|

市場調查報告書

商品編碼

1684003

美國殺菌劑:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)US Fungicide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

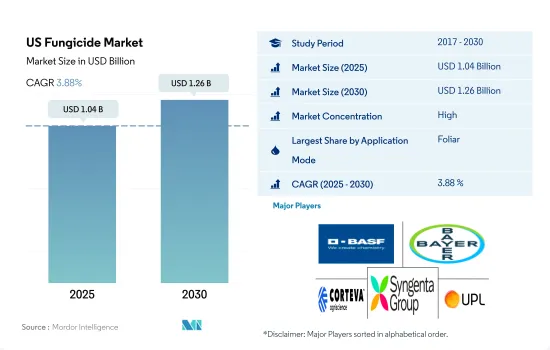

美國殺菌劑市場規模預計在 2025 年為 10.4 億美元,預計到 2030 年將達到 12.6 億美元,預測期內(2025-2030 年)的複合年成長率為 3.88%。

隨著農民採用不同的方法來保護作物免受真菌疾病的侵害,市場各個領域都在成長。

- 葉面噴布目前佔據美國殺菌劑市場的主導地位,預計從 2023 年到 2029 年,葉面噴霧的複合年成長率將達到 4.2%,是成長最快的噴霧類型。葉面噴布是將殺菌劑直接施用於植物的葉子上。此方法可以進行有針對性的局部治療,對控制作物葉片和莖部的真菌病害非常有效。葉面噴布之所以受歡迎,是因為它使用方便,且能快速控制疾病。

- 美國殺菌劑市場種子處理部分預計在預測期內(2023-2029 年)的複合年成長率將達到 4.1%,這得益於早期防治種子和土壤傳播疾病、提高發芽率和改善植物生長等多種因素。農民越來越意識到早期病害防治對於最佳化作物生長和產量的重要性。種子處理可以在作物生命週期早期開始進行有效的疾病管理。

- 2022 年化學灌溉產業的價值為 1.147 億美元。由於精確應用、勞動力成本降低以及整個田地殺菌劑分配更有效,該行業預計還將進一步成長。美國現代灌溉的普及率不斷提高也支持了這一領域的成長。

- 預計 2023 年至 2029 年期間美國殺菌劑市場的複合年成長率將達到 4.1%。隨著農民擴大採用不同的方法來保護作物免受真菌疾病的侵害,預計所有細分市場都將實現成長。

美國殺菌劑市場趨勢

害蟲侵擾加劇導致農藥消費增加

- 植物病害對產量和品質有重大影響。植物病原體每年造成約 210 億美元的農作物損失。預計這些因素將增加美國對殺菌劑的需求,以保護作物免受疾病侵害。

- 植物病害的發生和蔓延是農業生產的重要議題,對農業生產有重大影響。它們對糧食安全和經濟穩定構成威脅。 2021年,加州食品和農業部(CDFA)確認五個縣的2,510棵樹感染了柑橘黃龍病。為了應對這些疫情,農民擴大使用殺菌劑作為有效對抗植物疾病和減少其影響的手段。

- 2021年,植物病害導致美國玉米蒲式耳損失6.5%,高於2020年的整體損失3.9%,與2019年的整體損失6.8%更為接近。 2018年,美國玉米蒲式耳整體損失10.9%。此病害造成的損失增加,大部分是由於伊利諾州、印第安納州、密西根州和威斯康辛州爆發了焦油斑病。與 2018 年相比,2019 年和 2020 年疾病分佈和發病率的增加也導致該國殺菌劑消費量增加。

- 因此,由於植物病害發生率增加、作物產量下降以及新植物病原體的出現,美國殺菌劑市場預計將經歷顯著成長。隨著農民尋求有效的解決方案來對抗疾病、保護作物產量並應對新興植物病原體帶來的挑戰,對殺菌劑的需求可能會持續增加。

由於各種主要作物對Mancozeb的需求不斷增加以及國內產量的短缺,導致該國Mancozeb價格上漲。

- Mancozeb、丙森鋅和福美鋅是美國最常使用的殺菌劑成分。 2021年,大部分殺菌劑進口自印度、比利時和德國,成為全球第三大進口國。

- Mancozeb是一種廣譜接觸性殺菌劑,已在美國註冊,可用於多種水果、蔬菜、堅果和田間作物。預防多種真菌疾病,包括馬鈴薯枯萎病、葉斑病、瘡痂病和銹病。它還可以作為馬鈴薯、玉米、高粱、番茄和穀物等作物的種子處理劑。 2022 年的市場價值將達到每噸 7,800 美元。

- 丙森鋅是一種接觸性殺菌劑,2022 年的市場價值為每噸 3,500 美元。它的用途涵蓋治療多種疾病,包括影響蘋果、馬鈴薯、辣椒和番茄的瘡痂病、早疫病、晚疫病、枯萎病、七葉樹腐爛葉斑病、霜霉病、果葉斑病和褐斑病。

- 福美鋅是一種二硫代氨基甲酸類殺菌劑,註冊用於防治作物作物的真菌病害,包括核果、仁果、堅果、蔬菜和商業種植的觀賞植物。它用於防治蘋果和梨的黑星病、桃子的葉腐病和炭疽病以及番茄的早疫病。收穫前噴灑藥物也有助於防止水果在儲存和運輸過程中劣化。 2022 年的價格為每噸 3,300 美元。

美國殺菌劑產業概況

美國殺菌劑市場相當集中,前五大公司佔了75.73%的市場。市場的主要企業有:BASF公司、拜耳公司、科迪華農業科技公司、先正達集團和聯合磷化有限公司。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 每公頃農藥消費量

- 活性成分價格分析

- 法律規範

- 美國

- 價值鍊和通路分析

第5章市場區隔

- 執行模式

- 化學噴塗

- 葉面噴布

- 燻蒸

- 種子處理

- 土壤處理

- 作物類型

- 經濟作物

- 水果和蔬菜

- 糧食

- 豆類和油籽

- 草坪和觀賞植物

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 業務狀況

- 公司簡介(包括全球概況、市場層級概況、主要業務部門、財務狀況、員工人數、關鍵資訊、市場排名、市場佔有率、產品和服務、最新發展分析)

- ADAMA Agricultural Solutions Ltd.

- American Vanguard Corporation

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Nufarm Ltd

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 50001705

The US Fungicide Market size is estimated at 1.04 billion USD in 2025, and is expected to reach 1.26 billion USD by 2030, growing at a CAGR of 3.88% during the forecast period (2025-2030).

The market is experiencing growth in all segments as farmers are increasingly adopting different methods to protect crops from fungal diseases

- In the US fungicide market, foliar application currently holds the major share, and it is expected to record the fastest growth, with a CAGR of 4.2% during 2023-2029. Foliar application refers to the application of fungicides directly onto the foliage of plants. This method allows for targeted and localized treatment, making it highly effective in controlling fungal diseases on the leaves and stems of crops. The popularity of foliar application can be attributed to its ease of application and immediate impact on disease control.

- During the forecast period (2023-2029), the seed treatment segment is expected to register a CAGR of 4.1% in the US fungicide market, which can be attributed to various factors, including early protection against seed and soil-borne diseases, improved germination rates, and enhanced plant establishment. There is rising awareness among farmers about the importance of early disease control for optimal crop establishment and yield. Seed treatment allows for efficient disease management right at the beginning of the crop's life cycle.

- The chemigation segment was valued at USD 114.7 million in 2022. It is further estimated to grow due to its precise application, reduced labor costs, and increased efficiency in the distribution of fungicides throughout the field. The rising adaption of modern irrigation in the United States is also supporting the growth of the segment.

- The US fungicide market is anticipated to register a CAGR of 4.1% during 2023-2029. It is expected to witness growth in all segments as farmers are increasingly adopting different methods to protect their crops from fungal diseases.

US Fungicide Market Trends

The consumption of insecticides is being driven by the rising pest infestation

- Plant diseases have a significant impact on yields and quality. Crop losses due to plant pathogens are estimated at USD 21 billion per year. Due to these factors, the demand for fungicides in the United States is expected to increase to protect crops from diseases.

- The emergence and spread of plant disease outbreaks have become a growing concern, significantly impacting agricultural production. They are posing threats to both food security and economic stability. In 2021, the California Department of Food and Agriculture (CDFA) confirmed that 2,510 trees across five counties were infected by citrus greening disease. In response to such outbreaks, farmers have increasingly turned to the usage of fungicides as a means to effectively address plant diseases and mitigate their impact.

- Plant diseases reduced corn bushels by 6.5% across the United States in 2021, up from an overall 3.9% in 2020, corresponding more closely with the overall 6.8% loss experienced in 2019. In 2018, an overall 10.9% loss occurred in corn bushels in the United States. Most of this increase in disease loss was due to severe outbreaks of tar spots in Illinois, Indiana, Michigan, and Wisconsin. The increased distribution and incidence of diseases in 2019 and 2020 compared to 2018 also increased fungicide consumption in the country.

- Therefore, with the increasing incidence of plant diseases, the reduction in crop production, and the emergence of new plant pathogens, the US fungicide market is expected to witness significant growth. The demand for fungicides may continue to rise as farmers seek effective solutions to combat diseases, safeguard crop yields, and address the challenges posed by emerging plant pathogens.

The growing demand for mancozeb in various major crops and insufficient domestic production of it is raising the price of mancozeb in the country

- Mancozeb, propineb, and ziram are the most commonly used fungicide ingredients in the United States. In 2021, the country imported most of its fungicides from India, Belgium, and Germany, and it is the third-largest importer of fungicides worldwide.

- Mancozeb is a broad-spectrum contact fungicide that is labeled for use on many fruit, vegetable, nut, and field crops in the United States. It provides protection against a wide spectrum of fungal diseases, including potato blight, leaf spot, scab, and rust. It also serves as a seed treatment for crops such as potatoes, corn, sorghum, tomatoes, and cereal grains. In 2022, its market value reached USD 7.8 thousand per metric ton.

- Propineb, a contact fungicide, accounted for a market value of USD 3.5 thousand per metric ton in 2022. Its application extends to managing a range of diseases, including scab, early & late blight, dieback, buckeye rot, downy mildew, fruit spots, and brown, narrow-leaf spot diseases affecting apples, potatoes, chili, and tomatoes.

- Ziram is a fungicide belonging to the dimethyldithiocarbamate group, registered to control fungal diseases across a wide range of crops like stone fruits, pome fruits, nuts, vegetables, and commercially cultivated ornamental plants. Its applications comprise addressing issues like scabs in apples and pears, leaf curls in peaches, anthracnose, and early blight in tomatoes. It is used to prevent crop damage in the field and also applied prior to harvesting to prevent fruits from deterioration in storage or transport. Its price in 2022 accounted for USD 3.3 thousand per metric ton.

US Fungicide Industry Overview

The US Fungicide Market is fairly consolidated, with the top five companies occupying 75.73%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 United States

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Application Mode

- 5.1.1 Chemigation

- 5.1.2 Foliar

- 5.1.3 Fumigation

- 5.1.4 Seed Treatment

- 5.1.5 Soil Treatment

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd.

- 6.4.2 American Vanguard Corporation

- 6.4.3 BASF SE

- 6.4.4 Bayer AG

- 6.4.5 Corteva Agriscience

- 6.4.6 FMC Corporation

- 6.4.7 Nufarm Ltd

- 6.4.8 Sumitomo Chemical Co. Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

中國殺菌劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)亞太殺菌劑:市場佔有率分析、產業趨勢與成長預測(2025-2030)北美殺菌劑:市場佔有率分析、產業趨勢與成長預測(2025-2030)南美殺菌劑:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)印尼殺菌劑:市場佔有率分析、產業趨勢與成長預測(2025-2030)印度殺菌劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)歐洲殺菌劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)越南殺菌劑市場:佔有率分析、產業趨勢與統計、成長預測(2025-2030)非洲殺菌劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)

中國殺菌劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)亞太殺菌劑:市場佔有率分析、產業趨勢與成長預測(2025-2030)北美殺菌劑:市場佔有率分析、產業趨勢與成長預測(2025-2030)南美殺菌劑:市場佔有率分析、行業趨勢、統計數據和成長預測(2025-2030 年)印尼殺菌劑:市場佔有率分析、產業趨勢與成長預測(2025-2030)印度殺菌劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)歐洲殺菌劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)越南殺菌劑市場:佔有率分析、產業趨勢與統計、成長預測(2025-2030)非洲殺菌劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年) 2025年全球三唑類殺菌劑市場報告

2025年全球三唑類殺菌劑市場報告

▼