|

市場調查報告書

商品編碼

1686189

印度貨運和物流:市場佔有率分析、行業趨勢和統計數據、成長預測(2025-2030 年)India Freight and Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

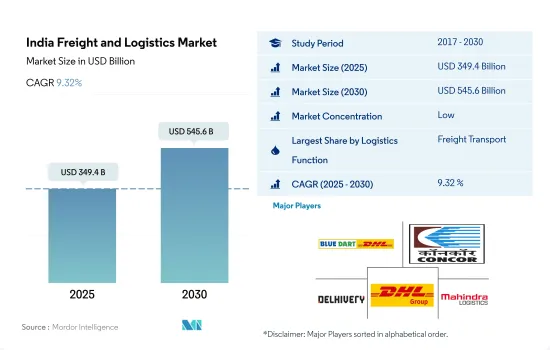

印度貨運和物流市場規模預計在 2025 年為 3,494 億美元,預計到 2030 年將達到 5,456 億美元,預測期內(2025-2030 年)的複合年成長率為 9.32%。

越來越多的政府舉措和計劃(例如 ZEV-EMI(零排放汽車新興市場計劃))正在推動該行業的需求。

- 到2025年,印度機場管理局和私人營運商將共同投資110億美元。作為擴大區域連通計劃(五年)的一部分,計劃開發規模較小、服務不足和偏遠的機場。印度目前擁有400條區域航線,另有600條正在規劃中,總合連接156個機場。印度的目標是到 2024 年建造 100 個新機場,採用政府資助和官民合作關係相結合的方式。此外,21 個擬建待開發區機場中有 8 個已經運作,包括傑瓦爾的諾伊達國際機場,該機場將成為該國最大的機場。機場佔地 1,334 公頃,擁有最先進的體積模組化設計。

- 2023 年 7 月,15 家知名公司在零排放汽車新興市場計劃 (ZEV-EMI) 和印度政府的永續交通電動貨運加速器 (E-FAST) 計劃下攜手合作。此次合作是在二十國集團清潔能源部長會議上宣布的,並宣布了幾個先導計畫。因此,預計到 2027 年印度對電動卡車 (E-trucks) 的需求將超過 5,000 輛,到 2030 年將達到約 7,700 輛。

印度貨運和物流市場趨勢

政府和私人投資、出口成長以及州際貨運量的增加是運輸業的主要驅動力

- 政府設定了2024年將物流成本降低5-6%的目標。印度鐵路正在努力提高貨運能力、加快貨運列車速度、降低貨運票價、建立專用貨運走廊並改善火車站、公路和港口之間最後一英里的連通性。我們正在與首席部長加蒂·沙克蒂合作,賦予物流行業地位,推廣數位解決方案,並發展物流和基礎設施。這些努力旨在降低成本並刺激物流領域的GDP成長。

- 預計該產業將持續成長,到 2027 年將增加 1,000 萬個就業機會。印度渴望成為全球製造和物流中心,最近的政策吸引了約 100 億美元的倉儲和物流行業投資。印度 2024 年的基礎設施計劃,如孟買跨港口連接線 (MTHL)、新孟買國際機場、諾伊達國際機場和西部專用貨運走廊,也有望加速印度成為全球物流領域重要參與者的進程。

由於多個邦政府削減增值稅,柴油價格的漲幅沒有汽油價格的漲幅那麼大。

- 9 月份,在沙烏地阿拉伯和俄羅斯將自願減產和出口協議延長至 2023 年後,原油價格觸及每桶 90 美元的 10 個月高點。由於印度 85% 的石油依賴進口,燃料價格受到了影響。代表 1,400 萬名卡車駕駛人和車輛駕駛人的全印度汽車運輸大會表示,不斷上漲的燃油價格正在影響印度卡車司機,因為他們轉嫁價格上漲的能力有限,而價格上漲佔卡車營運成本的 70%。

- 印度政府正考慮在 2024 年將汽油和柴油價格每公升降低 4-6 印度盧比(0.04-0.07 美元),以趕上定於 2024 年上半年舉行的人民院選舉。目前,政府正在與石油行銷公司進行討論,以平等分擔減價負擔,這可能會導致每公升汽油和柴油價格大幅下降,最高可達 10 盧比(0.12 美元)。此舉旨在減輕人們的經濟負擔,也可能導致零售通膨率下降,零售通膨率在2023年11月達到5.55%的高峰。

印度貨運及物流業概況

印度貨運和物流市場較為分散,前五大公司分別是 Blue Dart Express Limited、Container Corporation of India Limited、Delhi Ltd.、DHL Group 和 Mahindra Logistics Ltd.(按字母順序排列)。 (按字母順序)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 人口統計

- 按經濟活動分類的GDP分佈

- 經濟活動GDP成長

- 通貨膨脹率

- 經濟表現及概況

- 電子商務產業趨勢

- 製造業趨勢

- 交通運輸倉儲業GDP

- 出口趨勢

- 進口趨勢

- 燃油價格

- 卡車運輸成本

- 卡車持有量(按類型)

- 物流績效

- 主要卡車供應商

- 模態共享

- 海運能力

- 班輪連結性

- 停靠港和演出

- 貨運趨勢

- 貨物噸位趨勢

- 基礎設施

- 法律規範(公路和鐵路)

- 印度

- 法律規範(海運和空運)

- 印度

- 價值鍊和通路分析

第5章市場區隔

- 最終用戶產業

- 農業、漁業和林業

- 建設業

- 製造業

- 石油和天然氣、採礦和採石

- 批發和零售

- 其他

- 物流功能

- 快遞、快遞和小包裹(CEP)

- 目的地

- 國內的

- 國際的

- 貨物

- 按交通方式

- 航空

- 海上和內陸水道

- 其他

- 貨物

- 交通方式

- 航空

- 管道

- 鐵路

- 路

- 海上和內陸水道

- 倉庫存放

- 溫度管理

- 無溫度控制

- 溫度管理

- 其他服務

- 快遞、快遞和小包裹(CEP)

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介.

- Allcargo Logistics Ltd.

- Blue Dart Express Limited

- Container Corporation of India Limited

- Delhivery Ltd.

- Deutsche Bahn AG(including DB Schenker)

- DHL Group

- DSV A/S(De Sammensluttede Vognmaend af Air and Sea)

- FedEx

- Kuehne+Nagel

- Mahindra Logistics Ltd.

- Safexpress Pvt. Ltd.

- Transport Corporation of India Ltd.(TCI)

- VRL Logistics Ltd.

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 世界概況

- 概述

- 五力分析框架

- 全球價值鏈分析

- 市場動態(市場促進因素、限制因素、機會)

- 技術進步

- 資訊來源及延伸閱讀

- 圖表清單

- 關鍵見解

- 資料包

- 詞彙表

- 外匯

簡介目錄

Product Code: 50214

The India Freight and Logistics Market size is estimated at 349.4 billion USD in 2025, and is expected to reach 545.6 billion USD by 2030, growing at a CAGR of 9.32% during the forecast period (2025-2030).

Growing government initiatives and programs like Zero Emission Vehicles Emerging Markets Initiative (ZEV-EMI) are driving industry demand

- Till 2025, the Airports Authority of India and private operators are jointly investing a substantial USD 11 billion. As part of the expanding Regional Connectivity Scheme (spanning over 5 years), there are plans to develop smaller, underserved, and remote airports. While India currently has 400 regional routes, an additional 600 are in the pipeline to connect to a total of 156 airports. By 2024, India had aimed to establish 100 new airports, with a mix of government funding and public-private partnerships. Moreover, eight out of the planned 21 greenfield airports are already operational, with the Noida International Airport at Jewar set to be the country's largest. Spanning 1,334 hectares, this airport boasts a cutting-edge volumetric modular design.

- In a significant move in July 2023, 15 prominent companies joined forces under the Zero Emission Vehicles Emerging Markets Initiative (ZEV-EMI) and the Indian government's E-FAST (Electric Freight Accelerator for Sustainable Transport) program. This collaboration, announced at the G20 and Clean Energy Ministerial event, unveiled multiple pilot projects. As a result, the demand for electric trucks (e-trucks) in India is projected to surpass 5,000 by 2027 and reach approximately 7,700 by 2030.

India Freight and Logistics Market Trends

Government and private investments, rising exports, and the increasing interstate movement of goods are the major drivers of the transportation industry

- In 2024, the government is dedicated to reducing logistics costs to 5-6%. Indian Railways is taking steps to boost freight capacity, increase the speed of freight trains, lower freight expenses, establish dedicated freight corridors, improve last-mile connectivity between railheads, roads, and ports. They're aligning with PM Gati Shakti, granting industry status to logistics, promoting digital solutions, and developing logistics infrastructure. These efforts aim to cut costs and spur GDP growth in logistics.

- The sector is expected to grow till 2027 and is expected to add 10 million jobs by 2027. India is aiming to become a global hub for manufacturing and logistics, with recent policies attracting around USD 10 billion USD in investments for the warehousing and logistics sector. Also India's infrastructure plans for 2024, such as the Mumbai Trans Harbour Link (MTHL), Navi Mumbai International Airport, Noida International Airport and Western Dedicated Freight Corridor etc, are expected to accelerate India's journey towards becoming a prominent player in the global logistics landscape.

The diesel price increase was less sharp than the increase in petrol prices due to VAT cuts offered by several state governments

- In September 2023, oil prices hit a 10-month high of USD 90 per barrel as Saudi Arabia and Russia extended their voluntary production and export cuts till 2023. As India imports 85% of its oil, the fuel prices were impacted. According to the All-India Motor Transport Congress, which represents 14 million truckers and vehicle operators, the soaring fuel prices are impacting India's truckers as they have limited ability to pass on the rising prices, which account for 70% of the cost of operating a truck.

- The Indian government is contemplating reducing petrol and diesel prices by INR 4 - INR 6 (USD 0.04 - USD 0.07) per litre in 2024, timed with the upcoming Lok Sabha elections in H1 2024. Discussion in ongoing with Oil Marketing Companies to share the burden of this reduction equally, and there's a possibility of a more substantial cut of up to Rs 10 (USD 0.12) per litre. This move aims to alleviate the financial strain on the public and could also help lower retail inflation, which peaked at 5.55% in November 2023.

India Freight and Logistics Industry Overview

The India Freight and Logistics Market is fragmented, with the major five players in this market being Blue Dart Express Limited, Container Corporation of India Limited, Delhivery Ltd., DHL Group and Mahindra Logistics Ltd. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Demographics

- 4.2 GDP Distribution By Economic Activity

- 4.3 GDP Growth By Economic Activity

- 4.4 Inflation

- 4.5 Economic Performance And Profile

- 4.5.1 Trends in E-Commerce Industry

- 4.5.2 Trends in Manufacturing Industry

- 4.6 Transport And Storage Sector GDP

- 4.7 Export Trends

- 4.8 Import Trends

- 4.9 Fuel Price

- 4.10 Trucking Operational Costs

- 4.11 Trucking Fleet Size By Type

- 4.12 Logistics Performance

- 4.13 Major Truck Suppliers

- 4.14 Modal Share

- 4.15 Maritime Fleet Load Carrying Capacity

- 4.16 Liner Shipping Connectivity

- 4.17 Port Calls And Performance

- 4.18 Freight Pricing Trends

- 4.19 Freight Tonnage Trends

- 4.20 Infrastructure

- 4.21 Regulatory Framework (Road and Rail)

- 4.21.1 India

- 4.22 Regulatory Framework (Sea and Air)

- 4.22.1 India

- 4.23 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes 1. Market value in USD for all segments 2. Market volume for select segments viz. freight transport, CEP (courier, express, and parcel) and warehousing & storage 3. Forecasts up to 2030 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Logistics Function

- 5.2.1 Courier, Express, and Parcel (CEP)

- 5.2.1.1 By Destination Type

- 5.2.1.1.1 Domestic

- 5.2.1.1.2 International

- 5.2.2 Freight Forwarding

- 5.2.2.1 By Mode Of Transport

- 5.2.2.1.1 Air

- 5.2.2.1.2 Sea and Inland Waterways

- 5.2.2.1.3 Others

- 5.2.3 Freight Transport

- 5.2.3.1 By Mode Of Transport

- 5.2.3.1.1 Air

- 5.2.3.1.2 Pipelines

- 5.2.3.1.3 Rail

- 5.2.3.1.4 Road

- 5.2.3.1.5 Sea and Inland Waterways

- 5.2.4 Warehousing and Storage

- 5.2.4.1 By Temperature Control

- 5.2.4.1.1 Non-Temperature Controlled

- 5.2.4.1.2 Temperature Controlled

- 5.2.5 Other Services

- 5.2.1 Courier, Express, and Parcel (CEP)

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Allcargo Logistics Ltd.

- 6.4.2 Blue Dart Express Limited

- 6.4.3 Container Corporation of India Limited

- 6.4.4 Delhivery Ltd.

- 6.4.5 Deutsche Bahn AG (including DB Schenker)

- 6.4.6 DHL Group

- 6.4.7 DSV A/S (De Sammensluttede Vognmaend af Air and Sea)

- 6.4.8 FedEx

- 6.4.9 Kuehne+Nagel

- 6.4.10 Mahindra Logistics Ltd.

- 6.4.11 Safexpress Pvt. Ltd.

- 6.4.12 Transport Corporation of India Ltd. (TCI)

- 6.4.13 VRL Logistics Ltd.

7 KEY STRATEGIC QUESTIONS FOR FREIGHT AND LOGISTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (Market Drivers, Restraints & Opportunities)

- 8.1.5 Technological Advancements

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 8.7 Currency Exchange Rate

02-2729-4219

+886-2-2729-4219

中國貨運與物流-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)亞太貨運與物流-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美貨運和物流:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)南美貨運和物流:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)印尼貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)德國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)日本的貨運和物流:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)歐洲貨運和物流-市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)法國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)泰國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

中國貨運與物流-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)亞太貨運與物流-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)北美貨運和物流:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)南美貨運和物流:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)印尼貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)德國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)日本的貨運和物流:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)歐洲貨運和物流-市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)法國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)泰國貨運與物流:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

▼