|

市場調查報告書

商品編碼

1643224

電信託管服務:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Telecom Managed Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

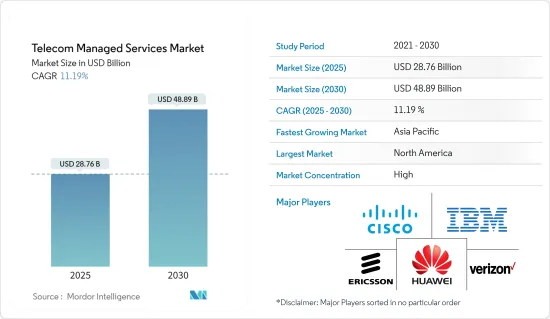

電信託管服務市場規模預計在 2025 年為 287.6 億美元,預計到 2030 年將達到 488.9 億美元,預測期內(2025-2030 年)的複合年成長率為 11.19%。

由於各種技術的採用率很高、BYOD 政策審查頻率增加(以使業務營運更加舒適和易於管理)以及由於組織中資料的快速成長而對高階安全性的需求不斷增加,通訊領域已成為託管服務的重要市場。

關鍵亮點

- 過去幾年,通訊產業經歷了顯著的成長。在競爭激烈的市場中,電信業者不斷面臨以低成本提供創新服務以留住客戶的壓力。網路最佳化需求的持續成長和網路效能的顯著提升、SDN、5G 和 NFV 等技術的進步、智慧型手機的日益普及和 BYOD 趨勢、以及網路攻擊數量的增加等因素將在預測期內進一步推動通訊託管服務市場的成長。

- 隨著電訊業務的蓬勃發展,各大公司紛紛轉向 MSP(託管服務供應商)。 MSP 提供重要的服務水平,幫助公司實現更好的業務成果。企業通常面臨收益、業務轉型、成本採用以及通訊領域日益激烈的市場競爭等若干挑戰,而這些挑戰都依賴 MNO 和 CSP。此外,各種 SD-WAN 託管服務供應商透過廣泛的安全產品來區分自己。例如,Cato Networks 提供一個雲端原生平台,其中包括 NGFW、進階威脅預防、CloudSecure Web 閘道、行動存取保護以及託管威脅偵測和回應服務。

- 電信公司也在收購託管服務供應商,以佔領更大的市場佔有率。例如,今年早些時候,網路系統、服務和軟體供應商 Ciena Corporation 披露,它已簽署具有約束力的協議,收購總部位於加州佩塔盧馬的非上市Tibit Communications, Inc.,以及在馬薩諸塞州伯靈頓設有辦事處的非上市公司 Benu Networks, Inc.。 Tibit 和 Benu 主要致力於透過新一代 PON 技術增強用戶管理和簡化寬頻存取網路。

- 預計在預測期內,公司對資料保密性、業務外包和確保客戶最佳分工的安全疑慮等決定性因素將限制市場成長。

- 然而,COVID-19 疫情已影響到全球的營運服務,包括通訊管理服務和支援服務。此外,疫情已導致大量公司轉向長期在家工作的文化。因此,大多數企業都轉向能夠為他們提供增值服務的服務供應商,以幫助最大限度地降低各種與安全相關的風險,從而成倍地擴大市場。

電信管理服務市場趨勢

雲端運算的使用增加預計將推動市場成長

- 通訊領域受到雲端運算的嚴重影響。在過去五年中,雲端運算的普及度大幅成長。它對商業、技術和資訊技術領域產生了重大影響。這導致全球在雲端運算方面的支出增加。總體而言,它降低了電訊部門的營運和管理成本,同時在廣泛的內容傳輸網路上保持了統一的通訊和團隊合作。雲端服務供應商使電訊業能夠專注於其核心功能,而不必擔心更新和維護 IT 和伺服器。

- 市場成長的關鍵驅動力是雲端運算技術的採用日益廣泛,尤其是在中小型企業中,以及行動性和巨量資料服務等技術的快速進步以提高業務效率。雲端運算為電訊業提供了廣泛的機會。它利用先進的技術顯著擴大了全球通訊的覆蓋範圍,因為它可以幫助企業改善業務並更有效地利用技術。雲端運算的好處包括雲端傳輸模式、通訊服務、網路服務、可擴展且靈活的基礎設施,以及高效且靈活的資源分配和管理。此外,雲端運算還降低了硬體成本,因為服務供應商可以以低價提供軟體,並藉助虛擬和配置軟體分配高效的運算資源。

- 雲端運算市場正在經歷主要企業的多次收購、合併和投資。例如,今年最後一個季度,Colt Technology Services 與 IBM 的合作邁出了新的方向,兩家公司在英國開設了一個新的工業 4.0 實驗室。 IBM 提供其 Maximo 應用程式套件和 Cloud Satellite混合雲端,而 Colt 提供其 Colt Edge 運算平台和 SD-WAN 技術。憑藉三個關鍵邊緣使用案例——視覺檢查推理、供應鏈遠端檢測、威脅監控和資料保護,兩人最初專注於製造業。

- 此外,亞馬遜網路服務宣布將於 2022 年第四季在瑞士推出一個新的雲端運算區域。 2036年,AWS 歐洲地區每年將在工程、通訊、設施維護和建設等各領域新增 2,500 名全職員工。根據 AWS 介紹,三個可用區將組成新的蘇黎世雲區域。每個可用區資料中心都有獨立的電源、實體安全、冷卻系統和低延遲網路連線。這些可用區為高可用性應用程式提供了增強的容錯能力,最大限度地減少了服務中斷。

- 根據 Digital Ocean 的數據,2021 年,74% 的企業表示他們使用 AWS EC2 和 Azure VM 等雲端託管/基礎設施服務。企業也大量使用平台即服務 (PaaS) 解決方案,例如 Heroku 和 Azure App Service。值得注意的是,傳統的中小企業通常使用較少的雲端服務,因此其雲端設定不太複雜。因此,隨著企業採用雲端託管/基礎設施服務的整體增加,市場預計將呈指數級成長。

北美主導電信管理服務市場

- 北美貢獻了最大的市場佔有率,預計將在預測期內主導電信託管服務市場。預計該地區的市場將快速成長。推動北美市場成長的因素包括快速發展的技術進步、全球通訊公司尋求最佳化網路投資和提高客戶滿意度以及該地區網路攻擊的增加。

- 此外,該地區伺服器配置錯誤問題的增加也是推動市場擴張的主要因素之一。許多公司都經歷過伺服器配置錯誤,這是導致個人資訊外洩的主要原因。這導致人們更加關注具有透過附加價值服務全面降低安全相關風險能力的電訊託管服務供應商。 SOCRadar 已確認該伺服器的錯誤配置導致約 65,000 家企業的敏感資料外洩。 SOCRadar發現,錯誤配置的伺服器暴露了約65,000家公司的敏感資料。因此,該地區配置錯誤的伺服器的增加極大地促進了市場的成長。

- 此外,隨著現代技術的快速發展和簡化 IT 功能的需求,該地區越來越多的企業發現,借助電信 MSP 的幫助可以最好地跟上步伐。此外,市場還見證了主要企業推出的各種產品和創新,這是他們改善業務、接觸客戶和擴大影響力以滿足多種應用需求的策略的一部分。

- 例如,今年早些時候,AT&T 推出了 AT&T 託管無線 WAN,這是一個由 AT&T 網路專家運行的即插即用系統,可為任何地方的任意數量的固定站點提供快速、靈活和安全的無線行動電話接入。此外,今年第二電訊,Emersion 宣布公共產業加速其北美企業發展。

- 此外,智慧型手機和平板電腦在美國越來越受歡迎,BYOD政策正在推行。預計全部區域不斷上升的設備普及率和強大的網路連接將鼓勵各組織採用 BYOD 計劃。此外,該地區主要通訊業者的存在和資料中心的不斷增加也有望推動市場的發展。此外,對提高業務流程業務效率和可靠性的需求日益成長,這也大大推動了該地區市場的發展。

電信管理服務業概況

電信管理服務市場正在整合,大型企業佔據市場主導地位。各行業的主要供應商都計劃對該市場進行大量投資。因此,未來幾年市場將經歷巨大的成長。主要企業正在採用多種有機和無機成長策略,例如併購、聯盟/夥伴關係關係和合資企業,以在市場上佔據強勢地位。市場的一些關鍵發展包括:

- 2022 年 11 月-通訊領域供應商 Agility Communications Group 被 BlackPoint IT Services 收購。主要原因是提供更全面的端到端 IT 服務和電訊能力,以支援美國以及亞洲和歐洲分公司的客戶。

- 2022 年 8 月 - Verizon 和全球領先的消費信貸機構 Nova Credit 宣布擴大合作夥伴關係,作為其旗艦零售計劃的一部分,透過電話或在選定的 Verizon 地點店內對新客戶進行外國信用檢查。該合作關係將允許 Verizon 提取潛在客戶的國際信用檔案並將其轉換為可用於獲得貸款資格的信用評分。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭強度

- COVID-19 對電信管理服務市場的影響評估

第5章 市場動態

- 市場促進因素

- 對電訊業務流程中提高業務效率、安全性和靈活性的需求

- 最大限度地降低企業基礎設施管理成本

- 市場限制

- 確保為客戶提供最佳部門

第6章 市場細分

- 按組織規模

- 大型企業

- 中小型企業

- 按服務類型

- 託管資料中心服務

- 資安管理服務

- 主機服務

- 管理資料和資訊服務

- 其他服務類型(託管通訊服務、行動化營運服務)

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

第7章 競爭格局

- 公司簡介

- Cisco Systems Inc.

- Huawei Technologies Co. Ltd

- International Business Machines Corporation

- Telefonaktiebolaget LM Ericsson

- Verizon Communications Inc.

- AT&T Inc.

- NTT Data Corporation

- Unisys Corporation

- Comarch SA

- GTT Communications Inc.

- Amdocs Inc.

- ZTE Corporation

- Nokia Corporation

- Tech Mahindra Limited

- Fujitsu Limited

第8章投資分析

第9章 市場機會與未來趨勢

The Telecom Managed Services Market size is estimated at USD 28.76 billion in 2025, and is expected to reach USD 48.89 billion by 2030, at a CAGR of 11.19% during the forecast period (2025-2030).

The telecom sector is a significant market for managed services due to the high rate of various technological adoptions, increased frequency of confirmation of the BYOD policy (to make business operations much more comfortable and controllable), and the increased need for high-end security due to the rapidly increasing data among the organizations.

Key Highlights

- The telecom industry observed extensive growth during the past few years. Telecommunication companies are constantly pressured to deliver innovative services at lower costs to retain their customers in the competitive market. The factors, such as the constant requirement for network optimizations and the significant level of network performance, advancements in technologies, such as SDN, 5G, and NFV, growing smartphone usage and BYOD trends, and the growing number of cyber-attacks, will further encourage the growth of the telecom managed services market during the forecast period.

- Since telecom businesses are increasing rapidly, enterprises frequently rely on MSPs (Managed Service Providers). An MSP helps enterprises achieve excellent business outcomes by providing a significant level of service. The companies mostly face several challenges in terms of revenue, business transformation, cost implementation, and heightened competition in the marketplace in the telecom sector, due to which they depend on MNOs and CSPs. Moreover, various SD-WAN-managed service providers distinguish themselves with a broad range of security offerings. For instance, Cato Networks gives a cloud-native platform that includes NGFW, Advanced Threat Prevention, CloudSecure Web Gateway, Mobile Access Protection, and Managed Threat Detection and Response service.

- Telecom companies are also acquiring managed service providers to gain a more significant market share. For instance, recently this year, Networking systems, services, and software provider Ciena Corporation revealed that it had signed a binding agreement to buy privately held Tibit Communications, Inc. with headquarters in Petaluma, California, as well as privately held Benu Networks, Inc. with offices in Burlington, Massachusetts. Tibit and Benu mainly focus on simplifying broadband access networks with enhanced subscriber management and next-generation PON technologies.

- Determinants, such as security concerns related to the confidentiality of data of businesses that are outsourcing the business and assuring the optimum business functionality of the clients, are expected to restrict the market growth during the forecast period.

- However, due to the COVID-19 outbreak, operational services, like telecom managed services and support services, were affected globally. Moreover, due to this pandemic, a broad range of firms has significantly undergone a long-term work-from-home culture. Hence, most organizations are turning to service providers for their ability to minimize various security-related risks with the value-added service they offer, which drives the market exponentially.

Telecom Managed Services Market Trends

Rise in the Usage of Cloud Computing is Expected to Drive the Market Growth Significantly

- The telecom sectors have been significantly impacted by cloud computing. For the past five years, cloud computing has experienced tremendous growth in popularity. It greatly affects the business, technology, and information technology sectors. This has caused a rise in global spending on cloud computing. Overall, it decreased operational and administrative costs in the telecom sector while preserving unified communication and teamwork with an extensive Content Delivery Network. Cloud service providers let the telecom industry concentrate on core business functions rather than IT, server updates, or upkeep concerns.

- The primary drivers of the market's growth are the increasing adoption of cloud computing technologies, especially by small and medium-sized businesses, and the rapid advancement of technology, including mobility and big data services, to improve operational efficiency. Cloud Computing offers a broad range of opportunities in the telecom industry. It could help companies improve their business and use technology more efficiently, so it has significantly increased the reach of telecommunications worldwide using advanced technologies. Some of its benefits include Cloud Delivery Model, Communication Services, Network Services, Highly scalable and flexible infrastructure, Efficient and flexible resource allocation and management, etc. Moreover, using cloud computing, service providers can provide software at lower rates with the help of virtualization and provisioning software, allocating efficient computing resources and thus reducing hardware costs as well.

- The market is witnessing several acquisitions, mergers, and investments by key players as part of its strategy to improvise business and its presence to reach customers and meet their requirements for various applications. For instance, recently, in the last quarter of this year, Colt Technology Services and IBM's cooperative relationship took a new direction when the two joined up to open a new Industry 4.0 lab in the United Kingdom where businesses can try edge cloud services. While IBM will give its Maximo Application Suite and Cloud Satellite hybrid cloud, Colt will contribute its Colt Edge computing platform and SD-WAN technology. With three critical edge use cases-visual inspection-based inferencing, supply chain telemetry, threat monitoring, and data protection-the duo initially focuses on the manufacturing industry.

- Moreover, in the Q4 of the year 2022, Amazon Web Services declared the introduction of a new cloud computing region in Switzerland. Through 2036, the corporation would add 2,500 full-time employees yearly in various sectors, including engineering, telecommunications, facility maintenance, and construction, due to the Europe AWS area. According to AWS, three availability zones make up the new cloud region in Zurich. Each availability zone's data centers have access to separate power, physical security, a cooling system, and a low-latency network connection. These availability zones should offer improved fault tolerance for high-availability applications to ensure minimal service interruption.

- As per Digital Ocean, In 2021, 74 % of enterprises indicated using cloud hosting/infrastructure services such as AWS EC2 or Azure VMs. Enterprises are also using the platform as a service (PaaS) solution, including Heroku or Azure App Service, to a great extent. Notably, traditional small and midsize businesses generally use fewer cloud services and therefore have less complex cloud setups. Hence the overall rise in the usage of cloud hosting/infrastructure services by enterprises will drive the market exponentially.

North America to Dominate the Telecom Managed Services Market

- North America held the most significant market share and is anticipated to dominate the telecom-managed services market during the forecast period. The market will experience an abrupt rise in this region. The factors encouraging the growth of the market in North America include quickly evolving technological developments, the presence of the world's largest telecom firms looking to optimize their network investments & intensify customer satisfaction, and rising network cyber-attacks in this region.

- Moreover, the rise in misconfigured servers within the region is also one of the significant reasons behind the market expansion. Various firms are experiencing misconfigured servers which lead to the prime cause of personal data being compromised. Hence, they are significantly turning to telecom-managed service providers for their overall ability to reduce security-related risks with their value-added services. Recently this year, Microsoft, a US-based company, confirmed that a misconfiguration of a Microsoft server endpoint exposed specific customer data, including emails and personal information.SOCRadar has identified that sensitive data of around 65,000 entities became public due to this misconfigured server. Hence, the rise in misconfigured servers in the region significantly drives the market's growth.

- Moreover, with the speedy acceleration of modern technology and the need for streamlined IT functions, an increasing number of businesses in the region are finding it best to keep pace with the help of Telecom MSP. Additionally, the market is witnessing various product launches and innovations by key players as part of its strategy to improve business and their presence to reach customers and meet their requirements for multiple applications.

- For instance, earlier this year, to provide fast, flexible, and secure wireless cellular access to any number of fixed sites, anywhere, AT&T offered AT&T Managed Wireless WAN, a plug-and-play system run by AT&T network professionals. Moreover, in the 2nd quarter of this year, Emersion, whose powerful business automation platform supercharges billing, provisioning, and order flow for telecom, MSP, and utility businesses, announced the acceleration of its presence in North America.

- Further, the penetration of smartphones and tablets is increasing in the United States, which in turn is driving the BYOD policy. The increasing penetration of devices and robust network connectivity across the region are expected to encourage organizations to adopt BYOD policies. Additionally, the presence of key telecom players in the region and the increasing deployment of data centers is expected to drive the market. Also, the rise in the need for improved operational efficiency and reliability in business processes is exponentially driving the market in the region.

Telecom Managed Services Industry Overview

The telecom-managed services market is consolidated, and significant players dominate it. Primary vendors across various verticals are planning for considerable investments in this market. As a result, the market is poised to grow at an extraordinary rate in the upcoming years. The principal players are embracing several organic and inorganic growth strategies, like mergers and acquisitions, collaboration and partnerships, and joint ventures, to gain a strong position in the market. Some of the critical development in the market are:

- November 2022 - Agility Communications Group, a provider in the telecommunications sector, has been acquired by BlackPoint IT Services. The key reason behind this is to provide end-to-end IT services and telecoms with even more comprehensive capabilities to assist their clientele across the United States and their branch offices in Asia and Europe.

- August 2022 - As part of its flagship retail program, Verizon and Nova Credit, the top consumer-permission credit agency in the world, have announced that they have expanded their partnership to conduct foreign credit checks for clients new to the country over the phone and in some Verizon stores. With the help of this cooperation, Verizon will be able to pull prospective customers' international credit files and convert them into credit scores that could make them eligible for financing.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Telecom Managed Services Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Demand for Enhanced Operational Efficiency, Security, and Agility in Telecom Business Process

- 5.1.2 Cost Minimization in Managing Enterprise Infrastructure

- 5.2 Market Restraints

- 5.2.1 Assuring the Optimum Business Functionality of the Customers

6 MARKET SEGMENTATION

- 6.1 By Organization Size

- 6.1.1 Large Enterprises

- 6.1.2 Small and Medium Enterprises

- 6.2 By Service Type

- 6.2.1 Managed Data Center Services

- 6.2.2 Managed Security Services

- 6.2.3 Managed Network Services

- 6.2.4 Managed Data and Information Services

- 6.2.5 Other Service Types (Managed Communication Services and Managed Mobility Services)

- 6.3 Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle-East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems Inc.

- 7.1.2 Huawei Technologies Co. Ltd

- 7.1.3 International Business Machines Corporation

- 7.1.4 Telefonaktiebolaget LM Ericsson

- 7.1.5 Verizon Communications Inc.

- 7.1.6 AT&T Inc.

- 7.1.7 NTT Data Corporation

- 7.1.8 Unisys Corporation

- 7.1.9 Comarch SA

- 7.1.10 GTT Communications Inc.

- 7.1.11 Amdocs Inc.

- 7.1.12 ZTE Corporation

- 7.1.13 Nokia Corporation

- 7.1.14 Tech Mahindra Limited

- 7.1.15 Fujitsu Limited

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

託管服務,全球市場,2025-2029

託管服務,全球市場,2025-2029 歐洲託管基礎設施服務:市場佔有率分析、行業趨勢和成長預測(2025-2030)

歐洲託管基礎設施服務:市場佔有率分析、行業趨勢和成長預測(2025-2030) 歐洲託管服務:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

歐洲託管服務:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 管理資訊服務:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

管理資訊服務:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 託管IT基礎設施服務 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

託管IT基礎設施服務 -市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 託管基礎設施服務:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

託管基礎設施服務:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 託管通訊服務:市場佔有率分析、產業趨勢、成長預測(2025-2030)

託管通訊服務:市場佔有率分析、產業趨勢、成長預測(2025-2030) 非洲的託管服務:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

非洲的託管服務:市場佔有率分析、行業趨勢和成長預測(2025-2030 年) 託管服務市場:按服務類型、組織規模、最終用途、部署模型分類 - 2025-2030 年全球預測

託管服務市場:按服務類型、組織規模、最終用途、部署模型分類 - 2025-2030 年全球預測 全球託管服務市場:按服務類型(資安管理服務、託管工作服務、託管IT基礎設施和資料中心服務、託管通訊和協作服務、行動化營運服務、託管資訊服務)、按部署類型、按組織規模、按產業和地區 - 2029 年預測

全球託管服務市場:按服務類型(資安管理服務、託管工作服務、託管IT基礎設施和資料中心服務、託管通訊和協作服務、行動化營運服務、託管資訊服務)、按部署類型、按組織規模、按產業和地區 - 2029 年預測