|

市場調查報告書

商品編碼

1644284

日本低溫運輸物流-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Japan Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

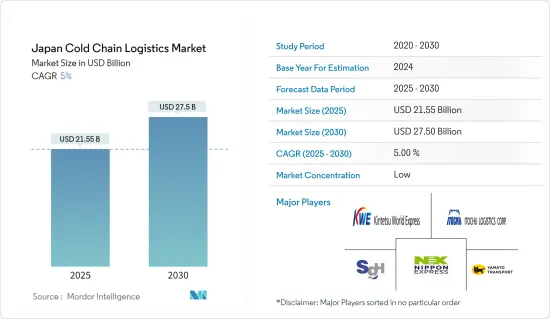

日本低溫運輸物流市場規模預計在2025年為215.5億美元,預計到2030年將達到275億美元,預測期內(2025-2030年)的複合年成長率為5%。

受新冠疫情影響,日本貿易工業部報告稱,2020 年 3 月藥局銷售額較去年同期成長了 7.5%。對此,日本超級市場協會表示,為滿足自我隔離和居家烹飪需求,2020年3月超級市場食品需求和銷售額與去年同期相比成長了7.4%。這些因素都對日本低溫運輸物流市場產生了負面影響。新冠疫情對日本的低溫運輸業務產生了影響,包括人們對食品安全的擔憂加劇。

日本被認為是低溫運輸物流的成熟市場,由多家參與企業主導。由於生物製藥和再生醫學的快速發展,日本近年來對藥品冷鏈的需求不斷增加。隨著 COVID-19 疫苗和其他治療方法的採用,預計這一趨勢將持續下去。日本的低溫運輸物流最初是針對生鮮、冷藏和冷凍食品產業而建立的。低溫運輸物流注重始終在溫度和濕度受控的環境中及時分銷產品。

日本的冷藏倉庫大多由大型低溫運輸公司擁有並經營,只有少數設施可供租賃。隨著利用電子商務銷售冷凍冷藏產品的不斷進步,有潛在需求的地區將會加速建造冷藏倉庫。

冷藏倉庫數量的增加和醫藥行業的成長等因素預計將推動日本低溫運輸物流市場的成長。市場挑戰包括冷藏能力分佈不均、缺乏適當的物流連接支援以及需要高額的資本投入。

日本低溫運輸物流市場趨勢

現代家庭推動冷凍食品需求

作為現代家庭的解決方案,隨著老年人變得更加獨立,雙收入家庭和單人家庭的增加,對冷藏/冷凍食品的需求不斷增加,同時也帶來了食品浪費的風險以及食品和飲料行業勞動力短缺的日益加劇。

2021年日本冷凍食品消費量量約290萬噸。日本生產的受歡迎的冷凍食品包括餃子、炸丸子和小麥粉麵條(烏龍麵)。近年來,日本食品特別是農產品在世界各地熱銷。

日本人口老化和向更健康壽命的轉變正在推動冷凍食品的銷售。超級市場、大賣場和藥局的銷售量也大幅增加。由於冷凍技術的進步和新冠疫情期間對居家食品的需求增加,日本的冷凍食品變得更加多樣化。

名店的高價位家常小菜、道地的外國菜複製品等迅速佔領市場,迫使百貨商場、超級市場加速擴大銷售面積。

日本製藥業的成長

日本是世界上最大的醫藥市場之一,主要原因是其老化社會。在政府大力推廣學名藥的舉措下,該國也是先進醫療設備的主要生產國和進口國之一。

該國的生技藥品領域僅次於美國。再加上政府重點支持低成本假冒產品,生物相似藥存在著巨大的機會。日本為創新製藥公司提供了慷慨的獨佔期,但在學名藥的採用方面,該國正在趕上其他成熟市場。

國內藥廠擴大在全球分銷其產品,這也反映出人們對該體系的信心。隨著主要企業海外銷售比重穩定上升,對低溫運輸儲運設施的需求也日益增加。人們對日本製藥業興趣日益濃厚的另一個關鍵促進因素是需要加強日本的藥物研發生態系統。

日本新冠肺炎感染人數不斷上升,處方藥和疫苗的需求也隨之增加。這影響了藥品需求。新冠疫苗進口增加推動了藥品需求。例如,2021年5月,日本政府與輝瑞-BioNTech簽署契約,將在2021年終進口1.94億劑(133萬美元)疫苗。據 IQVIA 稱,2021 年日本處方藥市場價值約為 10.6 兆日圓(800 億美元),高於 2020 年的約 10.4 兆日圓(790 億美元)。

日本低溫運輸物流產業概況

市場相對分散,擁有眾多國內外參與企業,包括日本通運、大和號、佐川急便、伊藤忠物流公司和近鐵世界快捷。市場競爭與成本、倉儲費、空間和包裝材料價格的上漲有關。服務供應商仍在努力發展其提供流程標準化的能力。缺乏有關儲存溫度和工作流程的標準化是該行業面臨的另一個主要挑戰。可用冷藏空間的品質和靈活性是一個值得關注的問題。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 調查結果

- 調查前提

- 研究範圍

第2章調查方法

第3章執行摘要

第4章 市場動態與洞察

- 當前市場狀況

- 市場動態

- 驅動程式

- 醫療領域的重要性

- 消費者對生鮮食品的需求不斷增加

- 限制因素

- 包裝不當或損壞的產品

- 溫控混亂

- 機會

- 技術創新

- 驅動程式

- 技術趨勢和自動化

- 政府法規和舉措

- 產業價值鏈/供應鏈分析

- 環境/溫度控制儲存亮點

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 購買者/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

- 排放標準和法規對低溫運輸產業的影響

- COVID-19 對市場的影響

第5章 市場區隔

- 按服務

- 貯存

- 運輸

- 附加價值服務(速凍、標籤、庫存管理等)

- 按溫度類型

- 冷藏

- 冷凍

- 按應用

- 園藝(新鮮水果和蔬菜)

- 乳製品(牛奶、冰淇淋、奶油等)

- 肉類、魚類、家禽

- 加工食品

- 製藥、生命科學、化學

- 其他

第6章 競爭格局

- 市場集中度概覽

- 公司簡介

- Nippon Express

- Yamato Holdings

- Sagawa

- Kintetsu World Express

- Itochu Logistics Corp.

- DHL

- Kuehne Nagel

- K line Logistics

- Nichirei Logistics Group, Inc.

- Sojitz Corporation

- CEVA Logistics

- Kokubu Goup

- Agility

- SF Express*

第7章 日本低溫運輸物流市場的未來

第 8 章 附錄

The Japan Cold Chain Logistics Market size is estimated at USD 21.55 billion in 2025, and is expected to reach USD 27.50 billion by 2030, at a CAGR of 5% during the forecast period (2025-2030).

With COVID-19 in effect, the Japanese Trade Ministry reported a 7.5% Y-o-Y increase in the sale of drugstores in March 2020. Along with this, the Japan Supermarkets Association, in response to the self-imposed quarantines and the need to cook at home, reflected a 7.4% Y-o-Y increase in the demand and sales of groceries at the supermarkets in March 2020. All these factors led to a negative impact on the cold chain logistics market in Japan. COVID-19 impacted Japan's cold chain operations, including increased food safety concerns.

Japan is regarded as a mature market for cold chain logistics and is dominated by several players. Rapid advancements in biopharmaceuticals and regenerative medicine recently increased the demand for the cold pharmaceutical chain in Japan. This trend is expected to continue with the COVID-19 vaccines introduction and other treatments. Cold chain logistics in Japan was initially established for the fresh, refrigerated, and frozen food industries. Cold chain logistics focuses on the timely distribution of products within a constantly controlled temperature and humidity environment.

Most cold storage facilities in Japan are owned and operated by major cold chain corporations, with only a small number available for lease. Advances in using e-commerce to sell frozen and chilled goods will accelerate cold storage development in areas with latent needs.

Factors such as an increase in the number of refrigerated warehouses and growth in the pharmaceutical sector are expected to drive the growth of Japan's cold chain logistics market. Some of the challenges in the market are the irregular distribution of cold storage capacity, lack of proper logistical connectivity support, and the need for high capital investment.

Japan Cold Chain Logistics Market Trends

Modern Households Leading to Demand for Frozen Foods

The demand for chilled/frozen foods is increasing as a solution for modern-age families, such as independent elderly citizens, increase in dual-income households and single people, along with the danger of food loss and increasing overall labor shortages in the food and beverage industry.

In 2021, the consumption volume of frozen food in Japan amounted to about 2.9 million tons (USD 0.020 million tons). Popular frozen food products manufactured in Japan include dumplings (gyoza), croquettes, and wheat-flour noodles (udon). In recent years, Japanese food also exploded worldwide, especially agricultural products.

As the Japanese population ages, the shift to healthy life expectancy is a common desire of the people aiding the sale of frozen products. It also significantly increased in supermarkets, hypermarkets, and drugstores. Frozen food items in Japan became more diverse due to advances in refrigeration technology and growing demand for eat-at-home products amid the COVID-19 pandemic.

High-priced delicacies from well-known restaurants and authentic reproductions of food from abroad grew across the market, prompting department stores and supermarkets to speed up efforts to expand sales spaces.

Growth of Pharmaceutical Sector in Japan

Japan is one of the largest pharmaceutical markets in the world, primarily due to its aging population. It is also among the major producers and importers of advanced medical facilities backed by active government initiatives to promote generic drugs.

The country's native biologics sector is second after the USA. Coupled with the government's focus on supporting lower-cost copycat products, this entails a massive opportunity for bio-similars. While innovative drugmakers long benefited from generous exclusivity periods in Japan, the country is catching up with other mature markets regarding generics penetration.

The confidence in the system is reflected by the fact that domestic drugmakers are increasingly going global with their products. With the share of top Japanese companies' overseas sales rising steadily, the demand for cold chain storage and transportation facilities is also increasing. Another critical factor for increased interest in Japan's pharmaceuticals sector is the need to enhance Japan's drug discovery ecosystem.

The increased COVID-19 infection cases in the country increased the demand for prescription drugs and vaccines. It impacted the pharmaceutical product demand. The increasing import of COVID-19 vaccines increased the pharmaceutical product demand. For instance, in May 2021, the Japanese government signed a contract with Pfizer-BioNTech to import 194 million (USD 1.33 million)vaccine doses by the end of 2021. In 2021, the Japanese prescription drug market was valued at approximately JPY 10.6 trillion (USD 0.080 Trillion), up from about JPY 10.4 trillion (USD 0.079 Trillion) in 2020, according to IQVIA.

Japan Cold Chain Logistics Industry Overview

The market is relatively fragmented, with many local and international players, including Nippon Express, Yamato, Sagawa Express Co., Ltd, Itochu Logistics Corp., and Kintetsu World Express. The competition in the market pertains to costs, storage fees, and space, along with the rising prices of packing and packaging materials. The service providers are still working on developing the ability to provide standardization in the processes. Lack of standardization related to storage temperature and operating procedures are a few more significant challenges the industry faces. The quality and flexibility of available cold warehousing space are a considerable concern.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Criticality of the healthcare sector

- 4.2.1.2 Increased consumer demand for fresh foods

- 4.2.2 Restraints

- 4.2.2.1 Inadequate packaging or damaged products

- 4.2.2.2 Disrupted temperature control

- 4.2.3 Opportunities

- 4.2.3.1 Technological Innovations

- 4.2.1 Drivers

- 4.3 Technological Trends and Automation

- 4.4 Government Regulations and Initiatives

- 4.5 Industry Value Chain/Supply Chain Analysis

- 4.6 Spotlight on Ambient/Temperature-controlled Storage

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Emission Standards and Regulations on Cold Chain Industry

- 4.9 Impact of COVID - 19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Services

- 5.1.1 Storage

- 5.1.2 Transportation

- 5.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

- 5.2 By Temperature Type

- 5.2.1 Chilled

- 5.2.2 Frozen

- 5.3 By Application

- 5.3.1 Horticulture (Fresh Fruits & Vegetables)

- 5.3.2 Dairy Products (Milk, Ice-cream, Butter, etc.)

- 5.3.3 Meats, Fish, Poultry

- 5.3.4 Processed Food Products

- 5.3.5 Pharma, Life Sciences, and Chemicals

- 5.3.6 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Nippon Express

- 6.2.2 Yamato Holdings

- 6.2.3 Sagawa

- 6.2.4 Kintetsu World Express

- 6.2.5 Itochu Logistics Corp.

- 6.2.6 DHL

- 6.2.7 Kuehne Nagel

- 6.2.8 K line Logistics

- 6.2.9 Nichirei Logistics Group, Inc.

- 6.2.10 Sojitz Corporation

- 6.2.11 CEVA Logistics

- 6.2.12 Kokubu Goup

- 6.2.13 Agility

- 6.2.14 SF Express*

7 FUTURE OF JAPAN COLD CHAIN LOGISTICS MARKET

8 APPENDIX

醫藥品低溫物流輸送系統市場:各一次包裝形式,各二次包裝形式,使用法類別,各主要地區:2035年前的產業趨勢與全球預測

醫藥品低溫物流輸送系統市場:各一次包裝形式,各二次包裝形式,使用法類別,各主要地區:2035年前的產業趨勢與全球預測 東協低溫運輸物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

東協低溫運輸物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 冷鏈物流市場機會、成長動力、產業趨勢分析及2025-2034年預測

冷鏈物流市場機會、成長動力、產業趨勢分析及2025-2034年預測 全球食品飲料低溫運輸物流市場(2025-2029)低溫運輸物流的日本市場評估:各類型,溫度,冷藏,各用途,各地區,機會,預測(2018年度~2032年度)

全球食品飲料低溫運輸物流市場(2025-2029)低溫運輸物流的日本市場評估:各類型,溫度,冷藏,各用途,各地區,機會,預測(2018年度~2032年度) 低溫運輸,全球市場 2025-2029

低溫運輸,全球市場 2025-2029 全球製藥業低溫運輸物流市場(2025-2029)冷凍食品物流:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)德國低溫運輸物流:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)義大利低溫運輸物流:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)

全球製藥業低溫運輸物流市場(2025-2029)冷凍食品物流:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)德國低溫運輸物流:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)義大利低溫運輸物流:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)