|

市場調查報告書

商品編碼

1683988

歐洲殺菌劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)Europe Fungicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

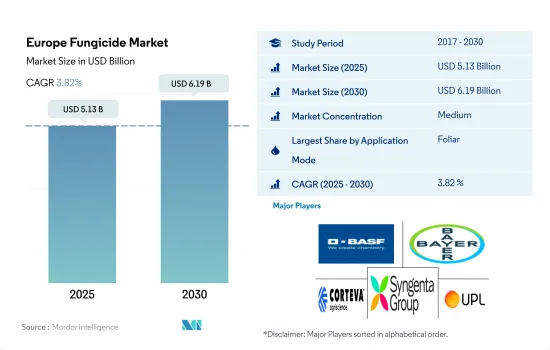

預計 2025 年歐洲殺菌劑市場規模將達到 51.3 億美元,預計到 2030 年將達到 61.9 億美元,預測期內(2025-2030 年)的複合年成長率為 3.82%。

對有效作物保護方法的需求正在刺激所有應用方法的市場成長。

- 在歐洲,我們看到採用不同施用方法的殺菌劑正在成長,以保護作物並確保高產量。其中,葉面噴布將佔據市場主導地位,2022 年市場規模將達到 28.2 億美元。這種方法通常用於水果、蔬菜和穀物等多種作物。歐洲農民越來越意識到使用葉面噴布保護作物免受真菌疾病侵害的好處,從而對葉面噴布的需求增加。

- 在 2023-2029 年預測期內,種子處理是歐洲殺菌劑市場成長最快的領域之一,預計複合年成長率為 3.6%。這種方法可以在發芽和早期生長階段提供對真菌病原體的早期保護,確保植物更健康。歐洲對精密農業的採用正在增加。種子處理適合精密農業策略,因為它可以有效使用殺菌劑,同時減少浪費。

- 預計 2023 年至 2029 年期間化學灌溉的複合年成長率為 3.4%。微灌溉的普及和滴灌面積的擴大正在推動這一領域的成長。

- 預測期內(2023-2029年),土壤處理市場價值預計將成長 9,090 萬美元。農民和農業相關人員對土壤健康的重要性及其對作物生產力的影響的認知不斷提高,這推動了對殺菌劑的需求。因此,預計預測期內(2023-2029 年)歐洲殺菌劑市場將以 3.7% 的複合年成長率成長。

西班牙主導歐洲殺菌劑市場

- 歐洲殺菌劑市場在歷史時期內經歷了穩定成長,預計2022年該地區將佔全球殺菌劑市場以金額為準的28.4%。Prothioconazole是該地區最常用的殺菌劑。

- 小麥是迄今為止歐洲最重要的作物。該地區是世界上最大的小麥生產地,2021年產量為1.39億噸。由於歐洲是最大的主糧出口國和生產國,殺菌劑主要用於該地區的穀物和穀類。 2022 年,穀物和穀類食品的市場佔有率以金額為準59.2%。

- 法國、義大利和西班牙的殺菌劑使用量佔歐洲殺菌劑總使用量的 64% 左右。以金額為準計算,2022 年西班牙佔最大佔有率,為 18.1%。這是因為這些國家在小麥和玉米等主要作物的生產上佔據主導地位。然而,葡萄晚疫病、早疫病、白粉病、鐮刀菌病、枯萎病和細菌性枯萎病等疾病是該地區常見的主要作物疾病。殺菌劑抗性的產生是一項重大挑戰,因為它縮小了有效管理疾病的殺菌劑選擇範圍。俄羅斯和荷蘭等政府正在投資研究舉措,以發現新的疾病和有效的殺菌劑來對抗這些疾病,並推出了支持農民的計劃。

- 政府的這些政策和農民日益增強的意識進一步鼓勵了作物保護措施的採用。預計這些因素將促進市場成長,預計預測期內(2023-2029 年)的複合年成長率將達到 3.7%。

歐洲殺菌劑市場趨勢

疾病傳播和作物損失增加導致殺菌劑消費量增加

- 在歐洲,由於作物病害造成的經濟損失不斷增加,殺菌劑的消耗量也增加。 2019 年至 2022 年,每公頃的消費量增加了 32.7%。由於氣候條件的變化、殺菌劑抗藥性的產生以及入侵真菌物種,該地區殺菌劑的使用量預計將增加。

- 影響穀物和穀類的真菌疾病包括銹病、白粉病、黑穗病和鐮刀菌核病。這些疾病對穀物和穀類構成重大威脅,並可能導致作物產量下降和品質下降。例如,小麥銹病會導致未經處理的易感小麥作物損失高達 100%。由於這些因素,歐洲廣泛使用殺菌劑來控制和管理這些疾病,並確保更高的產量和改善的作物品質。

- 義大利的殺菌劑消費量大幅增加。 2022年殺菌劑消費量比前一年增加了2,300克/公頃。這是由於作物病害發生率的增加、農業生產的擴大以及提高作物產量和品質的願望。

- 糧食生產對於維持未來人口的生存至關重要。可以透過增加土地用於農業並提高每公頃產量來提高糧食產量。提高每公頃產量的關鍵措施之一是使用植物保護產品。殺菌劑等產品有助於保護植物免受有害疾病的侵害。

- 因此,預計作物病害發生率將會增加,從而導致殺菌劑的消耗量增加,以保護作物並提高產量。

Tebuconazole與其他活性殺菌劑成分相比價格最高。

- Tebuconazole是一種三唑類殺菌劑,是一種以系統活性而聞名的活性成分,既能治療又能預防植物疾病。Tebuconazole用於幾種不同的常見殺菌劑產品中,可有效對抗真菌、細菌和病毒並保護植物。Tebuconazole的系統作用能阻止孢子的傳播並抑制其生長,使其成為一種流行的選擇,可以殺死影響葡萄、櫻桃、杏仁、穀物和菜籽等作物的有害真菌。 2022 年的價格為每噸 8,700 美元。

- Azoxystrobin是一種廣泛用於農業的殺菌劑,是抗菌頻譜最廣的殺菌劑。Azoxystrobin是一種強效活性成分,廣泛應用於多種作物,尤其是小麥種植。有效防治葉斑病、銹病、白粉病、霜霉病、網斑病、晚疫病等重要病害。尤其是德國,其大部分Azoxystrobin都是從印度進口的,2022 年市場價格將達到每噸 4,400 美元。

- Metalaxyl通常噴灑在馬鈴薯、葡萄等作物以及生菜、黃瓜等蔬菜上。Metalaxyl可有效防治馬鈴薯晚疫病、葡萄及蔬菜霜霉病等病害。Metalaxyl的使用將有助於控制這些真菌感染疾病,並有助於歐洲農業獲得更健康、更豐產的作物產量。 2018年至2022年,Metalaxyl價格明顯上漲,上漲了235.7美元/噸。目前價格為每公噸 4,400 美元。

歐洲殺菌劑產業概況

歐洲殺菌劑市場適度整合,前五大企業佔64.73%的市佔率。市場的主要企業有:BASF公司、拜耳公司、科迪華農業科技公司、先正達集團和聯合磷化有限公司。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 每公頃農藥消費量

- 活性成分價格分析

- 法律規範

- 法國

- 德國

- 義大利

- 荷蘭

- 俄羅斯

- 西班牙

- 烏克蘭

- 英國

- 價值鍊和通路分析

第5章 市場區隔

- 執行模式

- 化學灌溉

- 葉面噴布

- 燻蒸

- 種子處理

- 土壤處理

- 作物類型

- 經濟作物

- 水果和蔬菜

- 糧食

- 豆類和油籽

- 草坪和觀賞植物

- 原產地

- 法國

- 德國

- 義大利

- 荷蘭

- 俄羅斯

- 西班牙

- 烏克蘭

- 英國

- 歐洲其他地區

第6章 競爭格局

- 主要策略趨勢

- 市場佔有率分析

- 業務狀況

- 公司簡介(包括全球概況、市場層級概況、主要業務部門、財務狀況、員工人數、關鍵資訊、市場排名、市場佔有率、產品和服務、最新發展分析)

- ADAMA Agricultural Solutions Ltd.

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

- Wynca Group(Wynca Chemicals)

第7章:執行長的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 50001690

The Europe Fungicide Market size is estimated at 5.13 billion USD in 2025, and is expected to reach 6.19 billion USD by 2030, growing at a CAGR of 3.82% during the forecast period (2025-2030).

The need for effective methods for crop protection is fueling the market's growth in all application methods

- Europe is witnessing the growth of fungicides in various application modes to protect crops and ensure high yields. Among these modes, foliar application dominated the market, which accounted for USD 2.82 billion in 2022. This method is commonly used in various crops, including fruits, vegetables, and cereals. Farmers in Europe are increasingly recognizing the benefits of using foliar applications to protect their crops from fungal diseases, leading to higher demand for foliar methods.

- Seed treatment is expected to be one of the fastest-growing segments in the European fungicide market during the forecast period 2023-2029, registering a CAGR of 3.6%. This method provides early protection against fungal pathogens during germination and early growth stages, ensuring healthier plant establishment. The adoption of precision agriculture practices has increased in Europe. Seed treatment fits well into precision agriculture strategies, as it allows for the efficient use of fungicides while reducing wastage.

- The chemigation method is anticipated to register a CAGR of 3.4% during 2023-2029. The expansion of area under drip irrigation with the rising adoption of micro-irrigation is driving the growth of this segment.

- The market value of soil treatment is expected to increase by USD 90.9 million during the forecast period (2023-2029). The rising recognition among farmers and agricultural stakeholders regarding the significance of soil health and its influence on crop productivity is driving the demand for fungicides. Thus, the European fungicide market is expected to witness a CAGR of 3.7% during the forecast period (2023-2029).

Spain dominates the European fungicide market

- The fungicides market in Europe witnessed steady growth during the historical period, with the region occupying a share of 28.4% by value of the global fungicides market in 2022. Prothioconazole is the most commonly used fungicide in the region.

- Wheat is by far the most important crop throughout Europe. The region is the world's largest wheat producer and contributed 139 million metric tons in 2021. Fungicides are primarily used in grains and cereals in the region, as Europe is also the largest exporter and producer of staple grains. The grains and cereals segment occupied a market share of 59.2% by value in 2022.

- France, Italy, and Spain account for approximately 64% of the total use of fungicides in Europe. Spain held the largest share of 18.1% by value in 2022. This is due to the predominance of these countries in the production of major crops, such as wheat and corn. However, diseases like grape late blight, early blight, powdery mildew, downy mildew, Fusarium wilting, Septoria, and bacterial blight are the common diseases attacking major crops in the region. The occurrence of fungicide resistance presents a significant challenge as it limits fungicide choices for effective disease management. Governments of various countries, such as Russia and the Netherlands, are investing in research initiatives to discover new diseases and effective fungicides to combat them, along with launching supportive schemes for farmers.

- Such policies initiated by governments and a rise in awareness among farmers have further encouraged the adoption of crop protection practices. Such factors are expected to contribute to the market's growth, which is anticipated to record a CAGR of 3.7% during the forecast period (2023-2029).

Europe Fungicide Market Trends

The increasing disease infestation and rising crop losses are leading to an increase in the consumption of fungicides

- Europe is experiencing an increase in the consumption of fungicides due to the rising economic losses associated with crop diseases. The consumption increased by 32.7% per hectare in 2022 from 2019. Fungicide use in the region is predicted to increase because of changes in climatic conditions, the development of fungicide resistance, and invasive fungal species.

- The fungal diseases affecting grains and cereals include rust, powdery mildew, smut, and fusarium head blight. These diseases pose a substantial threat to grains and cereals, as they may result in yield losses and reduce the quality of the harvested crops. For instance, wheat rust may cause crop losses of up to 100% in untreated susceptible wheat. Due to these factors, fungicides are extensively used in Europe to control and manage these diseases, ensuring higher yields and better crop quality.

- The region has witnessed a significant increase in the consumption of fungicides in Italy. The consumption of fungicides increased by 2.3 thousand g/ha in 2022 from the previous year. It was because of the rising occurrence of crop diseases, the expansion of agricultural production, and the desire to enhance crop yields and quality.

- Food production is required to sustain the future population. Growth in food production may be achieved with the use of more farmland and an increase in yield per hectare. One of the important means to bring about high yields per hectare is the use of plant protection products because products such as fungicides help protect plants from harmful diseases.

- Therefore, due to the increasing occurrence of crop diseases and to protect and increase yields of the crops, the consumption of fungicides is expected to increase.

Tebuconazole holds the highest price compared to other active ingredients of fungicide

- Tebuconazole, part of the triazole fungicide family, is an active ingredient known for its systemic nature, providing both curative and preventive control over plant diseases. Tebuconazole is used in several different popular fungicide products to protect plants, effectively countering fungi, bacteria, and viruses. Tebuconazole's systemic approach hinders spore spread and curbing growth, making it a popular choice against harmful fungi affecting crops like grapes, cherries, almonds, cereals, canola, and other crops. Its value in 2022 stood at USD 8.7 thousand per metric ton.

- Azoxystrobin, a widely used fungicide in agriculture, has the broadest spectrum of activity as an antifungal agent. It serves as a potent active ingredient and is extensively utilized across various crops, with a significant focus on wheat farming. It effectively controls important diseases such as leaf spots, rusts, powdery mildew, downy mildew, net blotch, and blight. Notably, Germany imports most of its azoxystrobin from India, and its market value in 2022 amounted to USD 4.4 thousand per metric ton.

- Metalaxyl is commonly applied to crops such as potatoes, grapes, and vegetables like lettuce and cucumbers. Metalaxyl effectively controls diseases such as late blight in potatoes and downy mildew in grapes and vegetables. Its application helps manage these fungal infections, contributing to healthier and more productive crop yields in European agriculture. Between 2018 and 2022, the price of metalaxyl experienced a notable rise, with an increase of USD 235.7 per metric ton. Currently, it stands at USD 4.4 thousand per metric ton.

Europe Fungicide Industry Overview

The Europe Fungicide Market is moderately consolidated, with the top five companies occupying 64.73%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 France

- 4.3.2 Germany

- 4.3.3 Italy

- 4.3.4 Netherlands

- 4.3.5 Russia

- 4.3.6 Spain

- 4.3.7 Ukraine

- 4.3.8 United Kingdom

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Netherlands

- 5.3.5 Russia

- 5.3.6 Spain

- 5.3.7 Ukraine

- 5.3.8 United Kingdom

- 5.3.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 Nufarm Ltd

- 6.4.7 Sumitomo Chemical Co. Ltd

- 6.4.8 Syngenta Group

- 6.4.9 UPL Limited

- 6.4.10 Wynca Group (Wynca Chemicals)

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

中國殺菌劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)亞太殺菌劑:市場佔有率分析、產業趨勢與成長預測(2025-2030)北美殺菌劑:市場佔有率分析、產業趨勢與成長預測(2025-2030)南美殺菌劑:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)印尼殺菌劑:市場佔有率分析、產業趨勢與成長預測(2025-2030)印度殺菌劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)美國殺菌劑:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)越南殺菌劑市場:佔有率分析、產業趨勢與統計、成長預測(2025-2030)非洲殺菌劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)

中國殺菌劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)亞太殺菌劑:市場佔有率分析、產業趨勢與成長預測(2025-2030)北美殺菌劑:市場佔有率分析、產業趨勢與成長預測(2025-2030)南美殺菌劑:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)印尼殺菌劑:市場佔有率分析、產業趨勢與成長預測(2025-2030)印度殺菌劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)美國殺菌劑:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)越南殺菌劑市場:佔有率分析、產業趨勢與統計、成長預測(2025-2030)非洲殺菌劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年) 2025年全球三唑類殺菌劑市場報告

2025年全球三唑類殺菌劑市場報告

▼