|

市場調查報告書

商品編碼

1636447

亞太地區電動汽車電池分離器:市場佔有率分析、產業趨勢與成長預測(2025-2030)Asia Pacific Electric Vehicle Battery Separator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

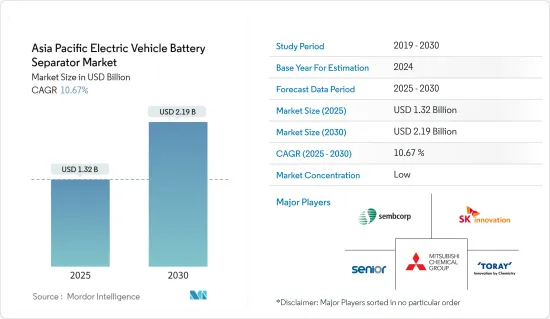

預計2025年亞太地區電動車電池隔膜市場規模為13.2億美元,2030年將達21.9億美元,預測期間(2025-2030年)複合年成長率為10.67%。

主要亮點

- 從中期來看,電動車的普及和鋰離子電池價格的下降預計將在預測期內推動市場發展。

- 另一方面,先進隔膜,尤其是具有高熱穩定性和機械強度的隔膜的製造成本較高,預計將抑制未來市場的成長。

- 其他電池化學材料(例如固態電池、先進鋰離子化學材料和鈉離子電池)的研發進展預計將為未來的市場提供機會。

- 預計中國將佔據重要的市場佔有率,這主要是由於其在電動車電池製造能力方面的主導地位。

亞太地區電動汽車電池隔膜市場趨勢

鋰離子電池領域可望主導市場

- 電池隔膜是多孔膜,對於鋰離子電池至關重要。透過將正極和負極分開並僅允許鋰離子通過,可以防止電氣短路。

- 近年來,鋰離子電池憑藉著能量密度高、循環壽命長、效率高等優點,已成為電動車(EV)的主流技術。

- 此外,推動綠色交通正在刺激整個亞太地區電動車產量的增加,其中中國、日本和韓國等國家處於領先地位。

- 隨著鋰離子電池的價格持續下降,其在電動車中的採用預計會增加,對鋰離子電池隔膜的需求預計也會增加。特別是,2023年鋰離子電池組的價格將比與前一年同期比較%,穩定在139美元/kWh。

- 持續的研發工作正在提高電池性能、成本效率和安全性,並專注於可提高鋰離子電池效率的電池隔膜的進步。

- 例如,2023年5月,SKIET與欣旺達簽署了一份合作備忘錄,根據該備忘錄,SKIET將供應電池隔膜。該合作夥伴關係還包括一項技術共用協議,旨在加強分離器在技術力、品質和有競爭力的價格方面的供應。

- 鑑於對鋰離子電池的需求不斷成長以及電動車電池隔膜的進步,該細分市場預計將獲得顯著的市場佔有率。

預計中國將佔較大佔有率

- 中國是亞太地區電動車主要生產國和消費國。中國大力推動電動化,刺激了電動車電池的需求,帶動了電池隔膜市場。

- 為促進電動車的普及,中國政府推出了一系列措施和補貼。這些措施包括稅收優惠、對電動車製造商的直接財政支持以及對充電基礎設施的大量投資,所有這些都正在加強電池隔膜市場。

- 此外,電動車的使用在中國正在迅速擴大,中國致力於減少空氣污染,並承諾在 2060 年實現碳中和。這種激增直接擴大了對高性能鋰離子電池以及電池隔離膜的需求。

- 國際能源總署的資料顯示,2023年中國電動車銷量將達810萬輛,較2022年的590萬輛大幅成長。展望未來,隨著中國電動車電池技術的不斷創新,電動車電池隔膜的需求預計將增加。國內企業正在投入資源進行研發,旨在生產先進的分離器,以提高安全性、卓越的效率和成本效益。

- 例如,2023年9月,深圳星源材料與布魯克納機械製造有限公司合作推出了第五代電池隔膜BSF生產線,年產能達2.5億平方公尺。此類戰略投資預計將增加未來幾年對電池隔膜的需求。

- 鑑於電動車的快速普及和技術的持續進步,中國可能在可預見的未來保持其市場主導地位。

亞太地區電動汽車電池隔膜產業概況

亞太地區電動汽車電池隔膜市場呈半截結構。該市場的主要企業包括(排名不分先後)Senior plc、SK Innovation、三菱化學集團公司、東麗工業公司和勝科工業有限公司。

其他好處

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2029年之前的市場規模與需求預測(單位:美元)

- 最新趨勢和發展

- 政府法規和措施

- 市場動態

- 促進因素

- 政府對電池製造的措施和投資

- 電池原物料成本下降

- 抑制因素

- 生產成本高

- 促進因素

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵對關係

- 投資分析

第5章市場區隔

- 電池類型

- 鋰離子

- 鉛酸

- 其他電池類型

- 材料類型

- 聚丙烯

- 聚乙烯

- 其他

- 地區

- 中國

- 印度

- 澳洲

- 日本

- 馬來西亞

- 泰國

- 印尼

- 越南

- 其他亞太地區

第6章 競爭狀況

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- Senior plc

- SK Innovation Co. Ltd

- Mitsubishi Chemical Group Corporation

- Toray Industries Inc.

- Sembcorp Industries Ltd

- UBE Corporation

- Teijin Ltd

- Hitachi Chemical Company Ltd

- Yunnan Enjie New Materials Co. Ltd

- Cangzhou Mingzhu Plastic Co. Ltd

- 其他知名公司名單

- 市場排名分析

第7章 市場機會及未來趨勢

- 增加其他電池化學物質的研究和開發

簡介目錄

Product Code: 50003714

The Asia Pacific Electric Vehicle Battery Separator Market size is estimated at USD 1.32 billion in 2025, and is expected to reach USD 2.19 billion by 2030, at a CAGR of 10.67% during the forecast period (2025-2030).

Key Highlights

- Over the medium period, the growing adoption of electric vehicles and the decreasing price of lithium-ion batteries is expected to drive the market in the forecast period.

- On the other hand, high production cost, especially for advanced separators with higher thermal stability and mechanical strength, is expected to restrain market growth in the future.

- Nevertheless, the increasing research and development of other battery chemistries like solid-state batteries, advanced lithium-ion chemistry, Sodium-ion batteries, etc, are expected to create an opportunity for the market in the future.

- China is poised to command a substantial market share, primarily due to its dominance in electric vehicle battery manufacturing capacity.

Asia Pacific Electric Vehicle Battery Separator Market Trends

Lithium-ion Battery Segment is Expected to Dominate the Market

- A battery separator, a porous membrane, is vital in lithium-ion batteries. It prevents electrical short circuits by isolating the cathode and anode, allowing only lithium ions to pass through.

- Recently, lithium-ion batteries have become the dominant technology in electric vehicles (EVs), thanks to their high energy density, long cycle life, and efficiency.

- Moreover, as countries like China, Japan, and South Korea lead the way, the push for greener transportation has spurred a rise in EV production across the Asia-Pacific (APAC) region.

- As lithium-ion battery prices continue to decline, their adoption in EVs is set to rise, subsequently increasing the demand for lithium-ion battery separators. Notably, in 2023, lithium-ion battery pack prices dropped by 14% from the previous year, settling at USD139/kWh.

- Ongoing R&D efforts are enhancing battery performance, cost efficiency, and safety, spotlighting advancements in battery separators that boost lithium-ion battery efficacy.

- For example, in May 2023, SKIET and Sunwoda inked a memorandum of understanding, with SKIET set to supply battery separators. The collaboration also includes a technology-sharing agreement, aiming to enhance separator supply in terms of technological prowess, quality, and competitive pricing.

- Given the rising demand for lithium-ion batteries and advancements in battery separators for EVs, this segment is poised to capture a substantial market share.

China is Expected to have a Significant Share

- China stands as the leading producer and consumer of electric vehicles in the Asia-Pacific region. The nation's vigorous push towards electrification has spurred a significant demand for electric vehicle batteries, subsequently propelling the market for battery separators.

- To promote the adoption of EVs, the Chinese government has rolled out a series of policies and subsidies. These measures encompass tax incentives, direct financial support to EV manufacturers, and substantial investments in charging infrastructure, all of which fortify the battery separator market.

- Moreover, with a heightened emphasis on curbing air pollution and a commitment to achieving carbon neutrality by 2060, China's embrace of EVs is rapidly escalating. This surge is directly amplifying the demand for high-performance lithium-ion batteries and, consequently, battery separators.

- Data from the International Energy Agency reveals that China's EV car sales reached 8.1 million units in 2023, a notable rise from 5.9 million units in 2022. Looking ahead, as the nation continues to innovate in electric vehicle battery technology, the appetite for EV battery separators is set to grow. Domestic firms are pouring resources into R&D, aiming to craft advanced separators that promise enhanced safety, superior efficiency, and cost-effectiveness.

- As an illustration, in September 2023, Shenzhen Senior Technology Material Co., Ltd., in collaboration with Bruckner Maschinenbau, launched a 5th generation BSF production line for battery separators, boasting an impressive annual capacity of 250 million square meters. Such strategic investments are poised to amplify the demand for battery separators in the coming years.

- Given the surging adoption of EVs and ongoing technological advancements, China is poised to maintain its market dominance in the foreseeable future.

Asia Pacific Electric Vehicle Battery Separator Industry Overview

The Asia Pacific electric vehicle battery separator market is semi-fragmented. Some of the major players in the market (in no particular order) include Senior plc, SK Innovation Co. Ltd, Mitsubishi Chemical Group Corporation, Toray Industries Inc., and Sembcorp Industries Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Government Policies and Investments towards battery manufacturing

- 4.5.1.2 Decline in cost of battery raw materials

- 4.5.2 Restraints

- 4.5.2.1 High Production Cost

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion

- 5.1.2 Lead-Acid

- 5.1.3 Other Battery Types

- 5.2 Material Type

- 5.2.1 Polypropylene

- 5.2.2 Polyethylene

- 5.2.3 Other Material Types

- 5.3 Geography

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Australia

- 5.3.4 Japan

- 5.3.5 Malaysia

- 5.3.6 Thailand

- 5.3.7 Indonesia

- 5.3.8 Vietnam

- 5.3.9 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Senior plc

- 6.3.2 SK Innovation Co. Ltd

- 6.3.3 Mitsubishi Chemical Group Corporation

- 6.3.4 Toray Industries Inc.

- 6.3.5 Sembcorp Industries Ltd

- 6.3.6 UBE Corporation

- 6.3.7 Teijin Ltd

- 6.3.8 Hitachi Chemical Company Ltd

- 6.3.9 Yunnan Enjie New Materials Co. Ltd

- 6.3.10 Cangzhou Mingzhu Plastic Co. Ltd

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Increasing Research and Development of Other Battery Chemistries

02-2729-4219

+886-2-2729-4219

2025 年至 2033 年鋰離子電池隔膜市場報告,按材料(聚丙烯 (PP)、聚乙烯 (PE)、尼龍等)、厚度(16µm、20µm、25µm)、最終用戶(工業、消費電子、汽車等)和地區分類

2025 年至 2033 年鋰離子電池隔膜市場報告,按材料(聚丙烯 (PP)、聚乙烯 (PE)、尼龍等)、厚度(16µm、20µm、25µm)、最終用戶(工業、消費電子、汽車等)和地區分類 電池隔膜市場,按電池、隔膜、材料、技術、應用、國家和地區分類 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

電池隔膜市場,按電池、隔膜、材料、技術、應用、國家和地區分類 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測 2025 年電池隔膜全球市場報告

2025 年電池隔膜全球市場報告 SLI用鉛酸電池隔離膜的全球市場:市場佔有率分析、產業趨勢與成長預測(2025-2030年)

SLI用鉛酸電池隔離膜的全球市場:市場佔有率分析、產業趨勢與成長預測(2025-2030年) 中國電動汽車電池隔膜:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

中國電動汽車電池隔膜:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030) 中東和非洲電動車電池分離器市場佔有率分析、產業趨勢、統計和成長預測(2025-2030)

中東和非洲電動車電池分離器市場佔有率分析、產業趨勢、統計和成長預測(2025-2030) 全球電動車鋰離子電池隔離膜市場:市場佔有率分析、產業趨勢與成長預測(2025-2030)

全球電動車鋰離子電池隔離膜市場:市場佔有率分析、產業趨勢與成長預測(2025-2030) 北美電動車電池分離器:市場佔有率分析、產業趨勢、成長預測(2025-2030)

北美電動車電池分離器:市場佔有率分析、產業趨勢、成長預測(2025-2030) 南美洲電動車電池分離器:市場佔有率分析、產業趨勢與成長預測(2025-2030)

南美洲電動車電池分離器:市場佔有率分析、產業趨勢與成長預測(2025-2030) 印度電動車電池分離器:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

印度電動車電池分離器:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)

▼