|

市場調查報告書

商品編碼

1686636

歐洲貨運和物流-市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)Europe Freight And Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

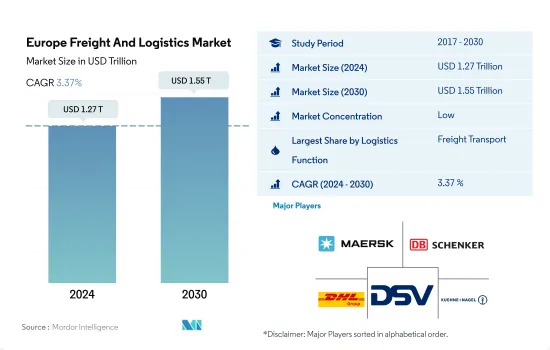

預計 2024 年歐洲貨運和物流市場規模為 1.27 兆美元,到 2030 年將達到 1.55 兆美元,預測期內(2024-2030 年)的複合年成長率為 3.37%。

包括德國政府投資 150 億美元在內的不斷增加的投資正在開放市場。

- 2022 年,亞馬遜在其配送車隊中引入了 5 輛電動重型貨車 (HGV),每年行駛 10 萬英里,減少碳排放超過 170 噸。德國正在努力安裝全國架空電網,為遠距電動卡車供電,這是 2050 年實現運輸業脫碳的努力的一部分。

- 2020年,德國對交通基礎設施的重大投資約為351.2億美元,其中大部分(86.6%)用於交通路線的建設和維護。 2022年,德國聯邦政府在交通基礎建設的支出較2021年大幅增加。尤其重要的是,2021年為聯邦鐵路撥款124.5億美元,是2016年撥款金額的兩倍多。 2022年預算為聯邦公路撥款超過135.8億美元,為水路撥款19.2億美元。

- 法國政府已製定了到 2028 年的基礎設施支出計劃,重點關注高速公路,投資額達 51 億歐元(54.4 億美元)。作為雄心勃勃的法國2030投資計畫的一部分,法國政府承諾投入25億歐元(26.6億美元),到2030年將電動和混合動力汽車汽車的產量提高到約200萬輛。 2022年,法國政府也啟動了加速部署電動車高功率充電站的計劃。法國政府的這項戰略舉措可望促進該國近距離貨運業的發展。

跨境電子商務將推動歐洲貨運和物流的成長並帶來改變。

- 德國政府已撥款 6.26 億美元的財政支持計劃,以促進該國 15 個主要機場的供應鏈運作。其中,4.26億美元將用於小型機場,特別是空中導航服務和交通管制基礎設施。德國的目標是到 2045 年實現氣候淨零排放,並認知到交通運輸部門脫碳的重要性,目前該部門約佔該國排放的 20%。德國聯邦航空管理局 (LBA) 是監督民航環境、安保和人事事務的國家機構,其對航空業的認知不斷提高,進一步強調了對永續性的關注。

- 2023 年,總部位於英國的鐵路營運商 Colas Rail推出了新子公司 Colas Rail Traction,進軍法國市場,該公司最近獲得了鐵路牌照。該子公司將設在巴黎西部的 Louveciennes,預計將僱用 140 名員工。 Colas Rail Traction 的主要業務將是機械、工作列車和貨物的運輸,以補充其現有的子公司 Colas Rail France,後者專門從事鐵路線路的設計、建設和維護。

- 英國CEP(快遞、速遞和小包裹)產業經歷了顯著成長,公司數量從 2012 年的 12,550 家增加到 2021 年的 39,165 家,年成長率高達 13.48%。預計到 2025 年電子商務滲透率將達到 90%,CEP 公司已準備好利用不斷擴大的線上消費市場。尤其是服飾和小工具,是英國消費者最喜歡在網路上訂購的產品。

歐洲貨運和物流市場的趨勢

歐盟撥款57.6億美元用於135個交通計劃以促進經濟復甦

- 運輸和倉儲業在支援各行各業的業務中發揮著至關重要的作用,其中德國位居榜首,超過法國和英國。德國是全球第三大貨物出口國和進口國。德國聯邦政府宣布將增加對交通基礎設施的投資,2022年將為聯邦公路撥款超過120億歐元(128億美元),為水路撥款約17億歐元(18.1億美元),彰顯其改善交通網路的決心。

- 德國政府打算對鐵路網的投資大於公路網的投資。 2022年,德國鐵路、聯邦政府和地方政府將在鐵路基礎建設上投資約136億歐元(145.1億美元)。下薩克森州、漢堡州、不來梅州、梅克倫堡-前波美拉尼亞和石勒蘇益格-荷爾斯泰因州正在與德國鐵路公司合作,投資到 2030 年對其鐵路網路進行現代化改造。

- 2022年,歐盟核准為約135個交通基礎建設計劃提供54億歐元的津貼。這些計劃旨在支持歐盟成員國在大洪水後的經濟復甦,加強交通網路,促進永續交通,提高安全性並創造就業機會。所有受支持的計劃都是跨歐洲交通網路的一部分,連接歐盟成員國,並符合歐盟到 2030 年完成 TEN-T 核心網路和到 2050 年完成綜合網路的目標。

自2023年2月起,俄羅斯的進口被禁止,導致來自中東、亞洲和北美的柴油進口量增加。

- 在法國,2023年底SP95-E10的價格為每公升1.96美元,柴油的價格為每公升1.93美元。法國大型石油公司道達爾能源公司宣布,到2024年,將法國的燃料價格上限設定為每公升1.99歐元。此外,德國2023年的天然氣消費量與2022年相比減少了5%。與2018年至2021年的平均消費量相比,德國的天然氣需求下降了17.5%。此外,到 2023 年為止,英國加油站的汽油平均價格已超過每公升 150披索(1.80 美元),而柴油價格已上漲至每公升 152.41披索(1.83 美元)。 2023 年 1 月,西班牙的燃料價格比英國汽油每公升低約 20 美分,柴油每公升低約 40 美分。

- 俄羅斯是歐洲最大的柴油供應國。 2023年,歐洲柴油價格下跌。自 2023 年 2 月歐盟實施禁止從俄羅斯進口石油產品禁令以來,俄羅斯對歐洲的柴油出口量平均為 24,000 桶/天,比 2022 年俄羅斯對歐洲的 63 萬桶/天下降了 96%。從 2 月到 5 月,中東對歐洲的柴油出口增加了 51%(16 萬桶/天),亞洲增加了 97%(147,000 桶/天),北美增加了 65%(47,000 桶/天)。

- 丹麥的汽油價格最高,而芬蘭的柴油價格最高。奧地利的汽油最便宜,西班牙的柴油最便宜。德國也預計,受歐盟排放權交易的影響,2027年燃料價格將大幅上漲。與2026年相比,2027年初,汽油價格將上漲每公升38美分,天然氣價格將上漲每度約3美分。

歐洲貨運及物流業概況

歐洲貨運及物流市場較分散,前五大公司佔10.02%。市場的主要企業有:AP Moller-Maersk、DB Schenker、DHL Group、DSV A/S (De Sammensluttede Vognmaend af Air and Sea) 和 Kuehne+Nagel(按字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 人口統計

- 按經濟活動分類的GDP分佈

- 按經濟活動分類的GDP成長

- 通貨膨脹率

- 經濟表現及概況

- 電子商務產業趨勢

- 製造業趨勢

- 交通運輸倉儲業GDP

- 出口趨勢

- 進口趨勢

- 燃油價格

- 卡車運輸成本

- 卡車持有量(按類型)

- 物流績效

- 主要卡車供應商

- 模態共享

- 海運能力

- 班輪連結性

- 停靠港和表演

- 貨運趨勢

- 貨物噸位趨勢

- 基礎設施

- 法律規範(公路和鐵路)

- 法國

- 德國

- 義大利

- 荷蘭

- 北歐的

- 俄羅斯

- 西班牙

- 英國

- 法律規範(海事和航空)

- 法國

- 德國

- 義大利

- 荷蘭

- 北歐的

- 俄羅斯

- 西班牙

- 英國

- 價值鍊和通路分析

第5章市場區隔

- 最終用戶產業

- 農業、漁業和林業

- 建設業

- 製造業

- 石油和天然氣、採礦和採石

- 批發和零售

- 其他

- 物流功能

- 快遞、快遞和小包裹(CEP)

- 目的地

- 國內的

- 國際的

- 貨物

- 按交通方式

- 航空

- 海上和內陸水道

- 其他

- 貨物

- 交通方式

- 航空

- 管道

- 鐵路

- 路

- 海上和內陸水道

- 倉庫存放

- 溫度管理

- 無溫度控制

- 溫度管理

- 其他服務

- 快遞、快遞和小包裹(CEP)

- 國家

- 丹麥

- 芬蘭

- 法國

- 德國

- 冰島

- 義大利

- 荷蘭

- 挪威

- 俄羅斯

- 西班牙

- 瑞典

- 英國

- 其他歐洲國家

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介.

- AP Moller-Maersk

- CH Robinson

- Dachser

- DB Schenker

- DHL Group

- DSV A/S(De Sammensluttede Vognmaend af Air and Sea)

- Expeditors International of Washington, Inc.

- FedEx

- Hapag-Lloyd

- Kuehne+Nagel

- Mainfreight

- United Parcel Service of America, Inc.(UPS)

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(市場促進因素、限制因素、機會)

- 技術進步

- 資訊來源及延伸閱讀

- 圖表清單

- 關鍵見解

- 資料包

- 詞彙表

- 外匯

The Europe Freight And Logistics Market size is estimated at 1.27 trillion USD in 2024, and is expected to reach 1.55 trillion USD by 2030, growing at a CAGR of 3.37% during the forecast period (2024-2030).

Rising investments, including USD 15 billion, from the German government are developing the market

- In 2022, Amazon launched 5 electric heavy goods vehicles (HGVs) in its delivery fleet, covering 100,000 annual road miles to cut down over 170 tonnes of carbon emissions. The country is working toward installing a nationwide network of overhead wires to power long-distance electric trucks as part of efforts to decarbonize the transportation sector by 2050.

- In 2020, Germany witnessed a significant investment of nearly USD 35.12 billion in its transport infrastructure, with a major chunk, 86.6%, allocated to the construction and maintenance of traffic routes. The German federal government's spending on transport infrastructure saw a notable uptick in 2022 compared to 2021. Of particular significance was the allocation of USD 12.45 billion to federal railroads in 2021, more than double the amount allocated in 2016. In 2022, the budget allocated over USD 13.58 billion for federal highways and USD 1.92 billion for waterways.

- The French government has outlined its infrastructure spending plans until 2028, with a significant focus on highways, earmarking investments worth EUR 5.1 billion (USD 5.44 billion). As part of the ambitious France 2030 investment plan, the government has committed EUR 2.5 billion (USD 2.66 billion) to bolster the production of nearly two million electric and hybrid vehicles by 2030. In 2022, the government also initiated a call for projects to facilitate the deployment of high-power charging stations for electric vehicles. These strategic moves by the French government are poised to bolster the growth of short-haul trucking in the country.

Cross-border e-commerce is driving growth and transforming freight and logistics in Europe

- The German government has allocated a financial support package of USD 626 million to bolster the supply chain operations in the country's 15 key airports. Out of this, USD 426 million is earmarked for smaller airports, specifically for air navigation services and traffic control infrastructure. With a target of achieving net-zero climate emissions by 2045, Germany recognizes the significance of decarbonizing its transportation sector, which currently accounts for about 20% of the nation's emissions. This focus on sustainability is further underscored by heightened industry awareness, with the Luftfahrt-Bundesamt (LBA) serving as Germany's national authority overseeing environmental, security, safety, and personnel matters in civil aviation.

- In 2023, UK-based rail company Colas Rail made its foray into the French market by launching a new subsidiary, Colas Rail Traction, which recently obtained its rail license. Headquartered in Louveciennes, west of Paris, the subsidiary is set to employ a workforce of 140. Colas Rail Traction's core operations will revolve around the transportation of machinery, work trains, and freight, complementing its existing subsidiary, Colas Rail France, which specializes in rail design, construction, and maintenance.

- The UK's CEP (Courier, Express, and Parcel) industry witnessed a significant surge, with the number of enterprises rising from 12,550 in 2012 to 39,165 in 2021, marking an impressive annual growth rate of 13.48%. With e-commerce projected to reach a penetration rate of 90% by 2025, CEP companies are poised to capitalize on the expanding online consumer market. Notably, clothing and gadgets are among the top products UK consumers prefer to order online.

Europe Freight And Logistics Market Trends

European Union allocated USD 5.76 billion to 135 transportation projects to boost economic recovery

- The transportation and warehouse sector plays a crucial role in supporting operations across various industries, with Germany leading as the dominant player, surpassing France and the United Kingdom. Globally, Germany ranks third in both imports and exports of goods. The German federal government expressed its intention to increase investments in transportation infrastructure, allocating over EUR 12 billion (USD 12.80 billion) for federal highways and around EUR 1.7 billion (USD 1.81 billion) for waterways in 2022, thereby demonstrating its commitment to improving transportation networks.

- The German government intends to invest more in rail than road network. In 2022, Deutsche Bahn, the federal government, and the local and regional governments invested roughly EUR 13.6 billion (USD 14.51 billion) in rail infrastructure. Lower Saxony, Hamburg, Bremen, Mecklenburg-Western Pomerania, and Schleswig-Holstein are partnering with DB to invest in modernizing their rail network by 2030.

- In 2022, the European Union approved EUR 5.4 billion through grants for approximately 135 transport infrastructural projects. These projects aim to aid post-pandemic economic recovery in the EU Member States, enhance transport links, promote sustainable transportation, boost safety, and create job opportunities. All supported projects are part of the Trans-European Transport Network, which connects EU Member States and aligns with the European Union's goal of completing the TEN-T core network by 2030 and the comprehensive network by 2050, all while aligning with climate objectives outlined in the European Green Deal.

Since February 2023, diesel imports from the Middle East, Asia, and North America have increased due to the ban on imports from Russia

- In France, 2023 ended with a litre of SP95-E10 priced at USD 1.96 and diesel at USD 1.93. TotalEnergies (the French oil company giant) announced that it will keep a 1.99 euro per liter cap on French fuel prices throughout 2024. Moreover, in 2023, gas consumption in Germany dropped by 5% compared to 2022. While compared to the average consumption in the period 2018 to 2021, gas demand in Germany fell by 17.5%. Furthermore, the average cost of petrol at UK forecourts has risen to break 150p a liter (USD 1.80) since the start of 2023, and diesel has risen to 152.41p a liter (USD 1.83). Spanish fuel prices were lower than in the United Kingdom by about 20 cents per liter for petrol and 40 cents per liter for diesel in January 2023.

- Russia has been Europe's largest supplier of diesel. In 2023, diesel prices declined in Europe. Since February 2023, when the European Union implemented the ban on petroleum product imports from Russia, diesel exports from Russia to Europe have averaged 24,000 barrels per day (b/d), down by 96% from the 630,000 b/d Russia sent to Europe in 2022. From February through May, diesel exports to Europe increased by 51% (160,000 b/d) from the Middle East, by 97% (147,000 b/d) from Asia, and by 65% (47,000 b/d) from North America.

- Denmark is the most expensive country for petrol, and Finland is the most expensive for diesel. Austria has the cheapest petrol, and Spain is the cheapest for diesel. Moreover, Germany anticipates a fuel price jump from 2027 EU emissions trading. An increase of 38 cents per liter of petrol and around 3 cents per kilowatt hour of natural gas at the beginning of 2027 compared to 2026.

Europe Freight And Logistics Industry Overview

The Europe Freight And Logistics Market is fragmented, with the top five companies occupying 10.02%. The major players in this market are A.P. Moller - Maersk, DB Schenker, DHL Group, DSV A/S (De Sammensluttede Vognmaend af Air and Sea) and Kuehne + Nagel (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Demographics

- 4.2 GDP Distribution By Economic Activity

- 4.3 GDP Growth By Economic Activity

- 4.4 Inflation

- 4.5 Economic Performance And Profile

- 4.5.1 Trends in E-Commerce Industry

- 4.5.2 Trends in Manufacturing Industry

- 4.6 Transport And Storage Sector GDP

- 4.7 Export Trends

- 4.8 Import Trends

- 4.9 Fuel Price

- 4.10 Trucking Operational Costs

- 4.11 Trucking Fleet Size By Type

- 4.12 Logistics Performance

- 4.13 Major Truck Suppliers

- 4.14 Modal Share

- 4.15 Maritime Fleet Load Carrying Capacity

- 4.16 Liner Shipping Connectivity

- 4.17 Port Calls And Performance

- 4.18 Freight Pricing Trends

- 4.19 Freight Tonnage Trends

- 4.20 Infrastructure

- 4.21 Regulatory Framework (Road and Rail)

- 4.21.1 France

- 4.21.2 Germany

- 4.21.3 Italy

- 4.21.4 Netherlands

- 4.21.5 Nordics

- 4.21.6 Russia

- 4.21.7 Spain

- 4.21.8 United Kingdom

- 4.22 Regulatory Framework (Sea and Air)

- 4.22.1 France

- 4.22.2 Germany

- 4.22.3 Italy

- 4.22.4 Netherlands

- 4.22.5 Nordics

- 4.22.6 Russia

- 4.22.7 Spain

- 4.22.8 United Kingdom

- 4.23 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes 1. Market value in USD for all segments 2. Market volume for select segments viz. freight transport, CEP (courier, express, and parcel) and warehousing & storage 3.Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode Of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode Of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.3 Country

- 5.3.1 Denmark

- 5.3.2 Finland

- 5.3.3 France

- 5.3.4 Germany

- 5.3.5 Iceland

- 5.3.6 Italy

- 5.3.7 Netherlands

- 5.3.8 Norway

- 5.3.9 Russia

- 5.3.10 Spain

- 5.3.11 Sweden

- 5.3.12 United Kingdom

- 5.3.13 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 A.P. Moller - Maersk

- 6.4.2 C.H. Robinson

- 6.4.3 Dachser

- 6.4.4 DB Schenker

- 6.4.5 DHL Group

- 6.4.6 DSV A/S (De Sammensluttede Vognmaend af Air and Sea)

- 6.4.7 Expeditors International of Washington, Inc.

- 6.4.8 FedEx

- 6.4.9 Hapag-Lloyd

- 6.4.10 Kuehne + Nagel

- 6.4.11 Mainfreight

- 6.4.12 United Parcel Service of America, Inc. (UPS)

7 KEY STRATEGIC QUESTIONS FOR FREIGHT AND LOGISTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (Market Drivers, Restraints & Opportunities)

- 8.1.5 Technological Advancements

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 8.7 Currency Exchange Rate

中國貨運與物流-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)亞太貨運與物流-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美貨運和物流:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)南美貨運和物流:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)印尼貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)印度貨運和物流:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)德國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)日本的貨運和物流:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)法國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)泰國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

中國貨運與物流-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)亞太貨運與物流-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美貨運和物流:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)南美貨運和物流:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)印尼貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)印度貨運和物流:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)德國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)日本的貨運和物流:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)法國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)泰國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)