動車電池分離器:市場佔有率分析、產業趨勢與成長預測(2025-2030)

南美洲電動車電池分離器:市場佔有率分析、產業趨勢與成長預測(2025-2030) 印度電動車電池分離器:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

印度電動車電池分離器:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)