|

市場調查報告書

商品編碼

1685835

南美工程塑膠:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029 年)South America Engineering Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

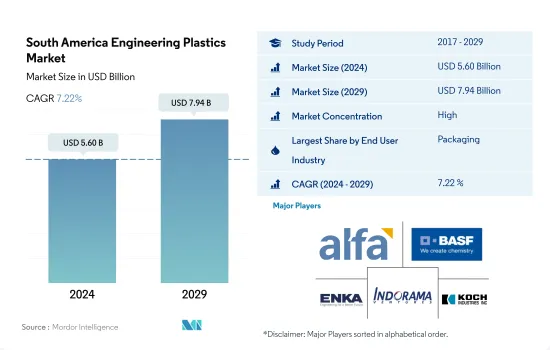

南美工程塑膠市場規模預計在 2024 年為 56 億美元,預計到 2029 年將達到 79.4 億美元,預測期內(2024-2029 年)的複合年成長率為 7.22%。

預測期內包裝產業將佔據市場主導地位

- 工程塑膠比通用一般塑膠具有更優異的機械性能和熱性能,這意味著它們的應用是無限的。工程塑膠正在汽車、航太、建築等各種應用領域中取代金屬和其他傳統材料。

- 工程塑膠的最大消費者是包裝產業。工程塑膠包裝有多種材質和形狀,包括薄膜、瓶子和容器,每種都有其獨特的特性。這些特性包括溫度範圍、適當的食品用途、保存期限、外觀、阻隔性等。工程塑膠既適用於熱灌裝,也可用於冷灌裝,也可在微波爐中加熱,預計在預測期內該產業的消費量複合年成長率為 5.13%。

- 汽車產業是工程塑膠的第二大消費產業,其中各種複合材料取代了更昂貴的金屬及其合金,每種複合材料都是針對其獨特的條件和要求而設計的。業界採用高強度工程塑膠不僅可以降低零件加工、組裝和維護成本,而且可以使汽車更輕、更節能。巴西和阿根廷是該地區汽車工業最發達的國家,預計2023年至2029年期間汽車產業消費以收益為準的複合年成長率為6.74%。

- 由於對智慧電子產品和先進設備的需求不斷增加,電氣和電子產業預計將成為成長最快的產業,從而促進產業的成長。預測期內,該產業的需求量預計複合年成長率為 7.74%。

巴西將在整個預測期內保持主導地位

- 2022年南美洲在全球工程塑膠消費量中的佔有率(以銷售額計算)為4.56%。工程塑膠用於各種行業,包括汽車、包裝、電氣和電子。

- 巴西是最大的工程塑膠消費國,2022年銷量較去年與前一年同期比較成長10.18%。巴西佔南美洲包裝和汽車總產量的近60%和66%。即食簡便食品的需求不斷成長,以及忙碌生活方式的興起,導致包裝材料的消費增加,活性化了該地區工程塑膠的銷售趨勢。汽車需求的激增是個人出行需求不斷成長的結果。技術創新正在推動對電子設備的需求。

- 阿根廷是一個以汽車工業為主導的快速成長消費國家,政府頒布了新的立法,鼓勵對汽車標誌產業的新投資,並加強供應鏈。這將加強該行業的出口導向,並在預測期內促進新引擎技術的發展。這將有助於增加對汽車工程塑膠的需求,預計在預測期內複合年成長率將達到 10.77%(以收益為準)。

- 由於先進材料、有機電子、小型化和顛覆性技術的使用,預測期(2023-2029 年),該地區工程塑膠的消費量預計將以 7.21% 的複合以收益為準成長。

南美洲工程塑膠市場趨勢

技術創新步伐加快推動產業成長

- 在南美洲,巴西佔該地區2017年電氣和電子製造業收入的最大佔有率,接近40%。 2017年,巴西電子產品電商滲透率接近20%。該地區的技術進步增加了對智慧電視、智慧冰箱、智慧空調等家用電器以及其他電氣和電子產品的需求。 2017 年至 2019 年,南美電氣和電子製造收入的複合年成長率超過 6.16%。

- 2020年,受疫情影響,遠距辦公和家庭娛樂等家用電器需求增加,該地區電氣和電子產品產量增加,與前一年同期比較增1.1%。可支配收入的增加、奢侈品需求的不斷成長、技術進步和生活水準的提高是推動電氣和電子設備市場成長的一些主要因素。因此,該地區 2021 年的電氣和電子設備產量銷售額也成長了 14.9%。

- 電子創新的快速步伐推動著對更新、更快的電氣和電子產品的持續需求。因此,該地區對電氣和電子設備生產的需求也在增加。 LG、三星、Panasonic、松下、戴爾、SONY、東芝、索尼、飛利浦、Sharp Corporation、蘋果、聯想等跨國公司的進駐也對電氣和電子設備市場產生了積極影響。預計所有這些因素將在預測期內推動該地區的電氣和電子設備產量增加約 7%。

南美洲工程塑膠產業概況

南美洲工程塑膠市場相當集中,前五大公司佔據了89.63%的市場。市場的主要企業是:Alfa SAB de CV、 BASF SE、Enka、Indorama Ventures Public Company Limited 和 Koch Industries, Inc.(按字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第 1 章執行摘要和主要發現

第2章 報告要約

第 3 章 簡介

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 最終用戶趨勢

- 航太

- 車

- 建築和施工

- 電氣和電子

- 包裝

- 進出口趨勢

- 氟樹脂交易

- 聚醯胺(PA)貿易

- 聚碳酸酯(PC)貿易

- 聚對苯二甲酸乙二酯(PET)貿易

- 聚甲基丙烯酸甲酯(PMMA)貿易

- 聚甲醛(POM)貿易

- 苯乙烯共聚物(ABS 和 SAN)貿易

- 價格趨勢

- 回收概述

- 聚醯胺 (PA) 回收趨勢

- 聚碳酸酯 (PC) 回收趨勢

- 聚對苯二甲酸乙二醇酯 (PET) 的回收趨勢

- 苯乙烯共聚物(ABS、SAN)的回收趨勢

- 法律規範

- 阿根廷

- 巴西

- 價值鏈與通路分析

第5章 市場區隔

- 最終用戶產業

- 航太

- 車

- 建築和施工

- 電氣和電子

- 工業/機械

- 包裝

- 其他最終用戶產業

- 樹脂類型

- 氟樹脂

- 依亞型

- 乙烯-四氟乙烯(ETFE)

- 氟化乙丙烯 (FEP)

- 聚四氟乙烯(PTFE)

- 聚氟乙烯 (PVF)

- 聚二氟亞乙烯(PVDF)

- 其他子樹脂類型

- 液晶聚合物(LCP)

- 聚醯胺(PA)

- 副樹脂類型

- 芳香聚醯胺

- 聚醯胺(PA)6

- 聚醯胺(PA)66

- 聚鄰苯二甲醯胺

- 聚丁烯對苯二甲酸酯(PBT)

- 聚碳酸酯(PC)

- 聚醚醚酮 (PEEK)

- 聚對苯二甲酸乙二醇酯(PET)

- 聚醯亞胺(PI)

- 聚甲基丙烯酸甲酯 (PMMA)

- 聚甲醛(POM)

- 苯乙烯共聚物(ABS 和 SAN)

- 氟樹脂

- 國家

- 阿根廷

- 巴西

- 南美洲其他地區

第6章 競爭格局

- 主要策略趨勢

- 市場佔有率分析

- 業務狀況

- 公司簡介.

- Alfa SAB de CV

- BASF SE

- Celanese Corporation

- China Petroleum & Chemical Corporation

- Covestro AG

- Enka

- Formosa Plastics Group

- Indorama Ventures Public Company Limited

- Koch Industries, Inc.

- LANXESS

- Mitsubishi Chemical Corporation

- SABIC

- Teijin Limited

- Trinseo

- Unigel Plasticos

第7章:執行長的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架(產業吸引力分析)

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源和進一步閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

The South America Engineering Plastics Market size is estimated at 5.60 billion USD in 2024, and is expected to reach 7.94 billion USD by 2029, growing at a CAGR of 7.22% during the forecast period (2024-2029).

Packaging industry to dominate the market during the forecast period

- Engineering plastics, with their superior mechanical and thermal properties compared to common or commodity plastics, have endless applications. They have replaced metals and other traditionally used materials in various application areas, such as automotive, aerospace, building & construction, and more.

- The packaging industry is the largest consumer of engineering plastics. Packaging made from engineering plastics comes in a variety of material types and forms, including films, bottles, containers, and others, each with its own unique characteristics. These characteristics encompass temperature range, appropriate food use, shelf life, appearance, and barrier properties. Suitable for both hot and cold filling, as well as microwave reheating, engineering plastics are expected to see a CAGR of 5.13% in terms of consumption volume from this industry during the forecast period.

- The automotive industry is the second-largest consumer of engineering plastics, which have replaced expensive metals and their alloys with various types of composites, each designed for unique conditions and requirements. The industry uses high-strength engineering plastics, which not only reduces the cost of part processing, assembly, and maintenance but also makes the vehicle lighter and more energy-efficient. Brazil and Argentina have the most developed automotive industries in the region, and consumption in this industry is expected to record a CAGR of 6.74% in terms of revenue from 2023 to 2029.

- The electrical and electronics industry is projected to be the fastest-growing segment due to the increasing demand for smart electronics and advanced devices, contributing to the industry's growth. The demand in this industry is anticipated to record a CAGR of 7.74% in terms of volume during the forecast period.

Brazil to remain dominant during the forecast period

- South America accounted for a share of 4.56%, by revenue, of the consumption of engineering plastics globally in 2022. Engineering plastics have applications in different industries, such as automotive, packaging, electrical and electronics.

- Brazil is the largest consumer of engineering plastics and witnessed a growth of 10.18% in revenue in 2022 compared to the previous year. Brazil occupied nearly 60% and 66% volume shares of packaging and automotive production, respectively, of overall South America. With the growing demand for ready-to-eat convenience food and the emerging trend of on-the-go lifestyles, the consumption of packaging materials increased, increasing the sales of engineering plastics in the region. The surge in automobile demand is a consequence of the increasing demand for private mobility. Technological innovations are driving demand for electronic gadgets.

- Argentina is the fastest-growing consumer, led by the automotive industry, as the government legislated a new Act to promote new investments in the car-marking industry and strengthen its supply chain. This will reinforce the industry's export-oriented profile, promoting the development of new engine technologies during the forecast period. Therefore, the demand for engineering plastics in automotive is likely to increase, registering a CAGR of 10.77%, by revenue, in the country during the forecast period.

- The consumption of engineering plastics in the region is expected to register a CAGR of 7.21% by revenue during the forecast period (2023-2029), owing to the use of advanced materials, organic electronics, miniaturization, and disruptive technologies.

South America Engineering Plastics Market Trends

Rapid pace of technological innovations to boost the industry growth

- In South America, Brazil held the major share of nearly 40% of the region's electrical and electronics production revenue in 2017. In 2017, Brazilian electronics products had a penetration of nearly 20% in the e-commerce sector. The advancement of technology in the region increased the demand for consumer electronics products, such as smart TVs, smart refrigerators, smart air conditioners, and other electrical and electronic products. South American electrical and electronics production revenue witnessed a CAGR of over 6.16% between 2017 and 2019.

- In 2020, with the rise in demand for consumer electronics for remote working and home entertainment due to the pandemic, the production of electrical and electronic products in the region increased at a growth rate of 1.1% by revenue compared to the previous year. Rising disposable income, increased demand for luxury products, technological advancements, and improvement in living standards are some of the major factors driving the electrical and electronics market's growth. As a result, in the region, electrical and electronics production also increased at a rate of 14.9% by revenue in 2021.

- The rapid pace of electronic technological innovation is driving consistent demand for newer and faster electrical and electronic products. As a result, it has also increased the demand for the production of electrical and electronics in the region. The penetration of multinational companies, like LG, Samsung, Microsoft, Panasonic, Dell, Intel, Toshiba, Sony, Philips, Sharp, Apple, and Lenovo, also positively affects the electrical and electronics market. All such factors are expected to fuel the production revenue of electrical and electronics in the region during the forecast period at a rate of around 7%.

South America Engineering Plastics Industry Overview

The South America Engineering Plastics Market is fairly consolidated, with the top five companies occupying 89.63%. The major players in this market are Alfa S.A.B. de C.V., BASF SE, Enka, Indorama Ventures Public Company Limited and Koch Industries, Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.2.1 Fluoropolymer Trade

- 4.2.2 Polyamide (PA) Trade

- 4.2.3 Polycarbonate (PC) Trade

- 4.2.4 Polyethylene Terephthalate (PET) Trade

- 4.2.5 Polymethyl Methacrylate (PMMA) Trade

- 4.2.6 Polyoxymethylene (POM) Trade

- 4.2.7 Styrene Copolymers (ABS and SAN) Trade

- 4.3 Price Trends

- 4.4 Recycling Overview

- 4.4.1 Polyamide (PA) Recycling Trends

- 4.4.2 Polycarbonate (PC) Recycling Trends

- 4.4.3 Polyethylene Terephthalate (PET) Recycling Trends

- 4.4.4 Styrene Copolymers (ABS and SAN) Recycling Trends

- 4.5 Regulatory Framework

- 4.5.1 Argentina

- 4.5.2 Brazil

- 4.6 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Resin Type

- 5.2.1 Fluoropolymer

- 5.2.1.1 By Sub Resin Type

- 5.2.1.1.1 Ethylenetetrafluoroethylene (ETFE)

- 5.2.1.1.2 Fluorinated Ethylene-propylene (FEP)

- 5.2.1.1.3 Polytetrafluoroethylene (PTFE)

- 5.2.1.1.4 Polyvinylfluoride (PVF)

- 5.2.1.1.5 Polyvinylidene Fluoride (PVDF)

- 5.2.1.1.6 Other Sub Resin Types

- 5.2.2 Liquid Crystal Polymer (LCP)

- 5.2.3 Polyamide (PA)

- 5.2.3.1 By Sub Resin Type

- 5.2.3.1.1 Aramid

- 5.2.3.1.2 Polyamide (PA) 6

- 5.2.3.1.3 Polyamide (PA) 66

- 5.2.3.1.4 Polyphthalamide

- 5.2.4 Polybutylene Terephthalate (PBT)

- 5.2.5 Polycarbonate (PC)

- 5.2.6 Polyether Ether Ketone (PEEK)

- 5.2.7 Polyethylene Terephthalate (PET)

- 5.2.8 Polyimide (PI)

- 5.2.9 Polymethyl Methacrylate (PMMA)

- 5.2.10 Polyoxymethylene (POM)

- 5.2.11 Styrene Copolymers (ABS and SAN)

- 5.2.1 Fluoropolymer

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Alfa S.A.B. de C.V.

- 6.4.2 BASF SE

- 6.4.3 Celanese Corporation

- 6.4.4 China Petroleum & Chemical Corporation

- 6.4.5 Covestro AG

- 6.4.6 Enka

- 6.4.7 Formosa Plastics Group

- 6.4.8 Indorama Ventures Public Company Limited

- 6.4.9 Koch Industries, Inc.

- 6.4.10 LANXESS

- 6.4.11 Mitsubishi Chemical Corporation

- 6.4.12 SABIC

- 6.4.13 Teijin Limited

- 6.4.14 Trinseo

- 6.4.15 Unigel Plasticos

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

中國工程塑膠:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)亞太工程塑膠:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029 年)北美工程塑膠:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029 年)工程塑膠:市場佔有率分析、產業趨勢和成長預測(2024-2029)德國工程塑膠:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029 年)歐洲工程塑膠:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029 年)法國工程塑膠市場:佔有率分析、產業趨勢和成長預測(2025-2030 年)

中國工程塑膠:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)亞太工程塑膠:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029 年)北美工程塑膠:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029 年)工程塑膠:市場佔有率分析、產業趨勢和成長預測(2024-2029)德國工程塑膠:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029 年)歐洲工程塑膠:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029 年)法國工程塑膠市場:佔有率分析、產業趨勢和成長預測(2025-2030 年) 全球工程塑膠市場:成長、未來展望與競爭分析(2025-2033)

全球工程塑膠市場:成長、未來展望與競爭分析(2025-2033) 聚甲醛(聚甲醛,POM)市場報告:趨勢、預測與競爭分析(至 2031 年)

聚甲醛(聚甲醛,POM)市場報告:趨勢、預測與競爭分析(至 2031 年) 工程塑膠市場按產品類型、應用和地區分類

工程塑膠市場按產品類型、應用和地區分類