|

市場調查報告書

商品編碼

1683938

歐洲戶外 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Europe Outdoor LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

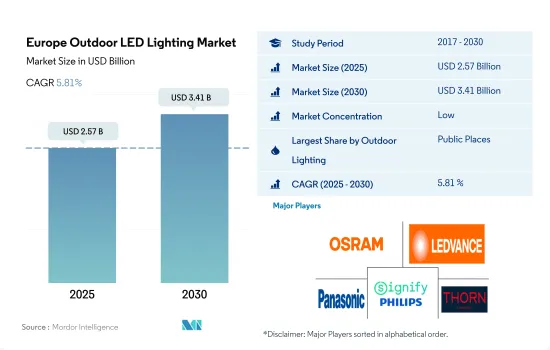

預計 2025 年歐洲戶外 LED 照明市場規模為 25.7 億美元,到 2030 年將達到 34.1 億美元,預測期內(2025-2030 年)的複合年成長率為 5.81%。

遊樂園和停車場擴大使用 LED 照明,以及政府禁止使用傳統燈具的規定將推動 LED 照明市場的成長

- 從金額和數量來看,2023 年公共空間將佔最大佔有率,其次是道路和小徑。為了遏制新冠肺炎疫情的蔓延,全部區域的體育場、游泳池、海灘和堡壘等公共場所都已關閉。歐洲在2021年放寬了與COVID相關的規定,隨著大樓的開放,LED照明市場也穩定成長。德國 Funtasy World Rodental 和俄羅斯普希金主題樂園等新遊樂園預計將於 2023 年開放。這些發展預計將對 LED 照明市場產生正面影響。

- 該地區零售業的出現也增加了停車需求。例如,IKEA斥資3.78億英鎊收購了牛津街上的前Topshop旗艦店。宜家計劃於 2023 年在該大樓開設第一家商店,專營燈具和窗簾等家居用品。預計此類市場趨勢將導致該地區對 LED 零售照明產品的需求增加。這些發展可能包括更多的公共空間,例如專用停車場和增加使用 LED 照明。

- 推動歐洲LED產品需求的主要因素是歐盟禁止銷售低效率照明技術的政策。 2009年,歐洲開始逐步淘汰白熾燈的使用。定向鹵素燈也於2016年逐步淘汰。 2018年9月,該地區禁止販售非定向鹵素燈。這些政策鼓勵消費者逐步以LED技術為基礎的產品取代傳統照明產品。

體育場館升級維修、鐵路基礎設施增加以及街道照明的使用將推動 LED 照明市場成長

- 就金額和數量而言,其他歐洲國家將在 2023 年佔據最大佔有率,其次是英國、法國和德國。未來幾年,其他歐洲國家的市場佔有率預計將略有下降,而其餘國家的市場佔有率預計將增加。

- 西班牙、巴塞隆納和瓦倫西亞等國家正在建造新的體育場並維修歷史建築。例如,巴塞隆納已從多位投資者那裡獲得了 14.5 億歐元(16 億美元)的資金,將於 2023 年開始建造諾坎普球場。布魯塞爾計劃在 2022 年投資 600 萬歐元(650 萬美元)。未來計劃在歐洲舉行的體育賽事包括 2024 年歐洲盃和 2025 年歐洲籃球錦標賽。因此,由於新體育場館的維修和建設以及體育賽事的增加,該國的 LED 照明銷售額預計將增加。

- 智慧建築計劃和 LED 平均價格的下降也是 LED 需求的主要驅動力。德國城市已開始測試將 LED 用於建築和街道照明。烏克蘭政府2023年6月計畫的新階段是更換舊燈泡。自2023年1月該計畫啟動以來,數百萬烏克蘭人利用機會免費獲得了現代燈泡。此外,出於各種社會、經濟和流動性相關的原因,對道路網路基礎設施的投資非常重要。平均而言,大多數歐洲國家每年將其 GDP 的 0.8% 至 1.2% 左右用於公路網建設。例如,2015年,奧地利實施了奧地利高速公路網投資計畫。

歐洲戶外 LED 照明市場趨勢

體育場館升級、更換和新建推動 LED 照明成長

- 預計體育場數量將從 2022 年的 1,700 個成長到 2029 年的 1,760 個,複合年成長率為 0.5%。近年來,體育領域發生了許多變化。例如,倫敦體育場和 Musco 於 2020 年合作升級其照明系統,引入 LED 照明。到 2020 年,都柏林的阿維瓦體育場將獲得令人讚嘆的照明昇級。紅色、綠色、藍色和白色 (RGBW) LED 燈具具有 52 種變色選項,構成了最近安裝的系統。瓦倫西亞城市體育場於 2020 年進行了維修,並增加了 LED 泛光燈。 2021年,歐洲六座體育場將配備由 Signify 提供技術支援的全新照明設備。這些因素正在支持該地區LED市場的擴張。

- 歐洲俱樂部已撥出超過 25 億歐元(26.9 億美元)用於維修其設施。西班牙的瓦倫西亞是第二昂貴的俱樂部,他們於 2022 年斥資 3 億歐元(3.2377 億美元)建造了諾梅斯塔利亞球場。塞爾維亞足球聯合會 (FSS) 在歐足總的支持下,已投資超過 2000 萬歐元(2158 萬美元)來維修該國的許多體育場,直至 2023 年。巴塞隆納已從多位投資者處獲得 14.5 億歐元(16 億美元)融資,諾坎普球場將於 2023 年開始興建。布魯塞爾已投資 600 萬歐元(647 萬美元)在 2022 年建造其主要體育場。 2024 年歐洲盃、2025 年歐洲籃球錦標賽和其他賽事是歐洲即將舉辦的一些體育賽事。因此,體育場館維修和新建以及體育賽事的增加預計將推動該國 LED 照明的銷售。

住宅和非住宅用途的增加可能推動 LED 照明的成長

- 2022年,歐洲人口為7.435億。歐盟成員國擁有超過1.31億棟建築。歐盟有1.19億棟住宅和1200萬座非住宅。 2022年,住宅需求依然強勁,鼓勵該地區住宅,並使當地的LED市場受益。

- 預計家庭數量將從 2020 年的 1.96 億增加到 2021 年的 1.974 億。在歐盟,2021 年 49.4% 的家庭有一個孩子,其次是 38.6% 有兩個孩子,12% 有三個或三個以上的孩子。 2020年,約70%的歐盟公民擁有自己的住房。 2019年,歐洲平均每人擁有1.6個房間。隨著人口和家庭數量的增加,家庭和商業空間中 LED 的使用可能會增加。

- 截至2019年,歐盟道路上共有2.427億輛汽車,比與前一年同期比較成長1.8%,其中包括2800萬多輛貨車。目前,法國是持有數量最多的國家,擁有 600 萬輛,其次是義大利(420 萬輛)、西班牙(380 萬輛)和德國(280 萬輛)。歐盟道路上有620萬輛中型和重型商用車。儘管近期註冊量增加,但歐盟所有車輛中只有 4.6% 採用替代能源。混合動力電動車佔歐盟道路上所有車輛的 0.8%,而電池電動車和插電式混合動力車僅佔 0.2%。汽車銷量的成長可能會對該地區的 LED 銷售產生積極影響。

歐洲戶外 LED 照明產業概況

歐洲戶外LED照明市場較為分散,前五大企業佔比為39.24%。該市場的主要企業是:ams-OSRAM AG、LEDVANCE GmbH(MLS)、松下控股公司、Signify Holding(飛利浦)和Thorn Lighting Ltd.(Zumtobel Group)(按字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章執行摘要和主要發現

第2章 報告要約

第 3 章 簡介

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 人口

- 人均收入

- LED進口總量

- 照明耗電量

- 家庭數量

- LED滲透率

- 體育場數量

- 法律規範

- 法國

- 德國

- 英國

- 價值鏈與通路分析

第5章 市場區隔

- 戶外照明

- 公共設施

- 道路照明

- 其他

- 國家

- 法國

- 德國

- 英國

- 其他歐洲國家

第6章 競爭格局

- 主要策略趨勢

- 市場佔有率分析

- 業務狀況

- 公司簡介(包括全球概況、市場層級概況、主要業務部門、財務狀況、員工人數、關鍵資訊、市場排名、市場佔有率、產品和服務、最新發展分析)

- ACUITY BRANDS, INC.

- ams-OSRAM AG

- Dialight PLC

- EGLO Leuchten GmbH

- LEDVANCE GmbH(MLS Co Ltd)

- Panasonic Holdings Corporation

- Signify Holding(Philips)

- Thorlux Lighting(FW Thorpe Plc)

- Thorn Lighting Ltd.(Zumtobel Group)

- TRILUX GmbH & Co. KG

第7章:執行長的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源和進一步閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

The Europe Outdoor LED Lighting Market size is estimated at 2.57 billion USD in 2025, and is expected to reach 3.41 billion USD by 2030, growing at a CAGR of 5.81% during the forecast period (2025-2030).

Increasing use of LED lighting in amusement parks and parking lots and government regulations to ban traditional lamps will drive the growth of the LED lighting market

- In terms of value and volume, public spaces will account for the largest share in 2023, followed by roads and trails. Public places such as stadiums, pools, beaches, and forts were closed across the region to contain the spread of COVID-19. Europe relaxed the COVID-related rules in 2021. With the opening of buildings, the LED lighting market is also growing steadily. New amusement parks, such as Funtasy World Rodental in Germany and Pushkin Theme Park in Russia, will open in 2023. These developments will have a positive impact on the LED lighting market.

- With the emergence of retail outlets in the area, the demand for parking has increased. For example, IKEA bought the former Topshop flagship store on Oxford Street for GBP 378 million. IKEA plans to open its first store in the same building in 2023, specializing in household items such as lamps and curtains. Such instances in the market are expected to lead to increased demand for LED retail lighting products in the region. These developments will increase the number of public spaces, such as private parking spaces, and the use of LED lighting.

- A major factor driving the demand for LED products in Europe is the European Union's policy of banning the sale of inefficient lighting technologies. In 2009, Europe phased out the use of incandescent light bulbs. Directional halogen lamps were also discontinued in 2016. In September 2018, the region banned the sale of non-directional halogen lamps. These policies have facilitated the gradual replacement of traditional lighting products by consumers with those based on LED technology.

Upgradation and renovation of stadiums, rising rail infrastructure, and use of street lights to drive the growth of the LED lighting market

- In terms of value and volume, the Rest of Europe occupied a major share in 2023, followed by the United Kingdom, France, and Germany. The market share is expected to be a small reduction in the Rest of Europe and gain in other remaining countries in coming years.

- Countries such as Spain, Barcelona, and Valencia are working to develop new stadiums and refurbish historical buildings in their countries. For example, Barcelona has secured EUR 1.45 billion (USD 1.6 billion) from multiple investors to begin construction of its Camp Nou stadium in 2023. Brussels planned to invest EUR 6 million (USD 6.5 million) in 2022. UEFA Euro 2024, EuroBasket 2025, and other events are some of the upcoming sporting events in Europe. Therefore, the renovation and construction of new stadiums and the increase in sports tournaments are expected to boost sales of LED lighting in the country.

- The smart building initiatives and falling average LED prices are also key drivers of LED demand. LEDs for building and street lighting have already been tested in German cities. In June 2023, a new phase of the Ukrainian government's program planned to replace old light bulbs. Since the program was launched in January 2023, millions of Ukrainian citizens have taken advantage of the opportunity to receive the latest light bulbs for free. In addition, investments in road network infrastructure are important for a variety of social, economic, and mobility-related reasons. On average, most European countries spend about 0.8% to 1.2% of their annual GDP on road networks. For example, in 2015, Austria implemented a program of investment in the Austrian motorway network.

Europe Outdoor LED Lighting Market Trends

Upgradation, replacement, and construction of new stadiums will drive the growth of LED lights

- The number of stadiums is expected to witness growth from 1,700 units in 2022 to 1,760 units in 2029, exhibiting a CAGR of 0.5%. The sports sector has undergone several changes in recent years. For instance, London Stadium and Musco collaborated in 2020 to upgrade the lighting system and install LED lights. The Aviva Stadium in Dublin had spectacular lighting effects by 2020. Red, green, blue, and white (RGBW) LED fixtures with 52 color-changing options make up the recently installed system. The stadium at Ciutat de Valencia underwent renovation in 2020, and LED floodlights were added. Six stadiums in Europe got new lighting by Signify in 2021. These elements support the expansion of the LED market in the area.

- European clubs set aside more than EUR 2.5 billion (USD 2.69 billion) for facility renovations. Valencia, Spain, which committed EUR 300 million (USD 323.77 million) to constructing the Nou Mestalla stadium in 2022, made the second-most expensive investment. With UEFA's assistance, the Football Association of Serbia (FSS) invested more than EUR 20 million (USD 21.58 million) in 2023 to upgrade a number of the nation's stadiums. Barcelona obtained EUR 1.45 billion (USD 1.6 billion) in financing from several investors to start building the Camp Nou stadium in 2023. Brussels invested EUR 6 million (USD 6.47 million) in building a major stadium in 2022. UEFA Euro 2024, EuroBasket 2025, and other events are a few of the upcoming sporting occasions in Europe. Thus, the renovation and construction of new stadiums and an increase in sporting tournaments are expected to increase sales of LED lights in the country.

Increasing residential housing and non-residential buildings may drive the growth of LED lights

- In 2022, Europe had 743.5 million people. The Member States of the European Union contains over 131 million structures. The European Union has 119 million residential buildings and 12 million non-residential buildings. In 2022, the demand for housing remained high, encouraging the building of new homes in the region, thus benefitting the local LED market.

- There were 197.4 million households in 2021 as opposed to 196.0 million in 2020. In the EU, 49.4% of households had a single child in 2021, followed by 38.6% with two children and 12% with three or more. About 70% of EU citizens were homeowners in 2020. In 2019, European homes had 1.6 rooms per person on average. The use of LEDs in homes and business spaces may increase as the population and the number of households rise.

- As of 2019, there were 242.7 million cars on the road in the European Union, an increase of 1.8% from the previous year, and more than 28 million vans on the road. France has by far the largest fleet of vans, with six million vehicles, followed by Italy (4.2 million), Spain (3.8 million), and Germany (2.8 million). EU roadways have 6.2 million medium and heavy commercial vehicles. Even though registrations have gone up recently, only 4.6% of all EU vehicles are alternatively powered. Hybrid electric vehicles make up 0.8% of all vehicles on EU roads, while battery-electric and plug-in hybrid vehicles each account for only 0.2% of the total. The increase in automotive vehicle sales may positively impact LED sales in the region.

Europe Outdoor LED Lighting Industry Overview

The Europe Outdoor LED Lighting Market is fragmented, with the top five companies occupying 39.24%. The major players in this market are ams-OSRAM AG, LEDVANCE GmbH (MLS Co Ltd), Panasonic Holdings Corporation, Signify Holding (Philips) and Thorn Lighting Ltd. (Zumtobel Group) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Population

- 4.2 Per Capita Income

- 4.3 Total Import Of Leds

- 4.4 Lighting Electricity Consumption

- 4.5 # Of Households

- 4.6 Led Penetration

- 4.7 # Of Stadiums

- 4.8 Regulatory Framework

- 4.8.1 France

- 4.8.2 Germany

- 4.8.3 United Kingdom

- 4.9 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Outdoor Lighting

- 5.1.1 Public Places

- 5.1.2 Streets and Roadways

- 5.1.3 Others

- 5.2 Country

- 5.2.1 France

- 5.2.2 Germany

- 5.2.3 United Kingdom

- 5.2.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ACUITY BRANDS, INC.

- 6.4.2 ams-OSRAM AG

- 6.4.3 Dialight PLC

- 6.4.4 EGLO Leuchten GmbH

- 6.4.5 LEDVANCE GmbH (MLS Co Ltd)

- 6.4.6 Panasonic Holdings Corporation

- 6.4.7 Signify Holding (Philips)

- 6.4.8 Thorlux Lighting (FW Thorpe Plc)

- 6.4.9 Thorn Lighting Ltd. (Zumtobel Group)

- 6.4.10 TRILUX GmbH & Co. KG

7 KEY STRATEGIC QUESTIONS FOR LED CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

中國戶外 LED 照明:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)中東和非洲戶外 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)亞太戶外 LED 照明:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美戶外 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)南美戶外 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)印度戶外 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)德國戶外 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)戶外 LED 照明市場:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)日本戶外 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)法國戶外 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

中國戶外 LED 照明:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)中東和非洲戶外 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)亞太戶外 LED 照明:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美戶外 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)南美戶外 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)印度戶外 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)德國戶外 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)戶外 LED 照明市場:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)日本戶外 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)法國戶外 LED 照明:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)