|

市場調查報告書

商品編碼

1685798

中國貨運與物流-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)China Freight and Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

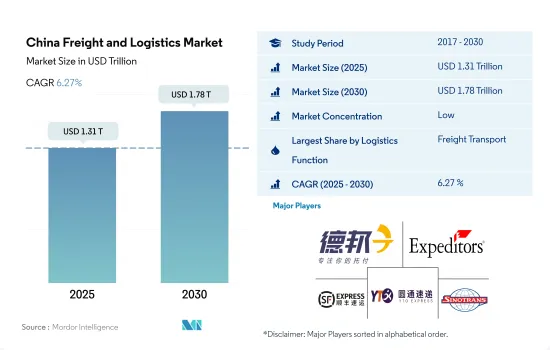

預計 2025 年中國貨運和物流市場規模將達到 1.31 兆美元,到 2030 年預計將達到 1.78 兆美元,預測期內(2025-2030 年)的複合年成長率為 6.27%。

強勁的行業需求和適度的供應導致內部物流服務的採用率增加

- 2022年,同城快遞累計業務量達1,280億件。 2022 年前 11 個月,宅配部門的營收與前一年同期比較增 1.6%。隨著消費者轉向網路購物日常必需品,在封鎖期間他們對宅配服務的依賴增加,這一成長隨之而來。電子商務的蓬勃發展促進了國內宅配、快遞和小包裹(CEP) 服務的需求和數量成長。 2023年6月,菜鳥集團宣布與全球速賣通合作,加速跨國小包裹遞送速度。

- 中國正在積極投資基礎設施,以加強其物流行業並確保供應鏈的無縫銜接。光是2022年,我們就撥款超過34億美元用於改善道路運輸基礎設施。展望未來,國家發展和改革委員會和交通運輸運輸部製定了雄心勃勃的公路擴建目標。到2035年,中國的目標是將公路網擴展至29.9萬公里高速公路和16.2萬公里公路。

中國貨運及物流市場趨勢

根據「十四五」規劃,成長將由清潔能源基礎設施的發展和交通運輸領域的投資推動。

- 2023年,中國清潔能源產業為國家經濟成長做出了重大貢獻。根據能源與清潔空氣中心(CREA)統計,中國對可再生能源基礎設施的投資達8,900億美元,幾乎與當年全球對石化燃料供應的投資相當。清潔能源,包括再生能源來源、核能、電網、能源儲存、電動車和鐵路,到2023年將佔中國GDP的9.0%,與前一年同期比較7.2%。 2023年電動車產量與前一年同期比較成長36%。

- 中國在其「十四五」規劃(2021-2025年)中公佈了擴大交通網路的目標。到2025年,高鐵里程將由2020年的3.8萬公里增加到5萬公里,覆蓋95%的50萬人口以上城市,線路長度達到250公里。到2025年,全國鐵路營業里程將達到16.5萬公里,民用機場270個以上,都市區地鐵營業里程將達到1萬公里,高速公路營業里程將達到19萬公里,高等級內河航道營業里程將達到1.85萬公里。 2025年,實現全面發展是首要目標,重點轉變交通運輸方式,提高交通運輸對GDP的貢獻率。

受俄烏戰爭影響,中國柴油、汽油零售價格飆升至歷史高點。

- 預計2023年中國原油進口量將較2022年成長11%,達到5.6399億噸,即1,128萬桶/日。受俄烏戰爭影響,全球油價上漲,中國燃油價格創歷史新高。 2024年1-2月原油進口量達8,831萬噸,年增5.1%。這一成長是由於之前以較低價格購買了原油。布倫特期貨在2023年9月達到高峰97.69美元,12月跌至72.29美元,2024年3月升至84.05美元。 2024年3月OPEC+集團決定將減產協議延長至6月底,進一步推高了油價。此舉引發了人們對全球石油需求的擔憂,因為該組織將減產近6%的全球需求。近期原油價格上漲也可能從2024年下半年開始抑制中國的進口。

- 中國計劃根據近期國際原油價格波動調整汽油、柴油零售價格。價格上漲反映出全球供應緊張和需求前景改善。根據國發改委預測,2024年中國汽油和柴油價格將上漲28美元/噸。儘管預計燃料需求將下降,但到2035年,石油基燃料仍可能是主要選擇。

中國貨運及物流業概況

中國的貨運和物流市場較為分散,市場上主要企業(按字母順序排列):德邦物流、華盛頓國際快遞、順豐速運(KEX-SF)、上海圓通速遞(物流)和中國外運。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 人口統計

- 按經濟活動分類的GDP分佈

- 經濟活動GDP成長

- 通貨膨脹率

- 經濟表現及概況

- 電子商務產業趨勢

- 製造業趨勢

- 交通運輸倉儲業GDP

- 出口趨勢

- 進口趨勢

- 燃油價格

- 卡車運輸成本

- 卡車持有量(按類型)

- 物流績效

- 主要卡車供應商

- 模態共享

- 海運能力

- 班輪連結性

- 停靠港和演出

- 貨運趨勢

- 貨物噸位趨勢

- 基礎設施

- 法律規範(公路和鐵路)

- 中國

- 法律規範(海運和空運)

- 中國

- 價值鍊和通路分析

第5章市場區隔

- 最終用戶產業

- 農業、漁業和林業

- 建設業

- 製造業

- 石油和天然氣、採礦和採石

- 批發和零售

- 其他

- 物流功能

- 快遞、快遞和小包裹(CEP)

- 目的地

- 國內的

- 國際的

- 貨物

- 按交通方式

- 航空

- 海上和內陸水道

- 其他

- 貨物

- 交通方式

- 航空

- 管道

- 鐵路

- 路

- 海上和內陸水道

- 倉庫存放

- 溫度管理

- 無溫度控制

- 溫度管理

- 其他服務

- 快遞、快遞和小包裹(CEP)

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介.

- Deppon Logistics Co., Ltd.

- Deutsche Bahn AG(including DB Schenker)

- DHL Group

- Dimerco

- DSV A/S(De Sammensluttede Vognmaend af Air and Sea)

- Expeditors International of Washington, Inc.

- Kuehne+Nagel

- SF Express(KEX-SF)

- Shanghai YTO Express(Logistics)Co., Ltd.

- SINOTRANS

- United Parcel Service of America, Inc.(UPS)

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(市場促進因素、限制因素、機會)

- 技術進步

- 資訊來源及延伸閱讀

- 圖表清單

- 關鍵見解

- 資料包

- 詞彙表

- 外匯

簡介目錄

Product Code: 47655

The China Freight and Logistics Market size is estimated at 1.31 trillion USD in 2025, and is expected to reach 1.78 trillion USD by 2030, growing at a CAGR of 6.27% during the forecast period (2025-2030).

Rising adoption of in-house logistics services owing to booming demand and moderate supply in the industry

- In 2022, intra-city express deliveries reached a cumulative volume of 128 billion. The parcel delivery sector saw a 1.6% Y-o-Y revenue increase in the first 11 months of 2022. This uptick was driven by heightened reliance on parcel services during lockdowns, as consumers increasingly turned to online shopping, even for daily essentials. This surge in e-commerce bolstered domestic demand and volume for courier, express, and parcel (CEP) services. In June 2023, Cainiao Group, in collaboration with AliExpress, announced plans to expedite cross-border parcel deliveries, aiming to cut delivery times to five working days, a 30% acceleration from the industry average.

- China is actively investing in infrastructure to bolster its logistics sector and ensure a seamless supply chain. In 2022 alone, the country allocated over USD 3.4 billion for road transport infrastructure improvements. Looking ahead, the National Development and Reform Commission, along with the Ministry of Transport, has set ambitious goals for road expansion. By 2035, they aim to extend the national road network to 299,000 kilometers of highways and 162,000 kilometers of expressways.

China Freight and Logistics Market Trends

Rising focus on developing clean energy infrastructure and transport sector investment under 14th Five-Year Plan driving growth

- In 2023, China's clean energy sector significantly contributed to the country's economic expansion. According to Energy and Clean Air (CREA), China's investment in renewable energy infrastructure amounted to USD 890 billion, almost matching global investments in fossil fuel supply for the same year. Clean energy, including renewable energy sources, nuclear power, electricity grids, energy storage, electric vehicles (EVs), and railways, constituted 9.0% of China's GDP in 2023, up from 7.2% YoY. EV production grew by 36% YoY in 2023.

- In the 14th Five-Year Plan (2021-2025), China revealed goals for expanding its transportation network. By 2025, high-speed railways will extend to 50,000 kms, up from 38,000 kms in 2020, with 95% of cities with populations above 500,000 covered by 250-km lines. The country aims to increase its railway length to 165,000 kms, civil airports to over 270, subway lines in cities to 10,000 kms, expressways to 190,000 kms, and high-level inland waterways to 18,500 kms by 2025. The primary objective is to achieve integrated development by 2025, emphasizing advancements in the transformation of the transportation system and its contribution to GDP.

China's retail diesel and gasoline prices were soared to historically high levels amid the Russia-Ukraine War

- In 2023, China imported 11% more crude oil than in 2022, totaling 563.99 mn metric tons (MMT), or 11.28 mn barrels per day. This surge was due to increased global crude oil prices amid the Russia-Ukraine War, causing fuel prices in China to reach historic highs. In Jan-Feb 2024, crude oil imports rose by 5.1% YoY, reaching 88.31 MMT. This increase was driven by purchasing crude oil at lower prices earlier. Brent futures peaked at USD 97.69 in September 2023, fell to USD 72.29 in December, and rose to USD 84.05 by March 2024. The decision made by the OPEC+ group in March 2024 to extend output cuts until the end of June has further boosted crude prices. This move has raised concerns about global oil demand, as the group is reducing production by nearly 6% of world demand. The recent increase in crude prices may also dampen China's imports starting from H2 2024.

- China plans to adjust retail prices for gasoline and diesel to align with recent shifts in global crude oil prices. The price hike reflects a tightening of global supply and a positive forecast for demand. According to NDRC, gasoline and diesel prices in China will increase by USD 28 per ton in 2024. Although there's expectation of declining demand for fuels, oil-based fuels will remain the primary choice until 2035.

China Freight and Logistics Industry Overview

The China Freight and Logistics Market is fragmented, with the major five players in this market being Deppon Logistics Co., Ltd., Expeditors International of Washington, Inc., SF Express (KEX-SF), Shanghai YTO Express (Logistics) Co., Ltd. and SINOTRANS (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Demographics

- 4.2 GDP Distribution By Economic Activity

- 4.3 GDP Growth By Economic Activity

- 4.4 Inflation

- 4.5 Economic Performance And Profile

- 4.5.1 Trends in E-Commerce Industry

- 4.5.2 Trends in Manufacturing Industry

- 4.6 Transport And Storage Sector GDP

- 4.7 Export Trends

- 4.8 Import Trends

- 4.9 Fuel Price

- 4.10 Trucking Operational Costs

- 4.11 Trucking Fleet Size By Type

- 4.12 Logistics Performance

- 4.13 Major Truck Suppliers

- 4.14 Modal Share

- 4.15 Maritime Fleet Load Carrying Capacity

- 4.16 Liner Shipping Connectivity

- 4.17 Port Calls And Performance

- 4.18 Freight Pricing Trends

- 4.19 Freight Tonnage Trends

- 4.20 Infrastructure

- 4.21 Regulatory Framework (Road and Rail)

- 4.21.1 China

- 4.22 Regulatory Framework (Sea and Air)

- 4.22.1 China

- 4.23 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes 1. Market value in USD for all segments 2. Market volume for select segments viz. freight transport, CEP (courier, express, and parcel) and warehousing & storage 3. Forecasts up to 2030 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode Of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode Of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Deppon Logistics Co., Ltd.

- 6.4.2 Deutsche Bahn AG (including DB Schenker)

- 6.4.3 DHL Group

- 6.4.4 Dimerco

- 6.4.5 DSV A/S (De Sammensluttede Vognmaend af Air and Sea)

- 6.4.6 Expeditors International of Washington, Inc.

- 6.4.7 Kuehne+Nagel

- 6.4.8 SF Express (KEX-SF)

- 6.4.9 Shanghai YTO Express (Logistics) Co., Ltd.

- 6.4.10 SINOTRANS

- 6.4.11 United Parcel Service of America, Inc. (UPS)

7 KEY STRATEGIC QUESTIONS FOR FREIGHT AND LOGISTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (Market Drivers, Restraints & Opportunities)

- 8.1.5 Technological Advancements

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 8.7 Currency Exchange Rate

02-2729-4219

+886-2-2729-4219

亞太貨運與物流-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美貨運和物流:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)南美貨運和物流:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)印尼貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)印度貨運和物流:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)德國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)日本的貨運和物流:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)歐洲貨運和物流-市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)法國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)泰國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

亞太貨運與物流-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美貨運和物流:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)南美貨運和物流:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)印尼貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)印度貨運和物流:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)德國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)日本的貨運和物流:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)歐洲貨運和物流-市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)法國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)泰國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

▼