|

市場調查報告書

商品編碼

1683990

印度殺菌劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)India Fungicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

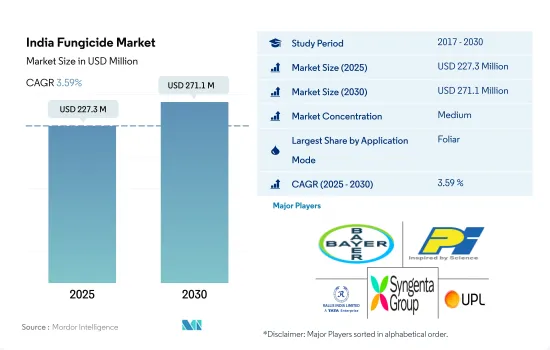

印度殺菌劑市場規模預計在 2025 年為 2.273 億美元,預計到 2030 年將達到 2.711 億美元,預測期內(2025-2030 年)的複合年成長率為 3.59%。

真菌疾病的增加增加了對各種施用方法的殺菌劑的需求。

- 根據具體要求和疾病,殺菌劑可以以多種方式使用。這些方法包括化學噴霧、葉面噴布、燻蒸以及種子和土壤處理。這些不同的施用方法對於根據條件將殺菌劑有效地應用於不同作物起著重要作用。

- 2022年,葉面噴布在殺菌劑應用領域佔據主導地位,佔據最大的市場佔有率,為60.9%。這種方法之所以受到高度青睞,是因為它透過直接針對葉子上的病原體,可以有效地預防葉面真菌疾病。葉面噴布可促進殺菌劑快速滲透和吸收到植物組織中,確保有效對抗真菌病原體。

- 殺菌劑種子處理被廣泛用於在植物發育早期對抗真菌感染。這些處理方法為種子周圍提供了保護屏障,有效地防止了種子腐爛、猝倒病、澇漬病和根腐病等多種疾病。在2022年的印度殺菌劑市場中,殺菌劑種子處理部分佔了13.8%的市場佔有率。

- 由於這些作物易受害蟲侵害,穀物和穀類生產商會根據作物階段和害蟲侵染情況採用各種噴灑方法。對於這些作物,主要採用葉面噴灑殺蟲劑的方法。

- 施用方法的選擇受多種因素的影響,包括特定的目標疾病、作物類型、疾病階段和設備的可用性。預計預測期內殺菌劑市場複合年成長率將達到 3.9%。

印度殺菌劑市場趨勢

氣候變遷和日益增加的疾病壓力可能會推動殺菌劑的消費

- 印度是作物保護化學品(包括殺菌劑)的重要消費國。該國農業部門規模龐大,種植的作物種類繁多,因此對殺菌劑的需求很高。真菌病害嚴重降低農產品的產量和品質,造成很大的損失。殺菌劑對於預防和控制各種疾病,維持農業生產的健康和生產力至關重要。 2022年,印度每公頃殺菌劑消費量為101.5公克/公頃。

- 印度的作物種類繁多,從水稻和小麥等主食作物到棉花、水果和蔬菜等經濟作物,因此引發的疾病種類繁多。銹病、枯萎病、霜霉病和腐爛病是真菌疾病對這些作物造成毀滅性影響的一些例子。為了減輕這些風險並保護作物,印度農民使用殺菌劑作為疾病管理策略的重要工具。

- 在印度,農業實踐的改變和糧食需求的增加導致耕地面積的增加。農民正在更頻繁地重複種植或逐年增加種植週期。作物集約化種植增加了疾病爆發的風險,包括真菌疾病,因此對殺菌劑的需求也增加了。 2017年至2022年期間,印度每公頃殺菌劑消費量增加了5.0%。

- 印度政府制定了多項計畫和方案來鼓勵使用殺菌劑等作物保護化學物質。各國政府透過補助、推廣服務和培訓計畫鼓勵農民使用殺菌劑進行病害防治。

氣候變遷會改變真菌的生存、傳染性和宿主的易感性,導致新疾病的出現。

- 真菌病害是重要作物的一大威脅。真菌病原體導致印度各種作物產量嚴重下降。在穀物中,它被認為是一個產量限制因素。印度因真菌感染造成的作物產量損失估計每年約 500 萬噸。

- 代森錳鋅是一種廣譜接觸性殺菌劑,用於防治玉米、稻米、小麥、蔬菜、水果、甘蔗、菸草等作物的冰斑病、環斑病、稻瘟病、瘡痂病、葉黴病、白粉病、莖腐病、莖腐病、褐腐病、白莖腐病、黑莖腐病等真菌病害。 2022 年其價格為每噸 7,700 美元。

- 丙森鋅是一種接觸性殺菌劑,2022 年的價格為每噸 3,500 美元。它用於防治蘋果、馬鈴薯、辣椒和番茄等作物的多種疾病,包括早晚疥瘡、七葉樹腐爛病、白粉病、果葉斑病和葉斑病。

- 福美鋅是一種基本的接觸性葉面殺菌劑,2022 年的價格為每噸 3,200 美元。主要防治馬鈴薯早疫病、晚疫病,攀緣植物和葫蘆科植物的霜霉病、黑腐病,蘋果的黑星病,香蕉的香蕉葉斑病,柑橘的黑腐病。

- 氣候變遷會影響真菌的生存、傳染性和宿主易感性,導致新疾病的出現。例如,印度半島西海岸、中部、內陸半島和東北部的氣候變暖趨勢為高粱霜霉病(SDM)和洋桔梗葉枯病(TLB)等玉米病害創造了有利條件。預計這些因素將影響殺菌劑的價格和需求。

印度殺菌劑產業概況

印度殺菌劑市場適度整合,前五大公司佔53.11%的市佔率。該市場的主要企業有:拜耳股份公司、PI Industries、Rallis India Ltd、先正達集團和UPL Limited(按字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 每公頃農藥消費量

- 活性成分價格分析

- 法律規範

- 印度

- 價值鍊和通路分析

第5章 市場區隔

- 執行模式

- 化學灌溉

- 葉面噴布

- 燻蒸

- 種子處理

- 土壤處理

- 作物類型

- 經濟作物

- 水果和蔬菜

- 糧食

- 豆類和油籽

- 草坪和觀賞植物

第6章 競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介(包括全球概況、市場層級概況、主要業務部門、財務狀況、員工人數、關鍵資訊、市場排名、市場佔有率、產品和服務、最新發展分析)

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- PI Industries

- Rallis India Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源和進一步閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 50001692

The India Fungicide Market size is estimated at 227.3 million USD in 2025, and is expected to reach 271.1 million USD by 2030, growing at a CAGR of 3.59% during the forecast period (2025-2030).

The rising fungal diseases are driving the demand for fungicides in various application methods

- Fungicides can be applied using a variety of methods, depending on the specific requirements and diseases. These methods include chemigation, foliar application, fumigation, and seed and soil treatments. These diverse application methods play a crucial role in effectively applying fungicides to various crops, depending on the conditions.

- In 2022, foliar application dominated the fungicide application segment, which held the largest market share of 60.9%. This method was highly preferred as it provides efficient protection against foliar fungal diseases by directly targeting pathogens on leaves. The foliar application facilitates swift penetration and absorption of fungicides into the plant tissues, ensuring their effective action against fungal pathogens.

- Fungicide seed treatments are extensively employed to combat fungal infections in the early stages of plant development. These treatments provide a protective barrier around the seeds, effectively preventing a range of diseases such as seed rots, seedling blights, damping off, and root rots. The fungicide seed treatments segment held a market share of 13.8% in the Indian fungicide market in 2022.

- Grains and cereal crop growers are majorly adopting all the application methods in their cultivation based on the crop stage and insect pests as these crops are more susceptible to insect pests. Foliar insecticide application was majorly adopted by the farmers in these crops.

- The selection of the application mode is influenced by various factors, including the specific target disease, crop type, disease stage, and the availability of equipment. The fungicide market is expected to register a CAGR of 3.9% during the forecast period.

India Fungicide Market Trends

The changing climate and rising disease pressure are expected to drive the consumption of fungicides

- India is a significant consumer of crop protection chemicals, including fungicides. The country's agricultural sector is large, with diverse types of crops being cultivated, leading to a substantial demand for fungicides. Fungal diseases can significantly reduce agricultural output and quality, resulting in considerable crop losses. Fungicides are essential in the prevention and management of various diseases, maintaining the health and productivity of agricultural production. In 2022, the consumption of fungicides in India per hectare accounted for 101.5 g/ha.

- India has a high crop diversity, ranging from staple food crops like rice and wheat to cash crops like cotton, fruits, and vegetables, creating a varied disease spectrum. Rust, blight, mildew, and rot are a few examples of the devastating effects of fungal diseases on these crops. To mitigate the risks and protect their crops, farmers in India rely on fungicides as an important tool in their disease management strategies.

- Crop intensity is rising in India because of changing agricultural practices and increased food demand. Farmers frequently engage in repeated cropping or increase the number of crop cycles every year. This intensification leads to a higher risk of disease outbreaks, including fungal diseases, and, consequently, a greater need for fungicides. The consumption of fungicides in India per hectare increased by 5.0% from 2017 to 2022.

- The Indian government has developed several plans and programs to encourage the use of crop protection chemicals such as fungicides. The government has pushed farmers to utilize fungicides for disease management through subsidies, extension services, and training programs.

Climatic changes altering fungal survivability and infectivity as well as host susceptibility, leading to new disease outbreaks

- Fungal diseases are a major threat to important crops. Fungal pathogens cause large yield losses in different crops in India. They are known to be yield-limiting factors in cereals. The fungal infections-related decline in crop yield in India is believed to be approximately 5.0 million tons per year.

- Mancozeb is a broad-spectrum contact fungicide used to control fungal diseases like eyespot, ringspot, blast, scab, leaf mold, powdery mildew, stem bois, stem rot, brown rot, white stem rot, and black stem rot in corn, rice, wheat, vegetables, fruit, sugarcane, and tobacco crops. It was valued at USD 7.7 thousand per metric ton in 2022.

- Propineb is a contact fungicide valued at USD 3.5 thousand per metric ton in 2022. It is used to control various diseases like scab early & late blight dieback, buckeye rot, downy mildew, fruit spots, and brown, narrow leaf spot diseases in apple, potato, chili, and tomato crops.

- Ziram is a basic contact foliar fungicide priced at USD 3.2 thousand per metric ton in 2022. It mainly controls early & late blight of potatoes/tomatoes, downy mildew and black rot of vines and cucurbits, scab of apples, Sigatoka of bananas, and melanose of citrus.

- Climatic changes can affect fungal survivability, infectivity, and host susceptibility, resulting in new disease outbreaks. For instance, the warming trend in climate along the Indian subcontinent's west coast, central, interior peninsula, and northeast regions creates favorable conditions for maize diseases like sorghum downy mildew (SDM) and turcicum leaf blight (TLB). These factors are expected to influence the prices and demand for fungicides.

India Fungicide Industry Overview

The India Fungicide Market is moderately consolidated, with the top five companies occupying 53.11%. The major players in this market are Bayer AG, PI Industries, Rallis India Ltd, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 India

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 PI Industries

- 6.4.7 Rallis India Ltd

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

中國殺菌劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)亞太殺菌劑:市場佔有率分析、產業趨勢與成長預測(2025-2030)北美殺菌劑:市場佔有率分析、產業趨勢與成長預測(2025-2030)南美殺菌劑:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)印尼殺菌劑:市場佔有率分析、產業趨勢與成長預測(2025-2030)歐洲殺菌劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)美國殺菌劑:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)越南殺菌劑市場:佔有率分析、產業趨勢與統計、成長預測(2025-2030)非洲殺菌劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)

中國殺菌劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)亞太殺菌劑:市場佔有率分析、產業趨勢與成長預測(2025-2030)北美殺菌劑:市場佔有率分析、產業趨勢與成長預測(2025-2030)南美殺菌劑:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)印尼殺菌劑:市場佔有率分析、產業趨勢與成長預測(2025-2030)歐洲殺菌劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)美國殺菌劑:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)越南殺菌劑市場:佔有率分析、產業趨勢與統計、成長預測(2025-2030)非洲殺菌劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年) 2025年全球三唑類殺菌劑市場報告

2025年全球三唑類殺菌劑市場報告

▼