|

市場調查報告書

商品編碼

1644335

德國低溫運輸物流:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)Germany Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

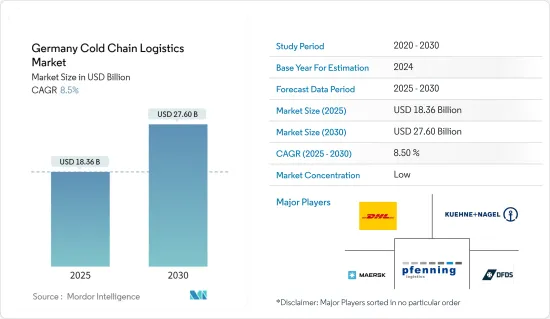

2025年德國低溫運輸物流市場規模預估為183.6億美元,預估至2030年將達276億美元,預測期間(2025-2030年)複合年成長率為8.5%。

低溫運輸的需求受到有組織的食品零售業的擴張、加工食品的需求以及醫療保健成本的上升所推動。德國低溫運輸物流市場受到電子商務在物流行業的滲透、冷藏倉庫的增加以及醫藥市場的擴大等因素的推動。

基礎設施薄弱、缺乏標準化、物流成本高以及製造商和零售商對物流服務的控制力不足等因素阻礙了德國低溫運輸物流市場的成長。然而,由於低溫運輸物流中採用多模態系統和 RFID 技術,IT 解決方案和自動化軟體的使用越來越多,並且成本降低和前置作業時間縮短,預計將為德國低溫運輸低溫運輸市場的成長提供豐厚的機會。

德國以其強大的食品工業而聞名,生產和出口各種生鮮產品,包括乳製品、肉類、水果和蔬菜。低溫運輸物流市場對於維持這些產品在供應鏈中流通時的新鮮度和品質至關重要。

德國低溫運輸物流市場趨勢

隨著製藥業的發展,冷藏倉庫的數量也增加

作為歐盟成員國,德國對藥品的運輸和儲存有嚴格的監管標準。遵守良好分銷規範(GDP)等法規至關重要,這推動了對專業低溫運輸物流服務的需求,以維護整個供應鏈中的產品完整性和安全性。先進生技藥品、疫苗和其他溫度敏感藥物的興起推動了對可靠的低溫運輸物流解決方案的需求,以確保這些治療的有效性和穩定性。製藥業向個人化醫療和生物製藥的轉變進一步凸顯了溫控運輸和儲存設施的重要性。

該公司正在對其低溫運輸業務進行數百萬美元的重大投資,以確保流程高效、可靠和安全。這一關注至關重要,因為端對端低溫運輸安全是該系統的一個薄弱方面。此外,溫控藥品和醫療設備的物流在醫療保健物流領域也呈現顯著成長。此外,複雜生技藥品的出現以及需要精確低溫運輸管理的荷爾蒙療法、疫苗和複雜蛋白質的運輸,推動了對溫控運輸和儲存設施的需求。此外,旨在維護貨物完整性的高品質低溫運輸物流服務的需求不斷成長也在推動市場擴張。

冷凍食品需求不斷增加

德國佔據歐洲冷凍食品市場的最大佔有率,因為德國人偏好風味高、品質高和獨特的食品,同時他們也優先避免過量攝取。中國蓬勃發展的消費經濟和豐富的自然資源為低溫運輸物流領域提供了龐大的商機。對生鮮食品、肉類、水產品和藥品的需求不斷成長,刺激了德國低溫運輸物流市場的擴張。此外,消費者逐漸從動物性食品轉向植物性食品,這推動了冷凍蔬菜市場的成長。此外,人們越來越認知到冷凍蔬菜比購買後冷藏的新鮮蔬菜保留了更多的維生素和營養。這種心態促使年輕消費者選擇冷凍蔬菜。

影響現代家庭財務狀況的多種因素推動了冷藏和冷凍食品的需求不斷成長,其中包括老年人變得更加獨立、雙收入家庭的數量不斷增加以及單人家庭的數量不斷增加。此外,對食品浪費和食品飲料行業勞動力短缺的擔憂也助長了這一趨勢。根據德國冷凍食品協會的資料,上年度德國人均冷凍食品消費量為46.1公斤。

德國低溫運輸物流產業概況

德國的低溫運輸物流市場較為分散,由大量本地公司組成,以滿足不斷成長的需求。電子商務物流領域的市場競爭日益激烈。預計國際和國內市場農產品出口的成長將吸引許多國際倉儲參與企業。市場的主要企業包括 Kuehne+Nagel International AG、DHL Group、A.P. Moller-Maersk A/S、Pfenning Logistics 和 Eurofresh Logistics GmbH。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章 簡介

- 研究假設和市場定義

- 研究範圍

第2章調查方法

- 研究框架

- 二次調查

- 初步調查

- 資料三角測量與洞察生成

- 計劃流程和結構

- 參與框架

第3章執行摘要

第4章 市場洞察

- 當前市場狀況

- 科技趨勢

- 政府法規和舉措

- 環境和溫度控制儲存亮點

- 產業價值鏈/供應鏈分析

- 排放標準和法規對低溫運輸產業的影響

- COVID-19 對市場的影響

第5章 市場動態

- 市場促進因素

- 新鮮農產品需求不斷增加

- 製藥業的成長

- 市場限制

- 初期投資成本高

- 勞動力短缺和技能差距

- 市場機會

- 缺乏足夠的基礎設施

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 購買者/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭強度

第6章 市場細分

- 按服務

- 貯存

- 運輸

- 附加價值服務(冷凍、標籤、庫存管理等)

- 按溫度類型

- 常溫

- 冷藏

- 冷凍

- 按應用

- 園藝(新鮮水果和蔬菜)

- 乳製品(牛奶、冰淇淋、奶油等)

- 肉類和魚貝類

- 加工食品

- 製藥、生命科學、化學品

- 其他

第7章 競爭格局

- 市場集中度概覽

- 公司簡介

- Kuehne+Nagel International AG

- DHL Group

- AP Moller-Maersk A/S

- Pfenning Logistics

- Eurofresh Logistics GmbH

- Heuer Logistics GmbH & Co. KG

- KLM Kuhl-und Lagerhaus Munsterland GmbH

- Kloosterboer BLG Coldstore GmbH

- Frigolanda Cold Logistics

- NewCold Advanced Logistics

- Scan Global Logistics*

- 其他公司

第 8 章:未來趨勢

第 9 章 附錄

The Germany Cold Chain Logistics Market size is estimated at USD 18.36 billion in 2025, and is expected to reach USD 27.60 billion by 2030, at a CAGR of 8.5% during the forecast period (2025-2030).

The demand for cold chains stems from the expansion of the organized food retail industry, the demand for processed food, and rising healthcare costs. The German cold chain logistics market is driven by factors such as the growing penetration of e-commerce in the logistics industry, the increasing number of refrigerated warehouses, and the expanding pharmaceutical market.

Poor infrastructure, a lack of standardization, higher logistics costs, and a lack of control by manufacturers and retailers over logistics services impede the growth of the German cold chain logistics market. However, the increasing use of IT solutions and automated software for cold chain logistics, as well as cost savings and reduced lead times as a result of the adoption of multi-modal systems and RFID technologies for cold chain applications, are expected to provide lucrative opportunities for the growth of the German cold chain logistics market.

Germany is well-known for its robust food industry, which produces and exports a diverse range of perishable goods, including dairy products, meat, fruits, and vegetables. The cold chain logistics market is critical in maintaining the freshness and quality of these products as they travel through the supply chain.

Germany Cold Chain Logistics Market Trends

The Number of Refrigerated Warehouses is Rising, Along With the Growing Pharmaceutical Industry

As part of the European Union, Germany upholds rigorous regulatory standards for the transportation and storage of pharmaceutical products. Adherence to regulations like Good Distribution Practice (GDP) is vital, driving the need for specialized cold chain logistics services to preserve product integrity and safety across the supply chain. The rise of advanced biologics, vaccines, and other temperature-sensitive medications has heightened the need for reliable cold-chain logistics solutions to safeguard the effectiveness and stability of these treatments. The pharmaceutical sector's pivot toward personalized medicine and biopharmaceuticals further underscores the significance of temperature-controlled transportation and storage facilities.

Companies are making substantial investments in their cold chain operations, amounting to millions of dollars, to establish efficient, reliable, and secure processes. This focus is crucial as end-to-end cold chain security represents a vulnerable aspect of the system. Moreover, the logistics of pharmaceutical products and medical devices under controlled temperatures is experiencing significant growth within the healthcare logistics sector. Additionally, the emergence of intricate biological-based medicines and the transportation of hormone treatments, vaccines, and complex proteins, which demand precise cold chain management, is driving the need for temperature-controlled transportation and storage facilities. The market is also expanding due to the increasing demand for high-quality cold chain logistics services aimed at preserving the integrity of goods.

The Demand for Frozen Foods is Increasing

Germany commands the largest share of the frozen food market in Europe, driven by a preference for high-flavor, high-quality, and distinctive foods among Germans, who also prioritize avoiding excessive calorie intake. The country's thriving consumer economy and abundant natural resources have created significant opportunities in the cold chain logistics sector. The escalating demand for perishable foods, meat, seafood, and pharmaceutical products has fueled the expansion of the cold chain logistics market in Germany. Additionally, there is a notable shift among consumers from animal-based foods to plant-based alternatives, propelling growth in the frozen vegetable market. Moreover, there is a growing awareness that frozen vegetables retain more vitamins and nutrients compared to fresh ones that are refrigerated after purchase. This awareness is gaining traction, driving younger consumers to opt for frozen vegetables.

The rising demand for chilled and frozen foods stems from various factors impacting modern households, including independent elderly individuals, the rise in dual-income households, and the growing number of single-person households. Additionally, concerns about food waste and labor shortages in the food and beverage industry contribute to this trend. According to data from the German Frozen Food Institute, per capita consumption of frozen foods was 46.1 kilograms in the previous year.

Germany Cold Chain Logistics Industry Overview

The German cold chain logistics market is fragmented and consists of a large number of local players that cater to the growing demand. The market is witnessing increasingly fierce competition in the field of e-commerce logistics. The growth in agricultural product exports in the international and domestic markets is expected to attract many international players in the warehousing and storage fields. Some of the major players in the market include Kuehne + Nagel International AG, DHL Group, A.P. Moller-Maersk A/S, Pfenning Logistics, and Eurofresh Logistics GmbH.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Data Triangulation and Insight Generation

- 2.5 Project Process and Structure

- 2.6 Engagement Frameworks

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Government Regulations and Initiatives

- 4.4 Spotlight on Ambient/Temperature-controlled Storage

- 4.5 Industry Value Chain/Supply Chain Analysis

- 4.6 Impact of Emission Standards and Regulations on Cold Chain Industry

- 4.7 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand for Perishable Products

- 5.1.2 Growth of Pharmaceutical Products

- 5.2 Market Restraints

- 5.2.1 High Initial Investment Costs

- 5.2.2 Labor Shortages and Skills Gap

- 5.3 Market Opportunities

- 5.3.1 Lack of Adequate Infrastructure

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Threat of New Entrants

- 5.4.2 Bargaining Power of Buyers/Consumers

- 5.4.3 Bargaining Power of Suppliers

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Services

- 6.1.1 Storage

- 6.1.2 Transportation

- 6.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

- 6.2 By Temperature Type

- 6.2.1 Ambient

- 6.2.2 Chilled

- 6.2.3 Frozen

- 6.3 By Application

- 6.3.1 Horticulture (Fresh Fruits and Vegetables)

- 6.3.2 Dairy Products (Milk, Ice-cream, Butter, etc.)

- 6.3.3 Meat and Seafood

- 6.3.4 Processed Food Products

- 6.3.5 Pharmaceuticals, Life Sciences, and Chemicals

- 6.3.6 Other Applications

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration Overview

- 7.2 Company Profiles

- 7.2.1 Kuehne + Nagel International AG

- 7.2.2 DHL Group

- 7.2.3 A.P. Moller-Maersk A/S

- 7.2.4 Pfenning Logistics

- 7.2.5 Eurofresh Logistics GmbH

- 7.2.6 Heuer Logistics GmbH & Co. KG

- 7.2.7 KLM Kuhl- und Lagerhaus Munsterland GmbH

- 7.2.8 Kloosterboer BLG Coldstore GmbH

- 7.2.9 Frigolanda Cold Logistics

- 7.2.10 NewCold Advanced Logistics

- 7.2.11 Scan Global Logistics*

- 7.3 Other Companies

8 FUTURE TRENDS

9 APPENDIX

醫藥品低溫物流輸送系統市場:各一次包裝形式,各二次包裝形式,使用法類別,各主要地區:2035年前的產業趨勢與全球預測

醫藥品低溫物流輸送系統市場:各一次包裝形式,各二次包裝形式,使用法類別,各主要地區:2035年前的產業趨勢與全球預測 東協低溫運輸物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

東協低溫運輸物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 冷鏈物流市場機會、成長動力、產業趨勢分析及2025-2034年預測

冷鏈物流市場機會、成長動力、產業趨勢分析及2025-2034年預測 全球食品飲料低溫運輸物流市場(2025-2029)低溫運輸物流的日本市場評估:各類型,溫度,冷藏,各用途,各地區,機會,預測(2018年度~2032年度)

全球食品飲料低溫運輸物流市場(2025-2029)低溫運輸物流的日本市場評估:各類型,溫度,冷藏,各用途,各地區,機會,預測(2018年度~2032年度) 低溫運輸,全球市場 2025-2029

低溫運輸,全球市場 2025-2029 全球製藥業低溫運輸物流市場(2025-2029)冷凍食品物流:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)日本低溫運輸物流-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)義大利低溫運輸物流:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)

全球製藥業低溫運輸物流市場(2025-2029)冷凍食品物流:市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)日本低溫運輸物流-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)義大利低溫運輸物流:市場佔有率分析、產業趨勢與成長預測(2025-2030 年)