|

市場調查報告書

商品編碼

1687074

中國工程塑膠:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)China Engineering Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

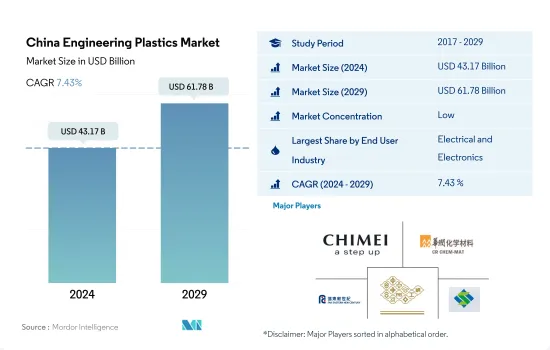

預計 2024 年中國工程塑膠市場規模將達到 431.7 億美元,預計到 2029 年將達到 617.8 億美元,預測期內(2024-2029 年)的複合年成長率為 7.43%。

包裝體積佔有率流失至電氣和電子產業

- 工程塑膠的應用範圍包括航太工業的內牆板和門以及硬質和軟質包裝。亞太工程塑膠市場受包裝、電氣電子和汽車產業推動。 2022年工程塑膠市場體積構成比:包裝電氣電子產業約佔39.65%,電子產業約佔35.86%。

- 2020年,受全球供應鏈中斷影響,中國工程塑膠消費量較去年與前一年同期比較下降2.88%。然而,消費量在 2021 年有所恢復,並在 2022 年繼續穩步成長,數量成長了 2.35%。

- 由於大量生產用於包裝飲料、飲用水、個人護理及家居護理產品的塑膠瓶,包裝行業是全國最大的工程塑膠消費產業。中國是全球最大的電子商務市場,佔全球近50%的市場。預計到 2027 年,該國的電子商務市場銷售額將達到約 2.3 兆美元,高於 2023 年的 1.4 兆美元。預計樹脂消費量將在 2022 年達到 709 萬噸,到 2029 年將達到 960 萬噸。所有這些因素都有望推動產業消費,預計在預測期內,產業以金額為準的複合年成長率將達到 6.47%。

- 汽車產業是中國工程塑膠市場成長最快的終端用戶產業,預計預測期內以金額為準複合年成長率為 9.40%。這與輕質工程塑膠複合材料(如聚碳酸酯、聚醯胺和氟塑膠)在汽車零件中的應用需求日益成長相吻合,這些複合材料具有耐高溫、化學惰性、耐磨、不浸出等優點,可確保性能穩定。

中國工程塑膠市場趨勢

中國仍為全球電子製造中心

- 2020年至2021年,中國電氣電子產業收益將成長14.5%。其中,1-4月電訊設備製造商產量年增8.6%,行動電話製造商與前一年同期比較10.9%。電腦製造商產量與前一年同期比較增3.9%。

- 受新冠疫情影響,2020年筆記型電腦和平板電腦產量分別下降31.1%和24.5%。

- 然而,在同一時期,由於對電子產品和遊戲的需求不斷成長,對電氣和電子產品的需求也隨之增加。 2021年,我國電子製造業利潤總額達8,283億元,與前一年同期比較增38.9%,創歷史最高增速。產業利潤在經歷2018年的下滑之後,2019年至2021年快速成長。

- 中國國防工業電子設備國產化率達85%,國防和高技術設備中關鍵電子元件國產化率由30%提高到85%。中國仍然是全球消費性電子產品重要製造地,吸引全球主要電子製造商建立製造地和研發中心。這些發展推動了 2022 年的電子產品產量,使該國成為全球產量第一。預計這些因素將在預測期內促進電氣和電子行業的生產。

中國工程塑膠產業概況

中國工程塑膠市場較為分散,前五大企業市佔率合計為31.57%。市場的主要企業為:奇美電子、華潤(集團)、遠東新世紀股份有限公司、台塑集團和新豐集團(按字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章執行摘要和主要發現

第2章 報告要約

第 3 章 簡介

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 最終用戶趨勢

- 航太

- 車

- 建築和施工

- 電氣和電子

- 包裝

- 進出口趨勢

- 價格趨勢

- 回收概述

- 聚醯胺 (PA) 回收趨勢

- 聚碳酸酯 (PC) 回收趨勢

- 聚對苯二甲酸乙二醇酯 (PET) 的回收趨勢

- 苯乙烯共聚物(ABS、SAN)的回收趨勢

- 法律規範

- 中國

- 價值鏈與通路分析

第5章 市場區隔

- 最終用戶產業

- 航太

- 車

- 建築和施工

- 電氣和電子

- 工業/機械

- 包裝

- 其他最終用戶產業

- 樹脂類型

- 氟樹脂

- 依亞型

- 乙烯-四氟乙烯(ETFE)

- 氟化乙丙烯 (FEP)

- 聚四氟乙烯(PTFE)

- 聚氟乙烯 (PVF)

- 聚二氟亞乙烯(PVDF)

- 其他子樹脂類型

- 液晶聚合物(LCP)

- 聚醯胺(PA)

- 副樹脂類型

- 芳香聚醯胺

- 聚醯胺(PA)6

- 聚醯胺(PA)66

- 聚鄰苯二甲醯胺

- 聚丁烯對苯二甲酸酯(PBT)

- 聚碳酸酯(PC)

- 聚醚醚酮 (PEEK)

- 聚對苯二甲酸乙二醇酯(PET)

- 聚醯亞胺(PI)

- 聚甲基丙烯酸甲酯 (PMMA)

- 聚甲醛(POM)

- 苯乙烯共聚物(ABS 和 SAN)

- 氟樹脂

第6章 競爭格局

- 主要策略趨勢

- 市場佔有率分析

- 業務狀況

- 公司簡介.

- Chang Chun Group

- CHIMEI

- China Petroleum & Chemical Corporation

- China Resources(Holdings)Co.,Ltd.

- Covestro AG

- Dongyue Group

- Far Eastern New Century Corporation

- Formosa Plastics Group

- Henan Energy Group Co., Ltd.

- Highsun Holding Group

- Jilin Joinature Polymer Co., Ltd.

- PetroChina Company Limited

- Sanfame Group

- Shenzhen Wote Advanced Materials Co.,Ltd.

- Zhejiang Hengyi Group Co., Ltd.

第7章:執行長的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架(產業吸引力分析)

- 全球價值鏈分析

- 市場動態(DRO)

- 資訊來源和進一步閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 54601

The China Engineering Plastics Market size is estimated at 43.17 billion USD in 2024, and is expected to reach 61.78 billion USD by 2029, growing at a CAGR of 7.43% during the forecast period (2024-2029).

Packaging to lose its market share by volume to the electrical and electronics industry

- Engineering plastics have applications ranging from interior wall panels and doors in the aerospace industry to rigid and flexible packaging. The Asia-Pacific engineering plastics market is led by the packaging, electrical and electronics, and automotive industries. The packaging electrical and electronics industries accounted for around 39.65% and 35.86%, respectively, of the engineering plastics market by volume in 2022.

- In 2020, China's engineering plastics consumption fell by 2.88% by volume over the previous year due to disruptions in the global supply chain. However, consumption recovered in 2021 and continued to grow steadily, increasing by 2.35% in volume in 2022.

- The packaging industry consumes the highest amounts of engineering plastics in the country due to the large-scale production of plastic bottles used in the packaging of beverages, drinking water, personal care, and household care products, among others. China is the largest e-commerce market globally, with its share amounting to almost 50%. The country's e-commerce market is projected to reach a revenue of around USD 2.3 trillion in 2027 from USD 1.4 trillion in 2023. In 2022, the industry consumed 7.09 million tons of resin, which is expected to reach 9.6 million tons by 2029. All these factors boost the industry's consumption, which is expected to record a CAGR of 6.47%, by value, during the forecast period.

- Automotive is the fastest-growing end-user industry of the Chinese engineering plastics market, expected to record a CAGR of 9.40% by revenue during the forecast period. This is in line with the industry's increasing demand for lightweight engineering plastic composites, such as polycarbonate, polyamide, and fluoropolymer, for use in vehicle components due to their benefits such as high-temperature use, chemical inertness, resistance to abrasion, and non-leaching capabilities that ensure consistent performance.

China Engineering Plastics Market Trends

China to remain a global electronics manufacturing hub

- China witnessed a 14.5% increase in the revenue of its electrical and electronics industry from 2020 to 2021. Of these, the output of telecom equipment manufacturers registered a Y-o-Y gain of 8.6% in the first four months, while mobile phone output shrank by 10.9% from the previous year. The output of computer manufacturers registered a 3.9% growth in 2020 from the previous year.

- The output of laptops and tablet computers dropped by 31.1% and 24.5%, respectively, in 2020 due to the COVID-19 pandemic-related disruptions.

- However, during the same period, the demand for electrical and electronic products increased owing to the rising demand for electronics and gaming. In 2021, the total profit of Chinese electronic manufacturing enterprises grew by 38.9% over the previous year, reaching CNY 828.3 billion, recording the highest growth rate in the given period. After experiencing a decrease in 2018, the industry's profits rose quickly from 2019 to 2021.

- China domestically manufactures 85% of the electronics used in its defense industry, and the ratio of domestically manufactured essential electronic parts in defense and high-tech equipment rose from 30% to 85%. China remains an important global manufacturing base for consumer electronics, attracting the world's major electronic producers to establish manufacturing bases and research and development centers. Such developments boosted electronics production in 2022, ranking the country first in terms of global production. Such factors are expected to drive production in the electrical and electronics industry during the forecast period.

China Engineering Plastics Industry Overview

The China Engineering Plastics Market is fragmented, with the top five companies occupying 31.57%. The major players in this market are CHIMEI, China Resources (Holdings) Co.,Ltd., Far Eastern New Century Corporation, Formosa Plastics Group and Sanfame Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.3 Price Trends

- 4.4 Recycling Overview

- 4.4.1 Polyamide (PA) Recycling Trends

- 4.4.2 Polycarbonate (PC) Recycling Trends

- 4.4.3 Polyethylene Terephthalate (PET) Recycling Trends

- 4.4.4 Styrene Copolymers (ABS and SAN) Recycling Trends

- 4.5 Regulatory Framework

- 4.5.1 China

- 4.6 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Resin Type

- 5.2.1 Fluoropolymer

- 5.2.1.1 By Sub Resin Type

- 5.2.1.1.1 Ethylenetetrafluoroethylene (ETFE)

- 5.2.1.1.2 Fluorinated Ethylene-propylene (FEP)

- 5.2.1.1.3 Polytetrafluoroethylene (PTFE)

- 5.2.1.1.4 Polyvinylfluoride (PVF)

- 5.2.1.1.5 Polyvinylidene Fluoride (PVDF)

- 5.2.1.1.6 Other Sub Resin Types

- 5.2.2 Liquid Crystal Polymer (LCP)

- 5.2.3 Polyamide (PA)

- 5.2.3.1 By Sub Resin Type

- 5.2.3.1.1 Aramid

- 5.2.3.1.2 Polyamide (PA) 6

- 5.2.3.1.3 Polyamide (PA) 66

- 5.2.3.1.4 Polyphthalamide

- 5.2.4 Polybutylene Terephthalate (PBT)

- 5.2.5 Polycarbonate (PC)

- 5.2.6 Polyether Ether Ketone (PEEK)

- 5.2.7 Polyethylene Terephthalate (PET)

- 5.2.8 Polyimide (PI)

- 5.2.9 Polymethyl Methacrylate (PMMA)

- 5.2.10 Polyoxymethylene (POM)

- 5.2.11 Styrene Copolymers (ABS and SAN)

- 5.2.1 Fluoropolymer

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Chang Chun Group

- 6.4.2 CHIMEI

- 6.4.3 China Petroleum & Chemical Corporation

- 6.4.4 China Resources (Holdings) Co.,Ltd.

- 6.4.5 Covestro AG

- 6.4.6 Dongyue Group

- 6.4.7 Far Eastern New Century Corporation

- 6.4.8 Formosa Plastics Group

- 6.4.9 Henan Energy Group Co., Ltd.

- 6.4.10 Highsun Holding Group

- 6.4.11 Jilin Joinature Polymer Co., Ltd.

- 6.4.12 PetroChina Company Limited

- 6.4.13 Sanfame Group

- 6.4.14 Shenzhen Wote Advanced Materials Co.,Ltd.

- 6.4.15 Zhejiang Hengyi Group Co., Ltd.

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

亞太工程塑膠:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029 年)北美工程塑膠:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029 年)南美工程塑膠:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029 年)工程塑膠:市場佔有率分析、產業趨勢和成長預測(2024-2029)德國工程塑膠:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029 年)歐洲工程塑膠:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029 年)法國工程塑膠市場:佔有率分析、產業趨勢和成長預測(2025-2030 年)

亞太工程塑膠:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029 年)北美工程塑膠:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029 年)南美工程塑膠:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029 年)工程塑膠:市場佔有率分析、產業趨勢和成長預測(2024-2029)德國工程塑膠:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029 年)歐洲工程塑膠:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029 年)法國工程塑膠市場:佔有率分析、產業趨勢和成長預測(2025-2030 年) 全球工程塑膠市場:成長、未來展望與競爭分析(2025-2033)

全球工程塑膠市場:成長、未來展望與競爭分析(2025-2033) 聚甲醛(聚甲醛,POM)市場報告:趨勢、預測與競爭分析(至 2031 年)

聚甲醛(聚甲醛,POM)市場報告:趨勢、預測與競爭分析(至 2031 年) 工程塑膠市場按產品類型、應用和地區分類

工程塑膠市場按產品類型、應用和地區分類

▼